With PYMNTS’ research finding that 70% of bridge millennials and millennials are now living paycheck-to-paycheck, some struggling with monthly bills and some not, these high-earning, high-spending cohorts like to finance purchases more than others — especially pricey items.

These exuberant spenders have a reputation for trying the new — even when the idea is something old like layaway, aka buy now, pay later (BNPL) — and we find a similar effect when looking at lease-to-own (LTO) financing trends in durable goods purchasing.

For “The Lease-To-Own Secret: Giving Consumers Control Over Durable Goods Purchases,” a PYMNTS and Katapult collaboration, PYMNTS surveyed nearly 2,700 U.S. consumers and found that many millennials and older bridge millennials see LTO as an attractive option today.

In fact, we found that these groups tick the right boxes for the LTO usage sweet spot.

Per the study, “age and income are two of the most significant determining factors influencing consumers’ use of alternative financing options for durable goods. Bridge millennials, millennials and Generation X consumers are the age groups most likely to finance all their purchases, with approximately 32% of respondents across these generations doing so.”

Alt-Fi Skews Young

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Credit cards are the No. 1 way that the average consumer buys a durable good, be it a bed or a cooking range, but certain demographics are developing a statistically significant familiarity and preference for shopping merchants that offer an LTO option.

For example, while LTO was the least common financing option used by respondents, we found millennials the most likely to use it for durable goods purchases, coming in at 23%.

In the research, there is an overlap between other forms of alternative credit favored by younger demos, showing both the appeal and utility of these novel financing types.

We found that 67% of LTO users and 57% of BNPL users could not have bought needed durable goods without access to these financing options, making the most common reason for accessing these options better management of personal finance.

Additionally, nearly one-third of respondents are somewhat interested in using LTO, with roughly half of millennials, bridge millennials and respondents with credit scores below 650 showing the highest levels of curiosity and intention behind LTO financing.

LTO or Off They Go

LTO or Off They Go

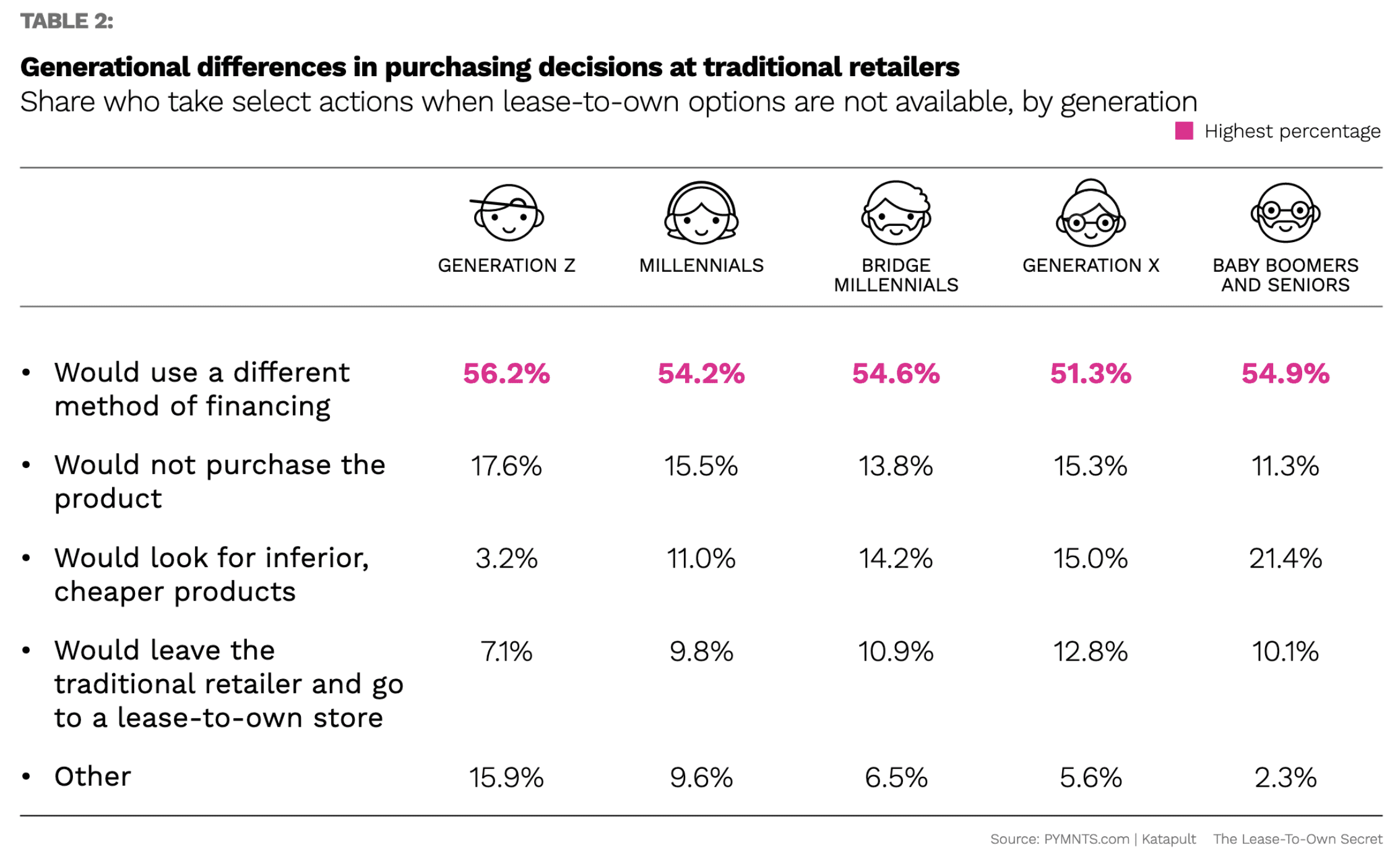

A fascinating aspect of LTO’s trajectory is the growing number of consumers — particularly younger demographic groups — who know about LTO and won’t shop where it’s not available.

According to “The Lease-To-Own Secret,” when LTO options are not present for specific durable goods, over half of consumers seek stores that have it, or abandon the purchase altogether.

The study found that 16% of respondents would not purchase a product without an LTO option, 10% look to cheaper substitutions and 10% seek a retailer offering lease-to-own.

That figure moves even higher among those with experience using lease-to-own, as 25% of that group will look for a retailer that offers this form of financing.

Read more: The Lease-To-Own Secret: Giving Consumers Control Over Durable Goods Purchases