In the Finances Deep Dive Edition of “New Reality Check: The Paycheck-to-Paycheck Report,” PYMNTS Intelligence draws on the insights from a survey of over 4,600 consumers to examine the impact of household composition on consumers’ ability to manage expenses and put aside savings.

According to findings detailed in the joint PYMNTS Intelligence-LendingClub study, nearly 90% of consumers cohabit with others, and a third of those living paycheck to paycheck reside in households of four or more people. Non-paycheck-to-paycheck consumers often live in two-person households (41%).

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Across demographics, millennials (49%) and bridge millennials (55%) predominantly live in larger households of four or more people, marking these age groups as the most inclined toward larger living arrangements. Urban residents also tend to have slightly larger households, with 39% living in households of four or more people, compared to suburban or rural consumers.

The correlation between household status, life stage, and financial standing becomes more apparent when observing consumers who choose to reside with family members. Gen Z individuals residing with three or more people allocated 22% of their income to housing, whereas those living alone or with a partner spent 30% of their income on housing expenses.

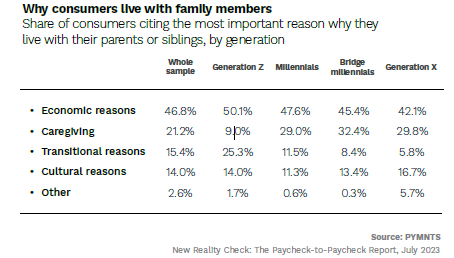

Additionally, Generation Z represents the demographic most likely to live with family members, at 58%, primarily driven by economic reasons such as the high cost of housing and the desire to save money. Generation Z’s choice to live with family members is influenced by various factors beyond economic reasons. Transitional motives, cultural considerations, and caregiving responsibilities also play a role, cited by 25%, 14%, and 9% of consumers within this age group, respectively.

Advertisement: Scroll to Continue

Overall, nearly half of consumers living with family members are most likely to cite economic reasons for doing so, followed by 21% of individuals, mainly from among older demographics, citing caregiving as their motive.

In terms of gender, adult males (20%) are slightly more inclined to live with parents compared to females (18%), especially among those struggling financially. Among cash-strapped individuals, 26% of males reside with parents or siblings, while only 18% of females do the same.

Examining the data further shows that couples or individuals living with a partner or spouse generally have a stronger financial footing, but the responsibility of raising children can strain their finances. This can be attributed to shared expenses and the need to cover essential and discretionary spending. Furthermore, consumers living with a partner or children are more likely to have auto loans or mortgages, indicating their commitment to long-term financial obligations.

In conclusion, understanding the financial dynamics of different household compositions is key. And by recognizing the challenges faced by specific demographics, individuals can make informed decisions regarding their financial well-being. Policymakers can also use this information to develop targeted strategies to address the financial struggles experienced by certain groups.