Money-storing apps are going mainstream, and although PayPal leads in consumer popularity, financial institutions (FIs) may have a major opportunity to leverage the trust they have earned and build loyalty by providing their own options.

As noted in the most recent PYMNTS/Treasury Prime collaboration, “Money-Storing Apps Gain Favor With Customers,” 59% of customers have used these platforms for general-purpose or merchant-specific payments over the last 12 months. Those meant for general purposes and not tied to a merchant, such as PayPal, have picked up the most steam: 37% of customers who have stored money in any app in the past year have exclusively done so with general-purpose apps. This is more than five times the share that exclusively store funds in merchant-specific apps, and FIs, being merchant-agnostic, are well positioned to capitalize.

How Consumers Select a Money-Storing App

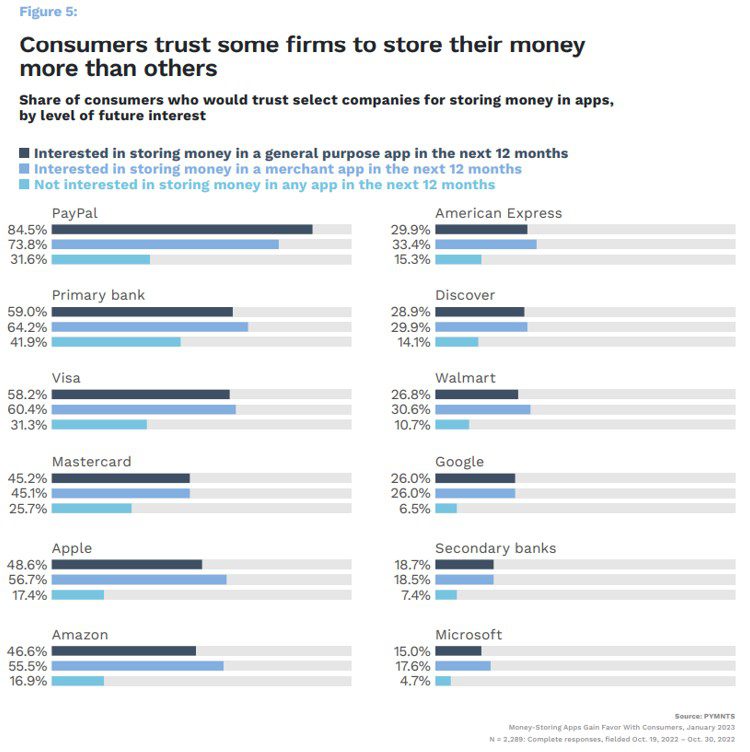

PayPal undoubtedly is customers’ current favorite when it comes to general-purpose money-storing apps, making it the platform to beat for the foreseeable future. Trust is a main driver behind customers’ decision on which app to opt for, our data finds, suggesting that banks — which often already have built long-term trust with customers — likely have room to maneuver into this space.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Overall, primary FIs lead all competitors except for PayPal in consumers’ likelihood to trust them as administrators of these platforms. PYMNTS’ research consistently notes the relationship between customer loyalty with FIs offering the right mix of engagement, real-time offerings and services. This consumer sentiment, therefore, can be tapped into by FIs to further win over customers.

An example of a combination that strikes it right, especially when it comes to attracting younger generations, typically includes a more personalized mobile experience — which may include tools like money-saving apps — and a balance of more traditional services and features. Two-thirds of customers are hesitant to switch from banks with brick-and-mortar locations due to the importance of in-person interaction.

Why Money-Storing Apps Have Money-Earning Potential

A reason that storing money in an app has gained rapid broad adoption within the past few years is that consumers generally seem to like the experience. Nearly 80% of consumers who have used general money-storing apps, for transactions ranging from P2P money transfers to digital purchases, are interested in using these apps again over the next 12 months — a statistic that suggests the apps have earned users’ approval.

Advertisement: Scroll to Continue

We found prior experience to be the biggest predictor of future money-storing app utilization: These consumers are five times more likely to use a money-storing app in the future than those who would be using such an app for the first time.

Digital offerings have translated into huge earnings for the biggest banks. Wells Fargo made up for its 3.7% dip in branch use with a 4% uptick in active mobile customers. Citi reported a 6% increase in active digital users up to 25 million, and the number of JPMorgan’s active mobile customers rose 9%.

The profitability of consumer-facing digital offerings is clear. Taking a cue from these industry giants, other FIs may well consider including money-saving apps as an up-and-coming portion of in their broader digital rollout strategies. Leveraging offerings that consumers will continually use and reuse could thus be the right move for FIs looking to increase customer loyalty and knock PayPal off its pedestal.