In many B2B software as a service (SaaS) markets and technology-enabled services, competitors compete on service, technology, geographic reach, and relatively transparent pricing. This is especially true in the procurement of services related to accounts payable and treasury organizations — where transactional models are well established. Examples include: lockbox services, outsourced billing, check printing, ACH processing, scan and OCR services, etc.

But in the world of broad, horizontal e-invoicing and payment solutions – the kind delivered by Ariba, Paymode-X, Taulia, Tradeshift and many others – the competitors still compete even on the basic business model used to sell their services. This is pretty unusual for a market that has been around for 15 years!

It is hard for an enterprise buying organization to determine exactly what the full e-invoice to e-pay process will cost them, given that some platforms:

That’s why I call it business model mayhem.

There appear to be at least three business models at play in the market:

1. Buyer-pay. Tradeshift seems to follow this model. The buyer pays and the suppliers pay nothing, at least the e-invoicing part. From the Tradeshift website: “The Tradeshift platform was built with suppliers in mind. We deliver free electronic invoicing, faster payments, and predictable cash flow.” Tradeshift has been an historically e-invoice oriented vendor, less payment oriented, so the payment part is less clear from the website.

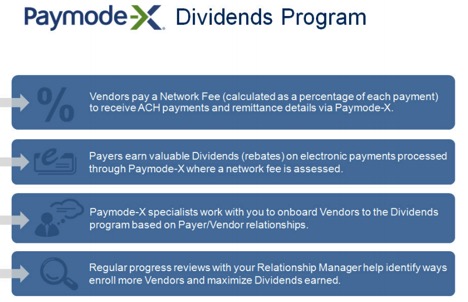

2. Supplier-pay (Buyer Rebate?). Paymode-X has moved to this model, as have a number of outsourcing organizations which want to take over your payments for you. These organizations may even pay you for the privilege of making your payments, as long as you work with them to negotiate the terms and “payment modality” for your vendors. That’s a fancy way of saying these payment providers will try to maximize card rebates, or early payment discounts, and share these fees with the enterprise buyer.

Here’s a diagram from a Paymode-X presentation (readily available on the Web):

Note that Paymode-X is a historically payment-centric provider, the inverse of Tradeshift. Also note that this approach appears to be relatively recent for Paymode-X as their CEO Robert Eberle said in their fiscal Q1 2015 earnings call, “We signed a record 13 new Paymode-X deals under the new vendor pay model.”

As you can imagine, the supplier pay model is compelling to many buyers relative to footing the bill themselves! But the supplier-pay model also forces the enterprise buyer to trust that the SaaS vendor’s value proposition will be strong enough to induce suppliers to participate. Otherwise the buyer paid nothing and received very little! Smaller buyers, and those more concerned with vendor relationships, may not be willing to take this risk.

3. Everyone pays. Charging both sides of the equation seems to be the model employed by Ariba, Tungsten/OB10, and Taulia (though I’m not sure about the latter, as there is nothing on their website to indicate). Ariba used to have a buyer fee for e-invoicing functionality and a relatively transparent supplier fee (relatively transparent in that it is clearly posted on the Web, though it is a little hard to follow). OB10, bought by Tungsten, had a similar business model. Both of these firms started in the e-invoicing market and then added payment. Ariba added AribaPay, whose business model is not yet clear, and Tungsten has made it clear it is adding payment and supply chain finance.

If all of this seems a little confusing to you, it could just be my writing style! But, I think it is more indicative of one of the many problems that have held this market back. In 15 years, we have made limited progress in moving to e-invoicing and e-payment. There are many reasons for this, but one reason is this lack of transparency and clarity of business model.

In many markets, one of the benefits of moving to a SaaS world has been relative transparency of the total cost of ownership of a solution for buyers. In fact, one of the first tests to determine whether a solution is SaaS should be whether the website has a pricing page with transparent pricing! If not, the buyer is probably in for a relatively typical enterprise software sales cycle, which has many of the elements we associate with car-buying, except that even car-buying has moved on! This process drags on for both the buyer and SaaS vendor.

The e-invoicing and payment market has yet to achieve this level of transparency, but does appear to moving that direction. Clearly, buyer prices are dropping for e-invoicing, and e-payment seems to be moving to a supplier pay model, with the value proposition for the supplier being earlier payment and rich remittance. When the providers converge and the pricing models clarify, the market will accelerate even more.

Full disclosure: I worked for Ariba from 2000-2010, but I am not privy to any non-public information. I own an immaterial amount of stock in Paymode-X’s owner, Bottomline Technologies.

Bob Solomon

CEO, Software Platform Consulting

Bob Solomon is the principal of Software Platform Consulting, Inc. (SPCI). Bob helps clients develop networks and platforms that offer value to all industry participants, including their owners. Prior to founding SPCI, Bob was President of ServiceChannel, a SaaS platform in the facilities management industry. During Bob’s tenure, ServiceChannel nearly doubled in size, instituted a new business model, and dramatically improved profitability. Prior to ServiceChannel, Bob was Senior Vice President, Network and Financial Solutions for Ariba, Inc. (now part of SAP). Reporting to Ariba’s CEO, Bob was responsible for monetization of the Ariba Network, Ariba’s cloud platform for connecting Global 2000 customers to their supply bases. Bob’s team helped make the Ariba Network Ariba’s fastest growing and most profitable business.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More