Account-to-account (A2A) transfers, also known as pay-by-bank, have emerged as a convenient alternative to traditional transaction methods like credit and debit cards.

By transferring money between bank accounts, this payment method bypasses traditional card networks, providing a more direct and cost-effective way to facilitate transactions.

According to Chris Jameson, managing director and head of GTS product management EMEA at Bank of America, the payment solution is enabling quicker and more secure payment processes, allowing online shoppers to instantly pay from their bank accounts without the need for credit or debit card information.

[It’s] an alternative to cards,” explained Jameson during an interview with PYMNTS in March. “The payment will actually come from the consumer’s bank account through various API calls rather than going through the card rails.”

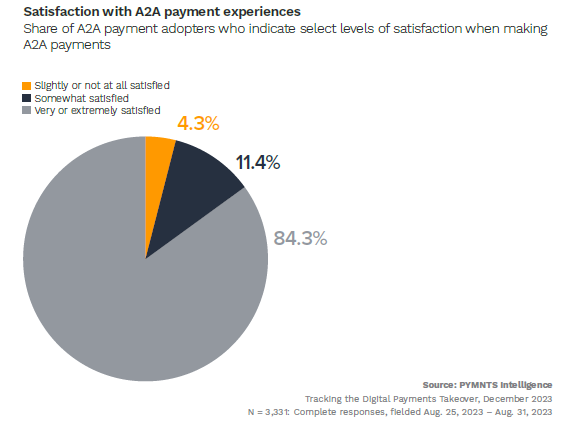

Convenience stands out as the primary driver behind consumer satisfaction with A2A payments. Per findings detailed in the study “Tracking the Digital Payments Takeover: Consumer Familiarity Controls Account-to-Account Payment Growth,” a PYMNTS Intelligence and AWS collaboration, 84% of users reported being very or extremely satisfied with their most-used A2A payment platform.

“This could be attributed to these platforms’ success in making the payment experience not just seamless but also part of an ecosystem where users frequently interact and transact,” the study noted. “Because consumers complete many of these transactions within a known network — sending money to the same recipients — the comfort and trust levels are higher, reinforcing platform loyalty.”

Another convenience factor that enhances satisfaction with A2A payments, especially in eCommerce, is the swift refund process, said Jameson. A2A payments occur instantly through API calls, whereas refunds for items purchased with a card often involve waiting several days for the money to reflect on the card.

As Jameson highlighted, when you buy something online and go into the store to return it, you’ll likely be told to expect a “refund to your card in the next seven to 10 days. Whereas with pay-by-bank, [you will be] standing in the store and seeing the money hit your account straight away.”

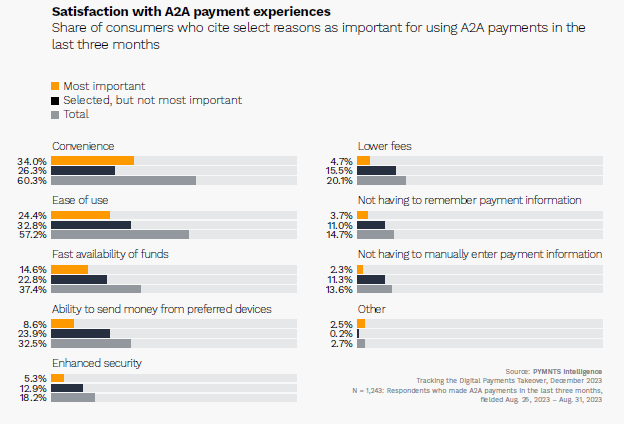

Other factors also impact consumer satisfaction with A2A payment experiences, including ease of use, prompt availability of funds and the option to transfer money using preferred devices.

Per the data, close to 60% of consumers reported ease of use as important, nearly 40% of consumers prioritized swift access to their funds, and 33% deemed the use of their preferred devices essential when choosing A2A as a payment method.

Additionally, approximately one-fifth of consumers emphasized the significance of heightened security when opting for A2A payments — an added advantage over traditional card-based payment methods.

“With pay-by-bank transactions, you don’t have to hold a customer’s [card] information,” Jameson pointed out, removing the need to store extensive consumer data and alleviating both the expenses and liabilities linked to preserving card information, applicable even for card acquirers and issuers.

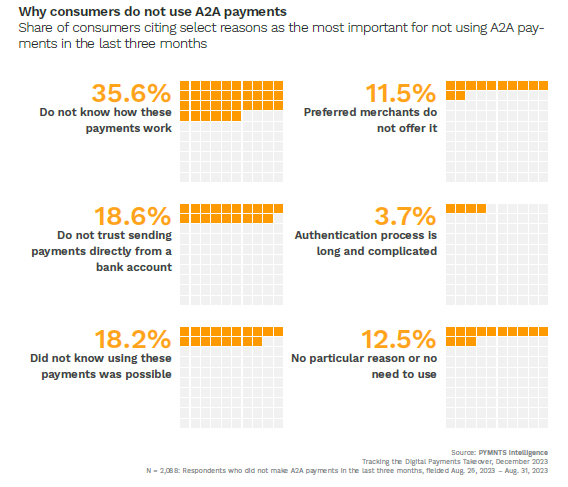

Despite these benefits, the survey found that widespread A2A adoption is still lacking. This is because nearly 40% of consumers, primarily baby boomers, admitted to not understanding how A2A payments work, and another 24% were unaware that this option existed.

To tackle this issue, comprehensive awareness campaigns are needed to educate consumers about the benefits and process of A2A payments to counter reservations. Moreover, targeted campaigns that include monetary incentives, such as discounts, rewards, or exclusive offers, could be effective in capturing the interest of consumers, the study stated.

However, it is important to note that incentives alone may not convince all consumers. The data showed that about one-fifth of consumers cited security concerns as a deterrent for adopting A2A payments, “suggesting a broader need for more detailed communication on the robust security frameworks that many A2A platforms now employ.”

By addressing these barriers, A2A payments have the potential to reshape the payments landscape, offering simplicity, convenience and potential rewards for consumers.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More