Consumers have grown accustomed to the idea of low-friction digital payments and account transfers, and businesses that are not keeping up with the push for money mobility ubiquity risk frustrating customers and losing their business. Digital wallets and peer-to-peer (P2P) payment apps continue to grow as a regular feature of consumers’ everyday lives. A nearly endless set of options for financial servicers accounts, from banking to P2P apps, inundate these same consumers, and new account openings continue to rise.

At the same time, those new account holders expect that they should be able to move money between accounts they own just as easily as they split a bill with a friend using a P2P app. Delays in moving money into and out of bank accounts or digital wallets may encourage customers to start looking for an alternative account provider. Once they have finished making a transaction, consumers do not want to spend days waiting for it to go from “pending” to “complete.” Still, pulling together an effective solution that meets these expectations can be daunting without help.

The Money Mobility Tracker® explores consumers’ growing expectations for easy, frictionless money movement between accounts and how account providers can address these needs effectively.

Around The Money Mobility Space

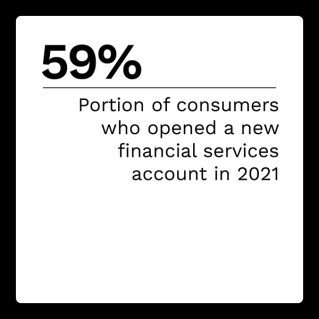

The rush of new account openings following the accelerated digital transformation accompanying the pandemic is showing no signs of slowing. U.S. consumers are projected to open 13 million new bank accounts this year. To capture those new account holders, account providers must ensure they have the features consumers want.

The rush of new account openings following the accelerated digital transformation accompanying the pandemic is showing no signs of slowing. U.S. consumers are projected to open 13 million new bank accounts this year. To capture those new account holders, account providers must ensure they have the features consumers want.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Around the world, the pandemic spurred a revolution in digital finance, with 40% of adults in low- and middle-income economies making electronic or card payments for the first time. As of 2021, more than three-quarters of consumers worldwide now have a bank or mobile money accounts, up from 68% in 2017.

For more on these and other stories, visit the Tracker’s News and Trends section.

Extend On Using Virtual Cards To Simplify Business Expenses

Despite the accelerated digital transformation, commercial finance is often still handled with multistep processes and slow approvals. Contractors and employees may have to cover significant expenses out of their own pockets and then wait some indeterminate period for reimbursement.

In this month’s Feature Story, Extend CEO and co-founder Andrew Jamison discusses his company’s efforts to develop a better solution for digitizing commercial expenses using virtual cards.

Keeping Pace With The Evolving Demands Of Money Mobility

With consumers increasingly turning to digital-first banking solutions, switching to a primary financial institution (FI) may be as easy as ordering a pizza through a mobile app. Opening an account may be easier depending on the account type and one’s dietary needs. In that environment, account providers cannot afford to fall behind or expect to keep customers once they are engaged with multiple products.

Meeting consumer expectations for easy, frictionless money movement between accounts — even those held at disparate FIs — is no simple task. Account providers have multiple rails and an ever-growing number of apps and digital wallets to ensure compatibility. Most will settle on some combination meant to appeal to the broadest range of customers. Not every account provider will have the means to go it alone, and partnerships may be a better fit than in-house solutions.

To learn more about the evolving demands of money mobility, read the Tracker’s PYMNTS Intelligence.

About The Tracker

The Money Mobility Tracker®, a PYMNTS and Ingo Money collaboration, examines efforts to meet consumer demands for better digital money mobility between accounts.