A testament to just how difficult and uncertain the Lending Club situation has been of late — a slight hiccup in the marketplace lender’s website last night caused some pretty big worries, as investors were suddenly concerned the end had come.

One nervous investor tweeted out his concern that “[a]s a long-time investor there, I am worried that they have closed down.”

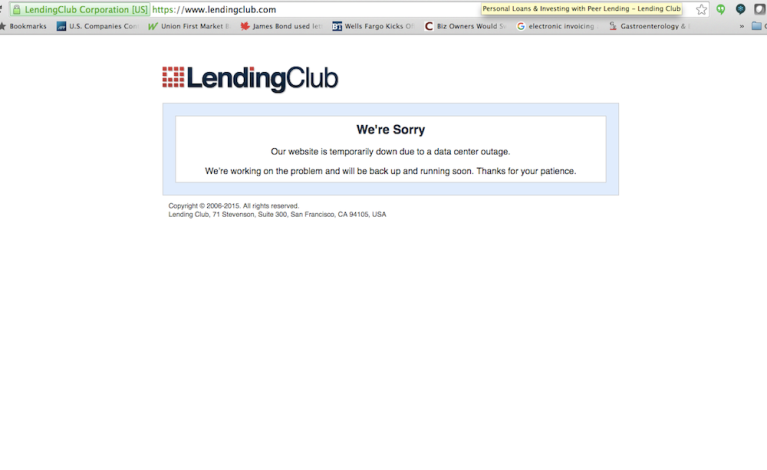

Calls placed to customer service didn’t yield much past the normal suggestion that customer service closed at 5 p.m. PST and to please call back the next day.

Lending Club, however, clearly noticed it was making people nervous and tweeted that it was in the midst of resolving a data center outage.

“We’re working to resolve a data center outage & our website is currently down. Sorry for any inconvenience- we’ll be back up & running soon!”

The outage was oddly timed, to say the least. Reports earlier in the day had indicated that departed CEO Renaud Laplanche might be working out a plan with investors to retake his firm. The Laplanche revelation came in tandem with the news that Lending Club’s second-largest shareholder had unloaded all of its stock and that the firm’s annual investor meeting was to be put off for two weeks.

But of course, the firm is ailing because of reasons directly connected to Laplanche, who an internal investigation connected to falsified loan documents and a failure to disclose personal holdings before a major Lending Club investment.

The situation is a bit of a mess, which is likely why investors got so jumpy when the site went down. Luckily for all, by 9:30 p.m. EST, the situation had been resolved, and LC was back online. It was still online at 6:30 this morning.

But come around 7 a.m. — it’s back down again.

What’s next?

Some think that, whether or not Laplanche can overcome his specific issues, it is seeming that Lending Club is increasingly likely to be acquired. At its IPO, the firm was worth $9 billion; that value, as of today, is less than $2 billion.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More