The higher a consumer’s income, the higher their credit score and the less often they check it, according to “The New Reality Check,” a PYMNTS and LendingClub collaboration based on a survey of 2,326 U.S. consumers.

Get the report: The New Reality Check

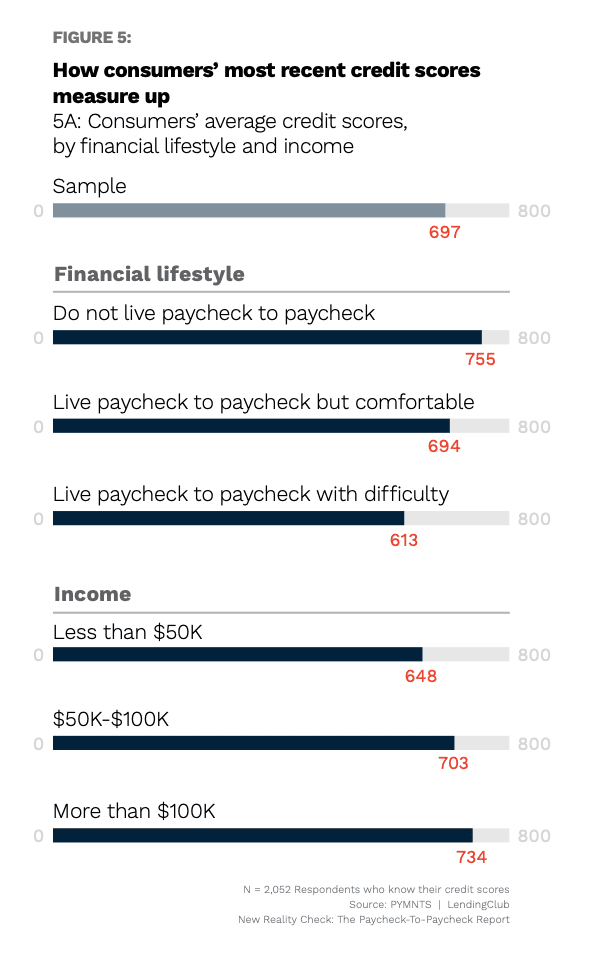

Among those included in the survey, the average U.S. consumer’s credit score in March 2022 was 697.

When categorized by income, there’s an 86-point gap between the credit scores of high-income consumers and low-income consumers, the report found.

The average credit score among high-income consumers — those earning more than $100,000 — was 734.

Among consumers earning $50,000 to $100,000, the average credit score was 703.

Advertisement: Scroll to Continue

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Among low-income consumers — those earning less than $50,000 — the average credit score was 648.

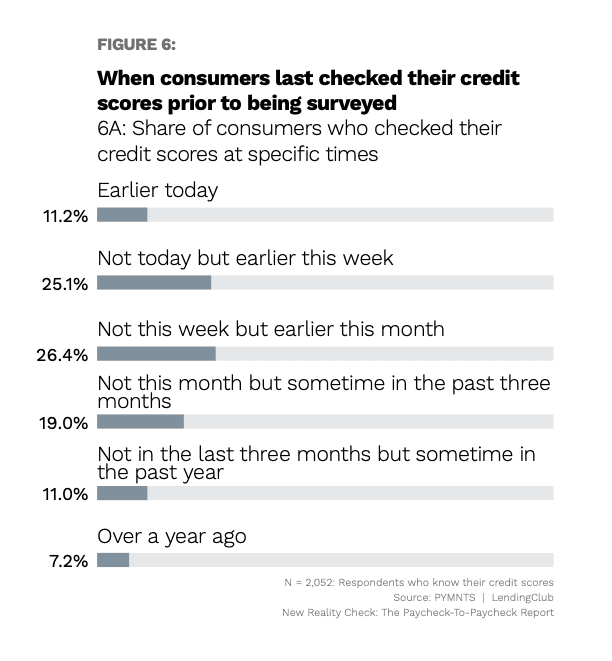

Sixty-three percent of all consumers said they had checked their credit score during the month leading up to March 2022, with 11% saying they had checked it earlier during the day they were surveyed, 25% saying they had checked it not today but earlier this week and 26% saying they had checked it not this week but earlier this month.

Among the different income groups, there’s a difference of seven percentage points in terms of the share of consumers who check their credit scores monthly

Those with a below-average credit score checked their report more often — and most frequently among the three income groups identified in the report — with 67% saying they had checked it during the month prior to being surveyed.

Among consumers with a credit score that was about average, 63% had checked it — the same percentage as that of the entire sample.

Those with an above-average credit score checked it least often, with 60% saying they had checked it during the month leading up to March 2022.