Black Friday’s in the rearview mirror. Cyber Monday is here.

Part of what incentivizes a consumer to buy is if and when their preferred payment method is available. It’s a testament to the power of choice and control (on the part of the shopper) that if they can’t pay the way they want to pay, they’ll hold off or go somewhere else to get what they want. Payments, then, become a competitive advantage.

For buy now, pay later (BNPL) providers — where paying over time has been gaining adherents through the past few years — there are some headwinds in brick-and-mortar settings. Simply put, shoppers online seek out BNPL, which may determine whether they seal the deal.

But in stores? Well, there’s a bit of a substitution effect. They may go ahead and buy, anyway, with a different payment option, or shift to a cheaper item. What’s lost at the (physical) register is the chance to more firmly entrench BNPL with the consumer.

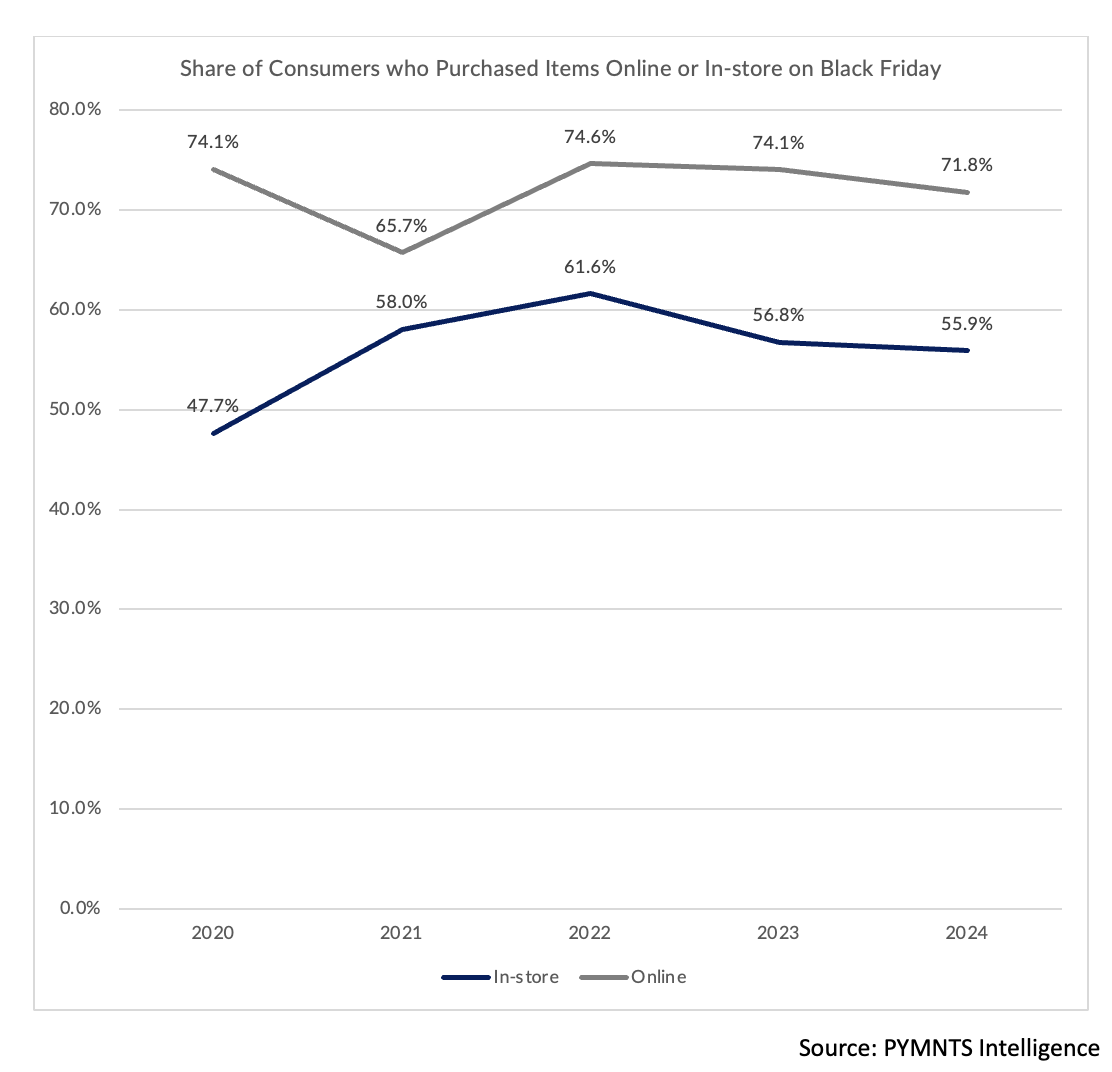

PYMNTS Intelligence found this past weekend that more people shopped on Black Friday than last year, which widened the pool of consumers who potentially would use BNPL. The data shows that 62% of U.S. consumers made at least one purchase on Nov. 29, representing a jump from 53% in 2023.

Drilling down into where the 2,800-plus individuals we surveyed shopped, we found that 72% of consumers went online; while roughly 56% of individuals shopped in-store. Only 28% of shoppers went exclusively into the stores, in person, to shop.

Advertisement: Scroll to Continue

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

It’s important to note how consumers used the tactile, in-store setting this past Friday: They supplemented their online spending with trips to the store. That means that the “main” conduit for commerce was the online channel. And we found, too, that although BNPL options still are a relatively small percentage of transactions, they are highly valued. The Black Friday data shows that shoppers who used BNPL spent more on average than others using credit or debit cards.

As for the actual spending: Consumers who do not live paycheck to paycheck spent the most this past Friday, overall, at $376.17. Those living paycheck to paycheck without difficulties paying their bills averaged a roughly similar $351.12. Paycheck-to-paycheck consumers who struggle to pay bills spent the least but still averaged $282.81.

Looking at the Total Budget

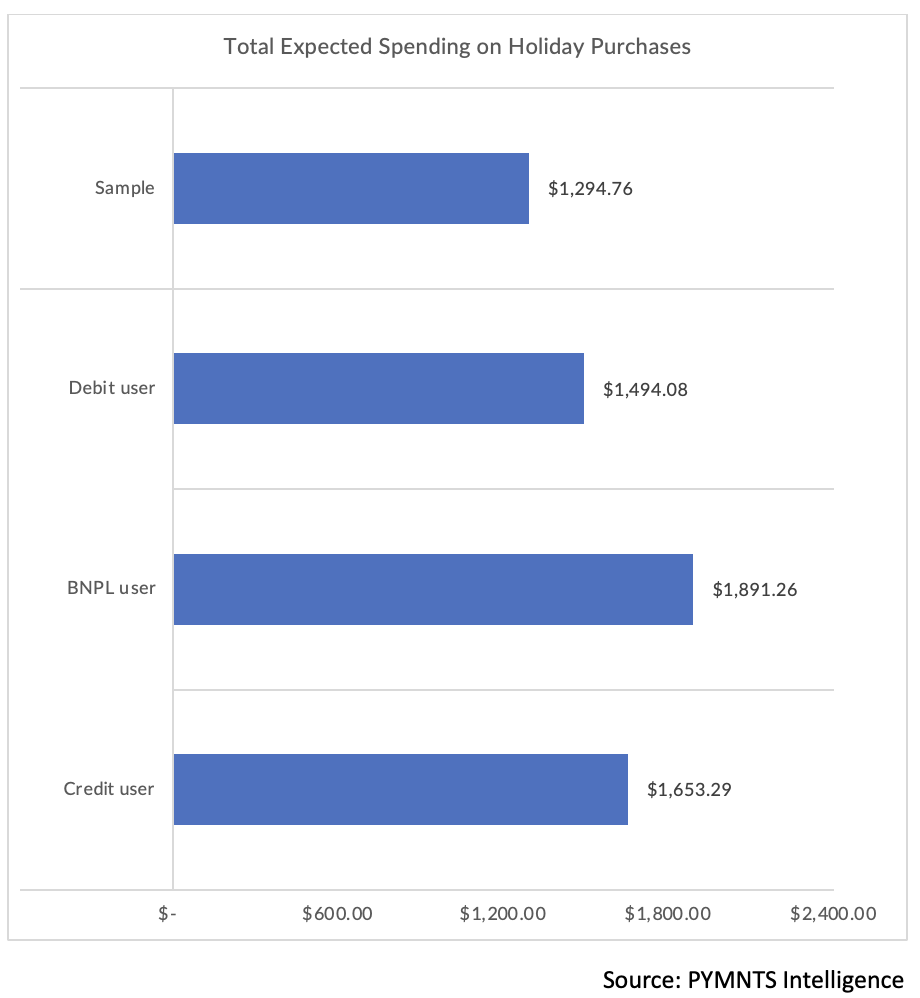

Of course, the shopping season is not over yet, as it stretches well into the next several weeks. The chart below notes the “total” amount that individuals have earmarked for the entire season we see that BNPL users are aiming to spend a bit more than customers who opt for debit and credit.

BNPL purchases accounted for 7.4% of in-store transactions, trailing the 10.1% tally seen with online transactions. Given the fact that so much more commerce has been done online than in person, BNPL has seen higher volumes as measured against total spending.

Sentiment Around BNPL

Consumer sentiment hints at the fact that BNPL is facing headwinds in store. The chart below notes that if the pay later option they used were not available, 21% of consumers in-store would go ahead and make the purchase anyway, while 13.6% would move towards a cheaper product. Conversely, only a respective 16.6% and 9.9% of online shoppers said the same. Meanwhile, 12% of digital shoppers said they’d outright not make the purchase, compared to 7.9% in-store.

The read across here is that online (which, again, has been a preferred channel for a super-majority of consumers), if consumers don’t have the pay-over-time choice they want, they may skip the sale entirely, conceivably moving to a different merchant.

In-store, there’s less of a competitive differentiator with BNPL: The consumer is less inclined to delay or nix the transaction if they can’t use their first choice in the aisles — even as paying over time has garnered a smaller share of in-store transactions anyway. In addition, there are some indications that were BNPL not available in-store, at least some consumers would move to payment options that are, arguably, less optimal choices — such as payday loans (which might carry high interest rates) or even overdraft tied to their bank accounts (when those accounts are overdrawn).

BNPL’s a winner online, and seemingly a bit of a work in progress in face-to-face commerce, at least for the moment.