Lagging in digital innovations poses a risk of losing some members, and while they probably were aware of that, perhaps they didn’t have data to prove it. But now, according to PYMNTS Intelligence data, this number may be as high as 27% of the CU members.

According to a PYMNTS Intelligence research study in collaboration with PSCU, “Credit Union Innovation: Staying Ahead Through Payments Innovation,” 27% of clients from CUs say they would consider changing financial institutions (FIs) to access new products. The data doesn’t specify whether switching to a new FI means a FinTech, a bank or simply to another CU that supplies more innovative products, but the fact is that less innovation may translate into losing members.

This willingness to switch has increased to 27% up from 17% since 2018. Brian Scott, chief growth officer at CU service organization PSCU, shared his view on this risk in a interview with PYMNTS: “A lot of financial institutions have pulled back a little bit on innovation, kind of taking that wait-and-see approach. And I’d say just the opposite. Now is a great time to double-down on the innovation.”

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Today, the share of CU members willing to switch for more innovative solutions is very close to the number of non-CU members willing to do the same, 29% as per PYMNTS Intelligence research.

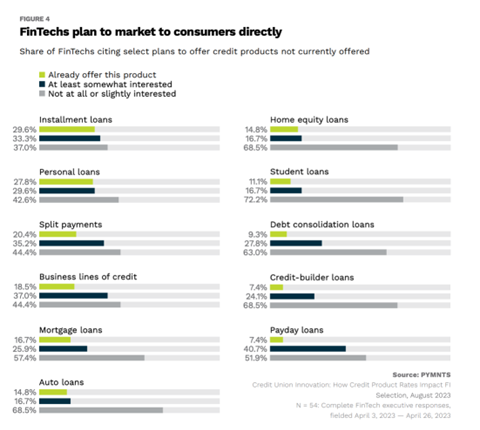

CUs have remained relatively stable in the variety of credit products they have offered their members over time. Meanwhile, FinTechs and digital banks are moving fast in product innovation to capture this opportunity.

Advertisement: Scroll to Continue

For instance, most CUs have no immediate plans to offer installment payment plans such as BNPL, which FinTechs are already capitalizing on. According to another PYMNTS Intelligence study in collaboration with PSCU, 37% of FinTechs plan to offer business lines of credit directly to end customers for the first time, and 41% plan to offer payday loans, just to cite couple of examples.

In addition to product offering, consumers also value the speed with which funds become available after applying for a credit product. Thus, reducing the time between application submission, approval and availability of funds could draw consumers to an FI.

Six out of 10 CUs believe that product setup times are highly influential in consumers’ decisions to apply for credit products. While CUs have made progress in reducing setup times for many of the products they offer, they are losing ground versus other FIs that have shown an inclination to invest in technology to provide installment payment products like BNPL to consumers.