Through the past few years, consumers in the United States, have collectively seemed to be an unstoppable force.

They have spent through inflationary times, geopolitical uncertainty and while living paycheck to paycheck.

There are signs, however, that the momentum may slow headed into the last few weeks of the year, which are a critical time for commerce and retailers, especially.

The National Retail Federation estimated that holiday sales in November and December accounted for about 19% of total retail sales over the last five years.

Last week, Target threw some cold water on the notion that consumer spending travels in one direction (namely, upward). During the company’s third-quarter earnings call Nov. 20, CEO Brian Cornell said, “consumers tell us their budgets are being stretched. They’re becoming resourceful, focusing on deals, then stocking up when they find them. Consumers allow themselves to splurge a little bit when they find the right item.”

The stocking up that Cornell referred to may imply that many consumers have already bought what they needed to buy. If it’s deal-chasing for the sake of stocking up on essentials or if it’s the same pursuit but for gift-giving, the read-across is that sales have been pulled forward in some respect, leaving less financial firepower to spend in subsequent weeks.

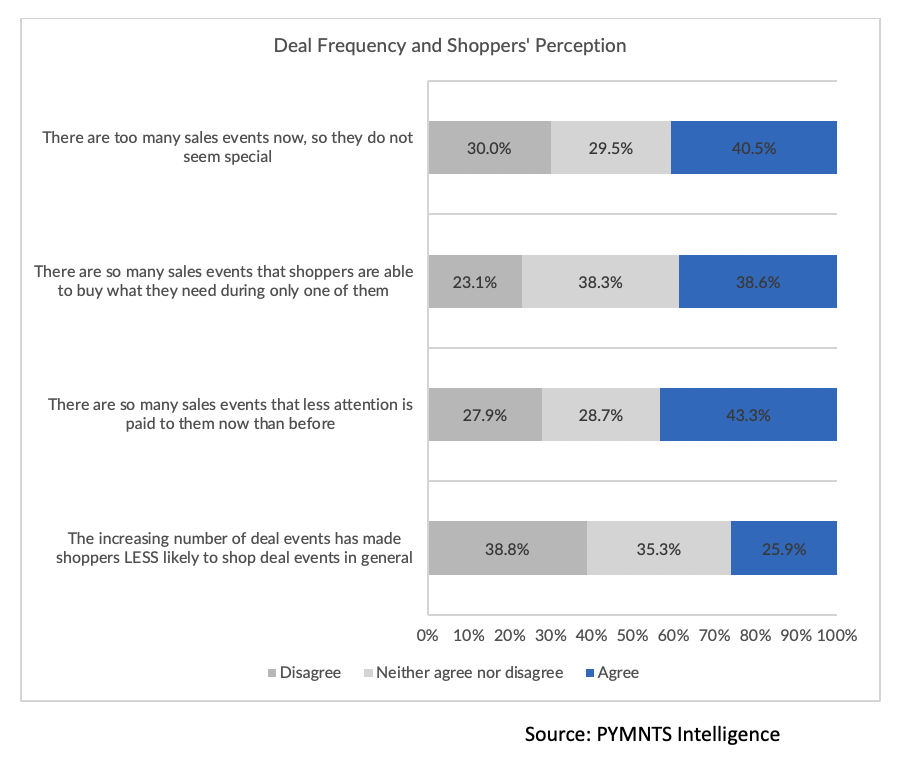

The PYMNTS Intelligence report “Intrigue or Fatigue? Amid Crowded Deals Landscape, Financial Lifestyle Drives Consumers’ Black Friday Interest” found that one-third of consumers said they feel like they are being “bombarded” by sales promotions. Forty-one percent said the increased frequency makes the deals feel less special.

A quarter of consumers said they are less likely to shop at deal events this year, in general. Thirty-nine percent said they are somewhat or much more likely to wait this year than last to buy a product they immediately need. A roughly equal share reported being more likely to wait this year to buy products they want but do not urgently need.

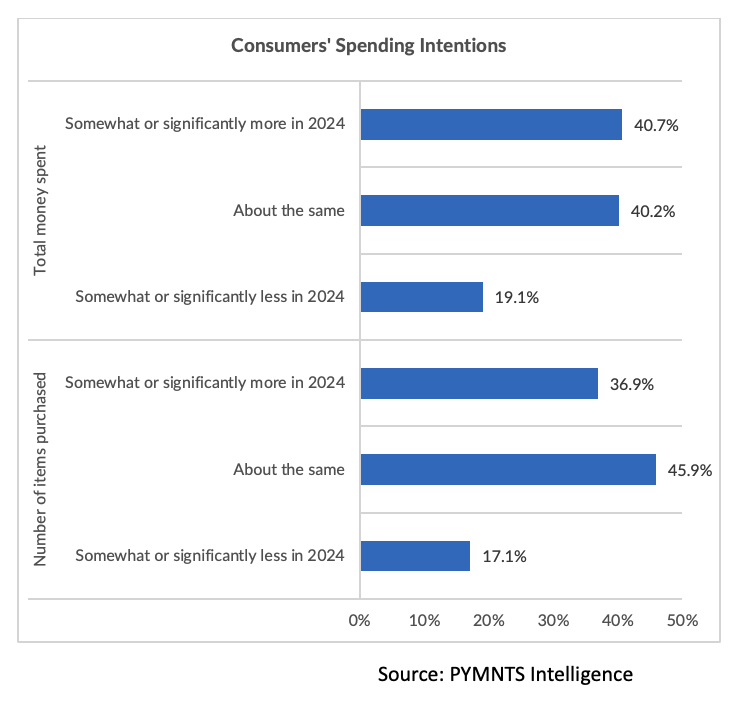

There’s also the push and pull of inflation, which erodes the purchasing power of every dollar held by the consumer. Roughly 59% of consumers said they will either spend the same amount or less than they did last year. Fifty-three percent said they would buy the same or less, in terms of the quantity of items.

The impact of strained finances may show up at the register in the next few weeks. Thirty-nine percent of consumers said they feel they must only shop at one big sales event to get what they need. That signals a one-and-done mentality that gives retailers a limited amount of runway to engage with shoppers.

The impact of strained finances may show up at the register in the next few weeks. Thirty-nine percent of consumers said they feel they must only shop at one big sales event to get what they need. That signals a one-and-done mentality that gives retailers a limited amount of runway to engage with shoppers.

None of this is to say that holiday magic won’t happen at in-store and online retailers. The wait-and-see approach might translate into a flurry of gift-giving.

However, as PYMNTS Intelligence found, 52% of financially stable consumers (those without issues paying bills and who don’t live paycheck to paycheck, which is one-third of consumers) shopping fewer sales said deal fatigue is a key factor in shifting to either purchasing the same amount or even spending less. This share is higher than the 40% sample average among all consumers shopping fewer sales who said the same.

Even one-third of consumers who earn more than $250,000 annually live paycheck to paycheck. A quarter of the paycheck-to-paycheck population has difficulties paying bills, and they carry average credit card balances of $7,000, higher than the sample average of roughly $5,700.

Credit may not be the lifeline to retail sales that some merchants might hope. We’ll see if waiting translates into pent-up demand in the weeks ahead.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More