No surprise – this past week was all about the banking sector.

Investors fled banks, worried about how bad the contagion would get in the wake of the collapses of Signature Bank and Silicon Valley Bank.

To that end, the banking group housed within the CE 100 Index plunged 9.5%

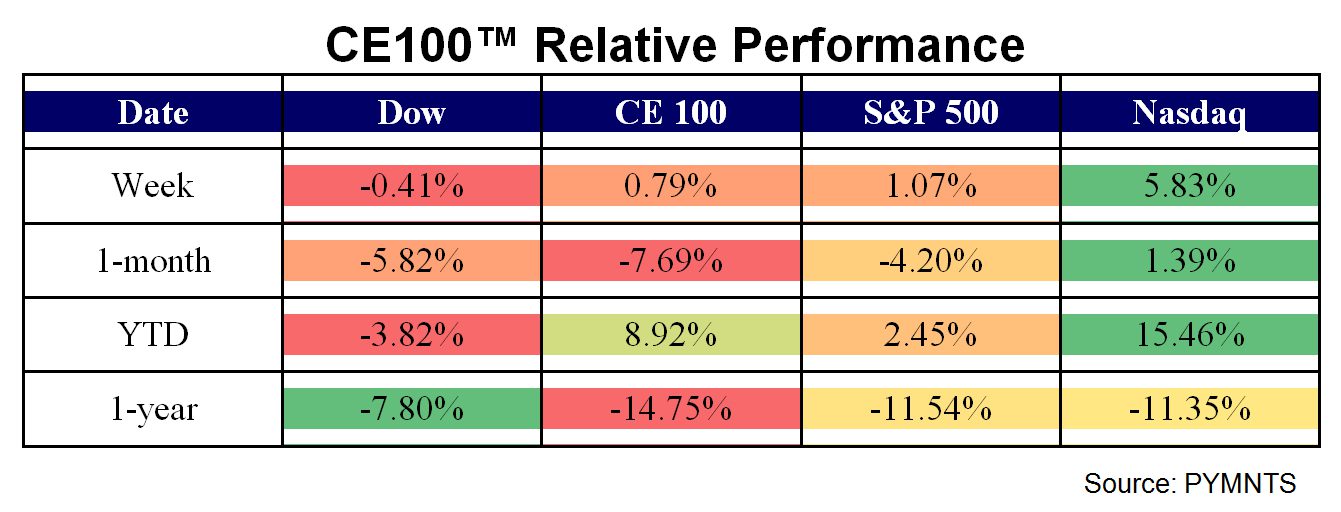

And yet, with the help of other sectors, which posted positive performances — specifically, the 6.4% rally in the Enablers segment — the CE 100 Index gathered 0.8% to cap what could only be described as a topsy-turvy week. That performance lagged the broader market gain of 1% in the S&P 500 Stock Index.

The companies that were most impacted within the bank group include Ally Bank, which gave up 13.8%. LendingClub was 13.3% lower, having noted in an SEC filing earlier in the month that it had $21 million in deposits at SVB.

Citigroup was off 8.5%, J.P. Morgan slid 5.9% and Goldman lost 7.5%. Those banks were among the names making uninsured deposits totaling $30 billion into First Republic Bank.

The move, we reported here, ensures First Republic has liquidity and shows the importance of regional, midsize and small banks, the 11 banks said Thursday in a joint press release. Citigroup and J.P. Morgan Chase each deposited $5 billion. Goldman Sachs deposited $2.5 billion.

As to what happens next: Over the weekend, various news outlets including The New York Times reported that the Swiss government would announce a deal whereby UBS would buy Credit Suisse for roughly $1 billion.

Within the Enablers group — which, as noted above, helped offset the bank group’s decline — Fastly gathered 15.2%.

News came this week that Fastly has entered into an agreement with Google to operate an Oblivious HTTP Relay as part of FLEDGE, the Privacy Sandbox initiative to help protect personally identifiable information. The Privacy Sandbox is a set of proposals to reduce cross-site and cross-app tracking.

MongoDB gained 13.2%, having reported fourth quarter results that showed revenues of $361.3 million were up 36% year over year. Subscription revenue was $348.2 million, gaining 35% from last year’s fourth quarter. During the conference call with analysts, CEO Dev Ittycheria stated that the company added about 500 net new direct sales customers, and noted that “we continue to have success in new workloads in existing accounts. Unlike many of our peers, we have not seen the macro environment impact our ability to win new business.”

Alphabet, which surged 12.6%, joining other Big Tech firms that have published monthly active users (MAU) numbers to comply with new regulations, as part of the European Union’s (EU’s) Digital Services Act (DSA). As PYMNTS noted this past week, under the act, online platforms and search engines had to publish their monthly active users to show whether they meet the threshold — 45 million users — at which they are classified as “very large online platforms” (VLOPs).

Alphabet reported that the MAU of signed-in users was 401.7 million for YouTube, 332 million for Google Search, 278.6 million for Google Maps, 274.6 million for Google Play and 74.9 million for Shopping, per the report.

Separately, and in a reminder that earnings season still has yet to conclude — and pressures of high interest rates and challenging capital markets are impacting sectors other than banks — Porch, focused on the home service industry, plummeted 29.6%.

Total revenue for the fourth quarter of 2022 was $64.1 million, an increase of 24% from last year (even as software segment revenues slipped 7%). But losses increased, as presentation materials showed that adjusted EBITDA (a rough measure of cash flow) was a negative $13.3 million, compared to a negative $5.4 million last year, due in part to weather-related events.

Though management sees growth ahead, top line momentum looks set to slow a bit, as revenues in the current year are projected to grow 20%. As Adam Kornick, president of the InsurTech division, said on the conference call, “I’ve been in the insurance industry for two decades, and 2022 was one of the most difficult years in my experience. We saw inflation increasing claims costs along the storms with Hurricane Ian in Q3 and Winter Storm Elliott in Q4, plus increases in reinsurance pricing.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More