Money mobility ended 2022 as a serious problem for FinTechs and enters 2023 needing attention.

The FinTech Fraud Ripple Effect, a PYMNTS and Ingo Money collaboration, found that the average FinTech firm in the U.S. loses 1.7% of its total revenue to fraud each year, averaging $51 million in losses per firm. For many, this is an issue of not having the requisite tech.

The bigger the company, the higher the losses, as we found that the average large firm loses 1.4% of its revenue to fraud, or at least $159 million.

Fraud-fighting capabilities are critical to securing FinTech money mobility, and firms have investment decisions to make along these lines to improve the fraud loss figures.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

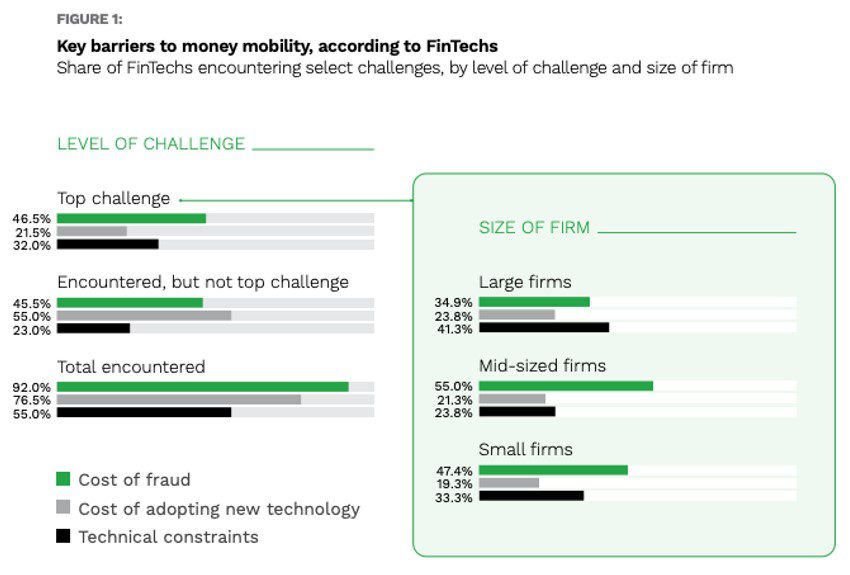

“Technical constraints, a category that includes both organizational constraints and regulatory requirements, are FinTechs’ second-most pressing issue, and 32% of firms cite technical constraints as their primary challenge,” the study said.

Additionally, “the more annual revenue a FinTech generates, the more likely it is to be limited by technical restraints. While 41% of large FinTech firms cite this as the most pressing challenge, just 24% of mid-sized firms and 33% of small firms agree. The cost of innovation can also impede progress, but it is the least common of these top three barriers to money mobility.”

Advertisement: Scroll to Continue

FinTechs employing more stringent fraud controls are less likely to report fraud losses or related issues. Among FinTechs that struggle with fraud, 19% said that their inability to guarantee deposits is the foremost factor limiting their money-in mobility, and 18% cited a general lack of convenience as such.

However, it’s important to note, as the study observed, that “these FinTechs were more likely to cite security barriers — such as security restrictions and authentication — as a barrier. This could signal that these FinTechs are consciously using tighter security measures to keep fraud at bay and that these measures could make it more difficult for customers to make deposits.”

See the Study: The FinTech Fraud Ripple Effect