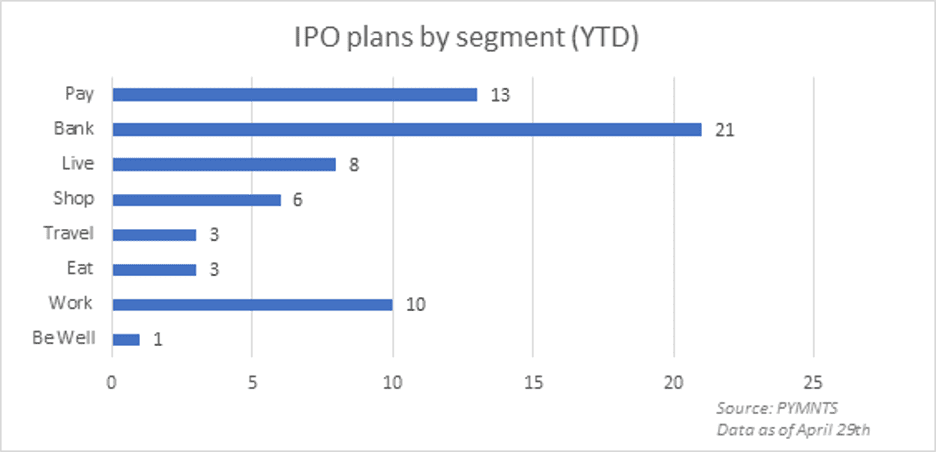

The latest edition of the ongoing SPAC/IPO Tracker finds that traditional listings held sway in the past week.

To that end, among the banks that have announced initial public offering (IPO) plans, Five Star Bank, based in California, with seven branches, had filed earlier in the month to go public in an IPO with plans to raise up to $100 million in its listing. As reported by Renaissance Capital, the company posted $75 million in earnings for the year that ended in December. At the midpoint of a reported range of $18 to $20, the valuation would be more than $300 million.

Separately, Paycor HCM, which offers a software-as-a-service human capital management platform geared toward small and medium-sized businesses (SMBs), also filed to raise as much as $100 million for an IPO. As reported by PYMNTS this month, Paycor solutions streamline payroll workflows and regulatory compliance. The company currently works with more than 40,000 SMBs offering a range of recruiting, payroll and HR solutions. The firm had $338 million in revenues for the trailing 12 months that ended March 31, with growth year over year of 13 percent.

And as we’d noted last week, PropTech firms have been gaining momentum on the listing front. On the heels of the SmartRent.com listing news, late this month, mortgage lending software platform Blend said it would go public, filing a confidential IPO with the Securities and Exchange Commission (SEC).

Beyond the confines of the U.S., Brazilian mobile payments app PicPay filed with the SEC for an IPO valued at up to $100 million. The company’s platform features a credit card and P2P payments, among other offerings.

Weighing In On The SEC

Advertisement: Scroll to Continue

Though special purpose acquisition company (SPAC) activity may have been relatively quiet in the spaces germane to PYMNTS in the past few days, the space is still drawing much interest, especially from a regulatory standpoint, through the lens of the SEC. As reported by Reuters, the commission is considering, according to reports, “new guidance to rein in growth projections” made by the blank check firms after they list, and the SEC is also reportedly mulling whether these firms qualify for specific legal protections.

Against the backdrop of what might be a shifting regulatory landscape, Clint Smith, a partner in the Jones Walker Corporate Practice Group and co-leader of the firm’s corporate, securities, and executive compensation team, weighed in with PYMNTS via written exchange on the lures and challenges of SPAC listings.

Generally, speaking, he said in terms of the practicalities of listing SPACs, they are relatively easier to bring to market than traditional IPOs for a few reasons.

“First, the SPAC has no business activity, making the required securities law disclosures very simple at the time of their initial public offering,” said Smith. “Second, the SPAC’s target acquisition is an acquisition, not an IPO; hence, many of the onerous IPO diligence and disclosure requirements are not required at the time of the SPAC’s acquisition transaction.”

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Asked by PYMNTs what verticals may command attention going forward, he said that logical targets will have capital needs to grow or expand, and those firms may have attributes that make an IPO less desirable.

“For example, technology companies may seek SPAC transactions if their lack of sustained net income renders IPO valuation uncertain,” he said.

Disclosures In Focus

With a nod toward the SEC’s focus on SPACs, he added, “sponsors may face increasing scrutiny of their disclosures and structures at the time of their initial public offering and their business combinations.” He noted, too, that in the wake of a business combination, all of the risks attendant with public reporting companies become risks of the target company.

The risks, he said, “include, from a financial reporting standpoint, appropriate books and records, audited financial statements that satisfy SEC requirements, disclosure controls and procedures and internal control over financial reporting.” The target company will, moving forward, be providing SEC level discourse of its business and operations — more likely at a higher level than had been done in the past.

As for the investors, he said, “there are a lot of unique risks in SPACs that retail investors and institutional investors should be concerned about, including risks related to fees, conflicts of interest, and sponsor compensation that may not be present if they were investing in a private operating company through an underwritten public offering.“

Recent SEC releases on issues that should be examined by public companies mulling SPACs, said Smith, spotlight the fact that “from the private operating company’s perspective, it will inherit not only the general set of rules and regulations that apply to public companies such as internal controls, exchange act reporting obligations and exchange listing standards as flagged by the SEC, but also rules that uniquely apply to companies that are shell companies or former shell companies.” The SEC article, he said, is likely not intended to encourage or discourage SPAC combinations.

Said Smith, “I believe the SEC was pointing out that a SPAC combination is not a shortcut to becoming a public company — you would still have all the general rules that apply to public companies, plus a few unique aspects of combining with a shell company.”

Read More On IPOs: