The paycheck economy faces many challenges.

But a deeper dive into the data shows that non-paycheck-to-paycheck consumers — representing about 40% of the population — have bolstered their savings, shifted some spending habits, and padded their savings enough so their “state” is a relatively stable one, strong enough to keep their resilience, well, resilient.

The demographics and the data bear this out. PYMNTS has found that the average age of the non-paycheck-to-paycheck consumer is just under 50 years old, a bit more than the 47 years of age logged by the adult population.

There are some notable differences here. Those consumers not living paycheck to paycheck tend to be more highly educated than the general populace, where 43% of respondents have had at least some college education, compared to a third of the population at large.

A quarter of the non-paycheck-to-paycheck and the general consumer pool have incomes of at least $100,000 compared to 37% of the wider benchmark, which gives a nod to the fact that about half of all earners above $100,000 have been living paycheck to paycheck.

Drill down a bit though and there remains some evidence of the strength inherent in this group. About 41% are baby boomers and seniors, compared to a third for the sample. More than a third of the non-paycheck-to-paycheck stalwarts are millennials and Generation Zers. And as we’ve seen elsewhere, these are the generational cohorts who are adept at using credit to facilitate their everyday spend.

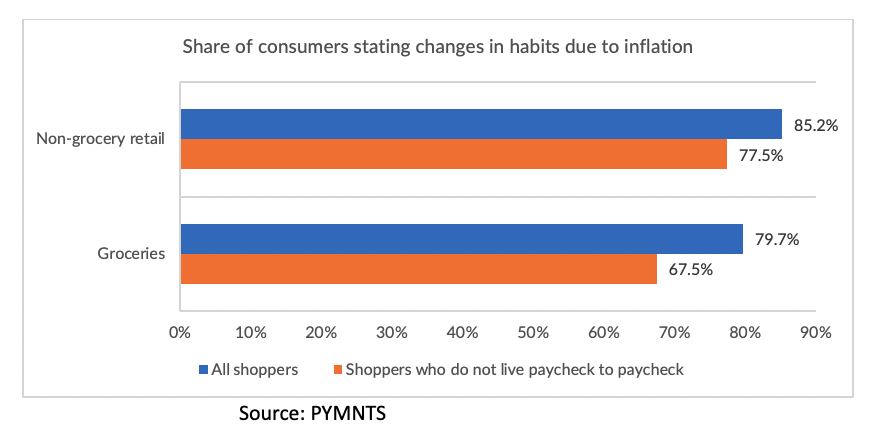

In reference to managing that everyday spend, most consumers — including the non-paycheck-to-paycheck segment — have fine-tuned their spending in reaction to recent economic headwinds due to recent inflation. However, fewer of those not living paycheck to paycheck have adjusted how they spend their money during this time.

PYMNTS found that there are three basic ways in which consumers have been reacting to inflation. They can reduce the quantity of items bought, they can shift to cheaper merchants, or they can reduce the quality of products that are bought. And there can be a strategy on hand that incorporates any combination of those tactics.

The data shows that only about 10% of non-paycheck-to-paycheck consumers changed all three habits when it came to retail spending; roughly the same percentage of respondents said the same about groceries. And when it came to, say, dining out, fewer non-paycheck-to-paycheck respondents said they were purchasing less from restaurants, at 41%, than the 50% seen in society at large.

The data shows that only about 10% of non-paycheck-to-paycheck consumers changed all three habits when it came to retail spending; roughly the same percentage of respondents said the same about groceries. And when it came to, say, dining out, fewer non-paycheck-to-paycheck respondents said they were purchasing less from restaurants, at 41%, than the 50% seen in society at large.

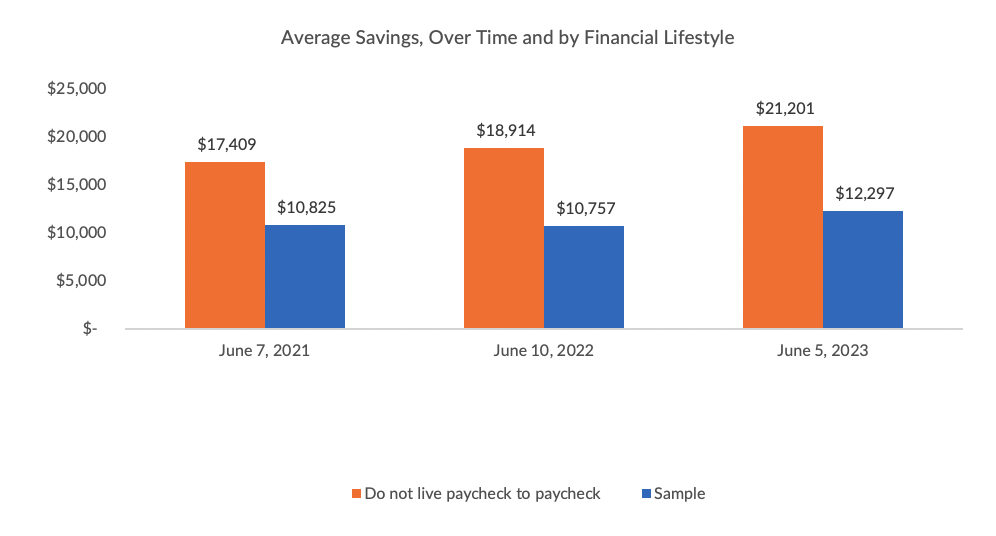

The dry powder seems to lie with the savings cushion built up. The average savings over time has been bulked up for the consumers who are not stretching to make ends meet — to a whopping $21,000 versus around $17,400 a few years ago. That’s a 21% jump where the rate had been 13% for all consumers. And it may be the case that the non-paycheck-to-paycheck consumer keeps the economy chugging along.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More