Fraud schemes are evolving alongside technology, becoming more sophisticated and mutating to exploit vulnerabilities within financial institutions.

In fact, fraud incidents increased by 13% in the past year, with FinTech companies being the most likely financial entities to report higher fraud losses, according to the “The Path to FinTech Profitability Must Be Fraud-Proof” report by PYMNTS Intelligence in collaboration with Sezzle.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Apart from financial losses — the cost of fraud is listed as the top challenge by nearly half of all FinTech firms — fraud schemes also pose reputational risks, regulatory penalties, legal costs and loss of business revenues, creating a complex web of challenges for businesses of all sizes to navigate.

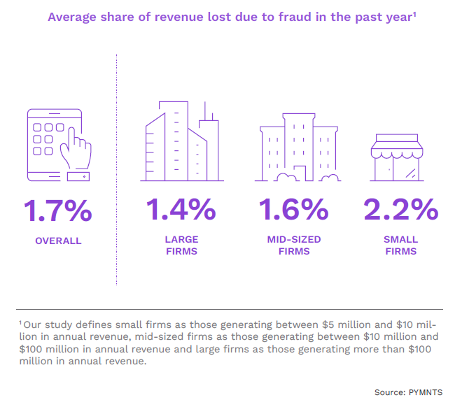

The impact of fraud varies inversely with the size of the FinTech company, however. As noted in the study, small firms suffer 57% more revenue loss to fraud than large firms, with an average annual loss of 2.2% of their revenue, equivalent to $200,000 on average. Mid-sized firms also experience higher fraud losses compared to larger firms.

As fraud threats continue to evolve, FinTech executives anticipate an increase in all types of fraud this year and plan to expand their budgets for fraud prevention management initiatives, with a particular focus on automated technology capable of combating deepfakes.

FinTech firms are increasingly leveraging artificial intelligence (AI) and machine learning (ML) solutions. These technologies enable quick processing of large quantities of data, allowing for the identification of patterns and aberrations in identity verification processes.

Advertisement: Scroll to Continue

AI and ML solutions can also adapt to fraudsters’ ever-evolving techniques, as noted in separate research by PYMNTS. These solutions can help FinTechs in recognizing and analyzing prevalent fraud patterns, offering them a standardized and comprehensive perspective on fraud dynamics. Moreover, proactive, automated fraud solutions powered by AI and ML have the potential to reduce revenue losses compared to reactive, manual solutions.

Overall, the fraud detection and prevention market is projected to reach $90.07 billion by 2030, with fraud analytics and identity theft segments predicted to witness the highest growth.