Payments modernization remains the order of the day in 2022 as companies of all sizes decide how to proceed with implementing solutions to reduce friction in B2B payments.

Financial institutions (FIs) small and large rely on automated account validation and digital lockboxes but realize that they either need to partner or outsource important work to specialists so that new solutions improve both money management and customer experience.

For the study “Meeting the Challenge of Payments Modernization: How Organizational Size Influences Innovation,” a PYMNTS and FIS collaboration, we surveyed over 300 executives heading treasury services or wholesale banking at large global banks, big national banks, regional banks, community banks and credit unions (CUs) managing over $500 million in assets.

The following data points reflect the state of payments modernization efforts now underway.

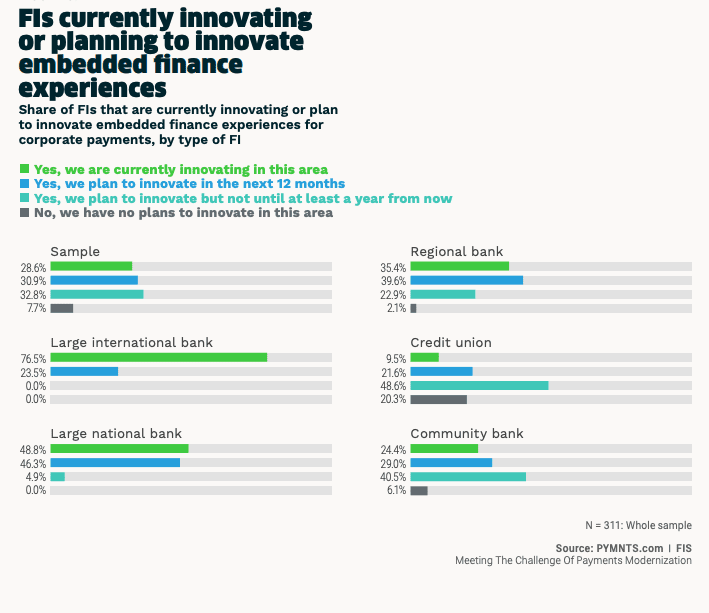

Data show that nine out of 10 FIs are now pursuing or plan to pursue embedded finance solutions to ease B2B payments frictions, but timetables and the focus of those efforts vary by FI size.

“Payment processing is the top embedded finance experience FIs plan to innovate, with 52% of FIs likely to do so,” the study stated. “Community banks and regional banks are the most likely FI types to make these plans.”

However, PYMNTS found that large banks “are more likely to cite loans and cash flow management as areas they are innovating or plan to innovate with embedded finance.”

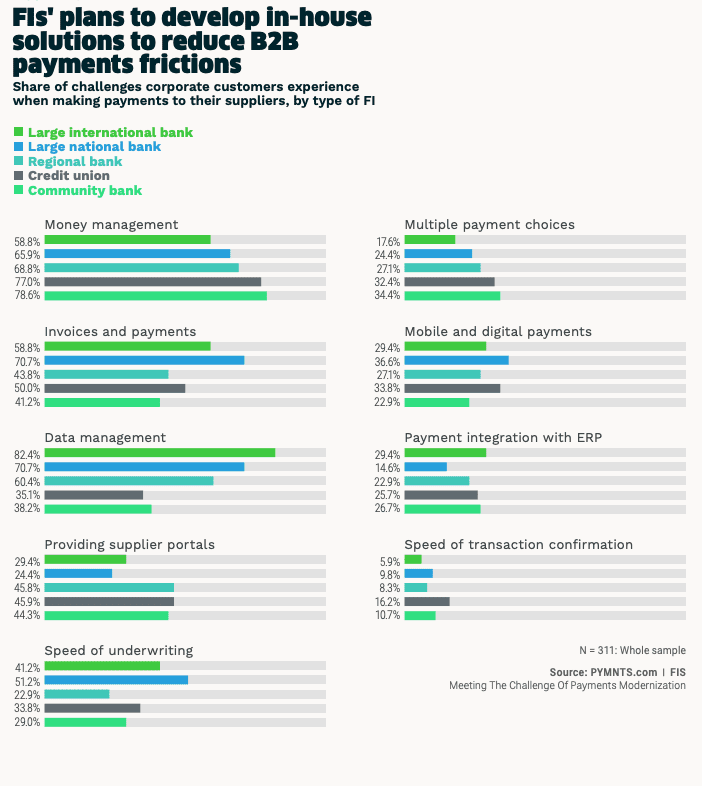

With money management, invoicing and payments, data management and supplier portals rank as high priorities for all FIs, while smaller ones are focusing where they see the biggest impact.

“Money management frictions are a target smaller FIs are currently tackling or planning to tackle via digital solutions, as 82% of community banks and 80% of credit unions report working on or planning to work on solutions to this end,” the study stated.

Money management rates with larger FIs, but data is more of an immediate concern for these.

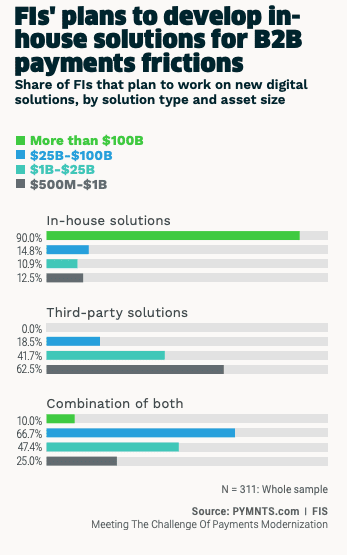

Different sized companies take different paths to reach similar destinations. While larger banks and FIs plan to do more with in-house teams, most respondents are using third-party expertise to bolster these efforts, ensuring that solutions align with market trends.

“Almost half of all FIs plan to address B2B payment frictions by developing in-house solutions in conjunction with adopting third-party solutions, while 35% plan to adopt only a third-party solution,” the study stated. “Smaller FIs — those with assets from $500 million to $1 billion — are the most likely to adopt only a third-party solution, with 63% saying they’ll take this route.”

Get the study: How Organizational Size Influences Innovation