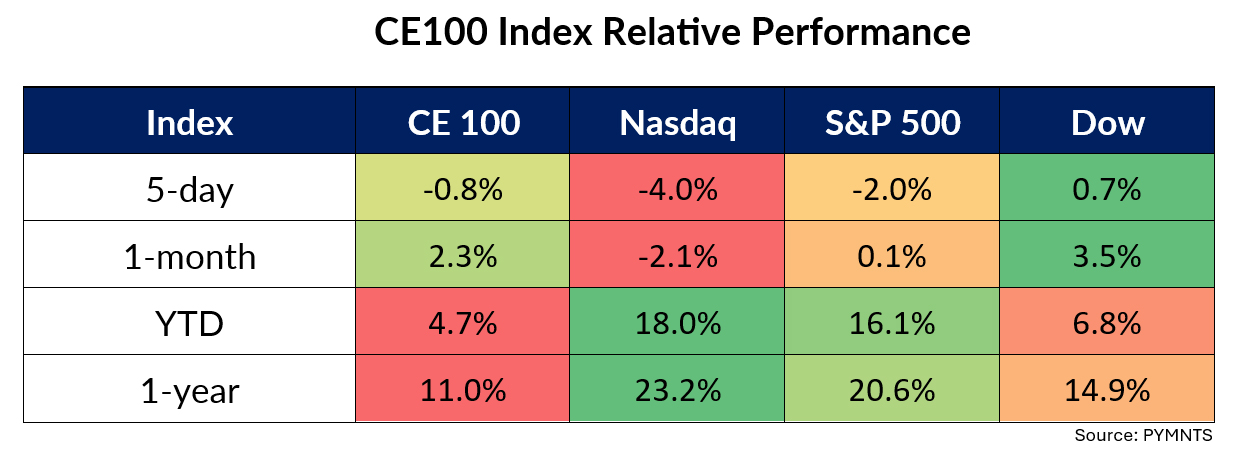

Of course, CrowdStrike was the focus here, as its shares plunging nearly 18% on the week led the Work segment 1.5% lower.

Banks, airlines and nearly any and every business relying on a Microsoft Windows computer system found themselves grappling with a massive disruption, PYMNTS reported.

As of late afternoon Friday, what was being called “the worst IT outage in history” was still rippling through various systems. The outage was tied to a software update issued by security firm CrowdStrike that inadvertently took down Microsoft’s systems. CrowdStrike software is used by over half of Fortune 500 companies.

Domino’s slid roughly the same amount during the week, by about 17%, and the Eat pillar was down 2.7% through the week.

As reported during the company’s most recent earnings, CEO Russell Weiner shared that loyalty reward redemptions for pickup orders have skyrocketed since the brand refreshed its program last fall.

Advertisement: Scroll to Continue

“Consumer spending [is] slow, but let’s think about what’s happened with that as a backdrop. We’ve grown orders in our delivery business, our carryout business, every income cohort,” Weiner said. “We’ve grown order count in international. [That’s] what’s going on in an economy where folks are maybe struggling to decide what to buy.” U.S. same-store sales growth came in at 4.8%. Analysts expected growth of 4.9%, as reported by The Wall Street Journal.

These losses were more than enough to offset the 2% rally in the Bank sector.

Banks Weigh in on Consumer Spending

Goldman Sachs shares were 3.8% higher. Drilling down into the data, the company’s credit card balances, up 11% year over year to $19 billion, remain somewhat even with the first quarter, while management said on the conference call with analysts that they were “pleased” with the card performance.

Charge-offs of 8.4% for consumer loans have been consistent with recent quarters. The overall provision for credit losses in the quarter stood at $395 million, down 27% year over year, reflecting the card business (the wholesale loan charge-offs, according to the data, stand at 0%).

Within its platform solutions segment, consumer platforms delivered 4% growth to $599 million in revenues, which reflected higher average credit card balances, though results were offset by the GreenSky transaction.

American Express pushed ahead with a 5% gain this week, but the Pay and Be Pay segment slipped 1.3%. American Express earnings released on Friday indicated that consumers continue to spend on experiences — particularly dining out — and that momentum belongs to the younger generations who are using their cards more often.

Spending by millennial and Gen Z customers was up 13% year over year, management said.

CFO Christophe Le Caillec said on the conference call with analysts that spending growth was visible across several categories. Spending on goods and services was 6% higher, and travel and entertainment-related spending grew 7%.

“We did see some slower growth in certain [travel and entertainment] categories versus the prior quarter, especially in airline and lodging,” he said. But spending at restaurants, he said, “remained strong.”

As for using the cards more often, the company’s transaction growth was 9% higher in the June quarter vs. last year.

BNPL providers such as Sezzle rocketed ahead by 66%. As reported this past week by PYMNTS, Sezzle has added Spanish language capability to its buy now, pay later (BNPL) app and checkout. This capability is meant to appeal to the 40 million Americans who speak Spanish, the company said in a Tuesday release.

Affirm shares lost nearly 10%.

In general news tied to the BNPL space, the Consumer Financial Protection Bureau’s (CFPB) rule classifying BNPL as credit card providers takes effect July 30, meaning these firms must provide legal protections and rights delivered by conventional credit cards.

A letter this week from the American FinTech Council (which, among other enterprises, represents BNPL providers) to Rohit Chopra, director of the CFPB, asked that the rule become effective next year, not this month.

In the letter, the Council argued that “given the complexity and variation in business models, lender practices, and partnerships with merchants, as well as differences in the levels of preexisting compliance with the provisions enumerated in the Interpretive Rule by BNPL lenders, it seems prudent to adopt an extended compliance period. Therefore, AFC recommends extending the effective date of the Interpretive Rule from its current date of July 30, 2024, to January 1, 2025.”