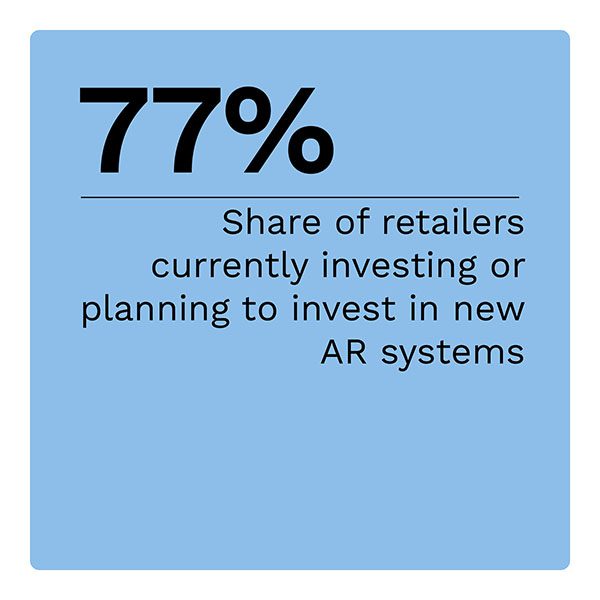

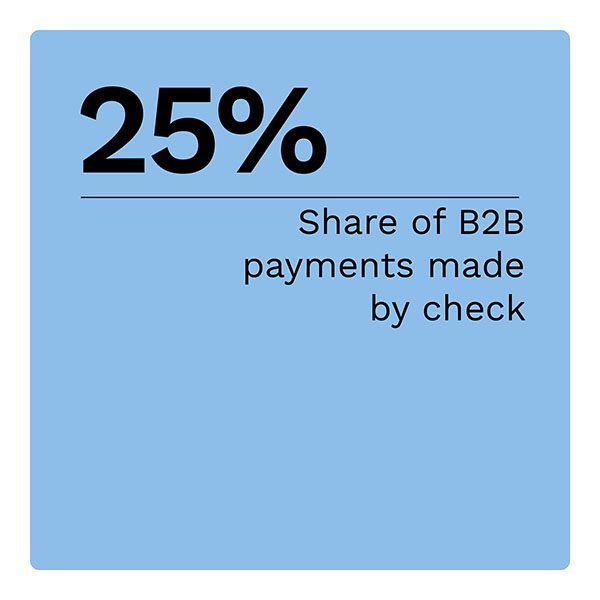

Merchants have gradually transitioned toward payment digitization for several decades, but these efforts have gained momentum in recent years. Companies are rapidly replacing legacy payment systems with more modern alternatives, which has impacted virtually every aspect of the business. For example, businesses are now making as few as 25% of business-to-business (B2B) payments by check, according to a PYMNTS survey, and many companies are investing or planning to invest in new accounts receivable (AR) and accounts payable (AP) systems to bolster their payment modernization efforts.

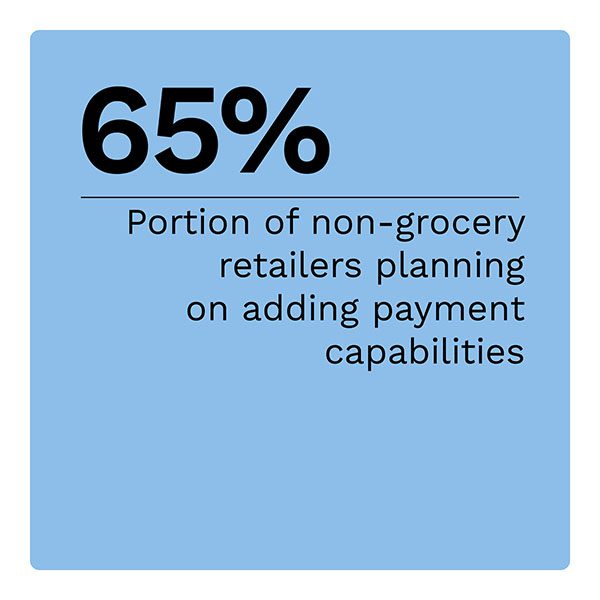

Merchants are also increasingly looking to enhance their digital payment capabilities for consumers. According to a PYMNTS report, 65% of non-grocery retailers are incorporating additional payment methods, while 55% and 56% of grocery and convenience stores, respectively, are also following suit. PYMNTS found that most companies have started accepting real-time payments or plan to do so, and many are looking at other business innovations, including loyalty programs and refund processes.

The “B2B and Digital Payments Tracker®” explores how the adoption of modern payment methods is accelerating and what benefits these payment modernization efforts can bring.

Around the B2B and Digital Payments Space

In 2022, the automated clearing house (ACH) network in the United States processed a staggering 30 billion payments totaling close to $77 trillion, according to a press release from Nacha. This amount marked a 3% increase in volume compared to 2021, much of it driven by increased use of Nacha’s faster payments option, same-day ACH. Business payments notably improved, with same-day ACH B2B transactions growing by 44% from the year prior.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Companies may want new payment options because they are increasingly frustrated with current business payment choices. A recent LexisNexis report found that 70% of corporations and FIs are unsatisfied with their rate of payment failures. For 64% of respondents, these failed payments have negatively impacted staff workloads. Failed payments also increased costs, with an average per-payment fee of $12.10 for unsuccessful payments.

For more on these and other stories, visit the Tracker’s News and Trends section.

An Industry Insider on Why Once B2B Goes Digital, It Won’t Go Back

Some business payment trends fundamentally change the landscape, while others falter and sometimes reverse. The movement of businesses’ payment digitization falls squarely into the first category.

To get the Insider POV, we spoke with Luke Trayfoot, chief revenue officer of Mangopay, to learn why companies are interested in B2B payment digitization and why this will be a permanent change.

Benefits Abound for Merchants Undertaking Payment Modernization

As the pandemic forced physical locations to close or impose restrictions on access, businesses had to pivot quickly to online channels and contactless payments to survive. The resulting digital transformation will continue because companies must embrace digital solutions to stay competitive, and these solutions can bring merchants significant advantages.

For example, payment digitization can potentially address the challenges associated with legacy B2B transactions. A PYMNTS survey found that small business payers encounter an average of five pain points when making B2B payments, with manual reviews and time-consuming procedures among the top concerns. Firms can alleviate these issues with modern payment systems, which helps explain why 92% of FIs are innovating or planning to innovate digital solutions to reduce B2B payment frictions.

To learn more about how modern payment systems can benefit merchants, read the Tracker’s PYMNTS Intelligence.

About the Tracker

The “B2B and Digital Payments Tracker®,” a collaboration with American Express, examines how adoption of digital payment methods is accelerating and what benefits these payment modernization efforts can bring.