GDP was better than expected, and it’s almost always the case that GDP’s direction rests firmly on the shoulders of U.S. consumers’ spending, which accounts for roughly 70% of the figure.

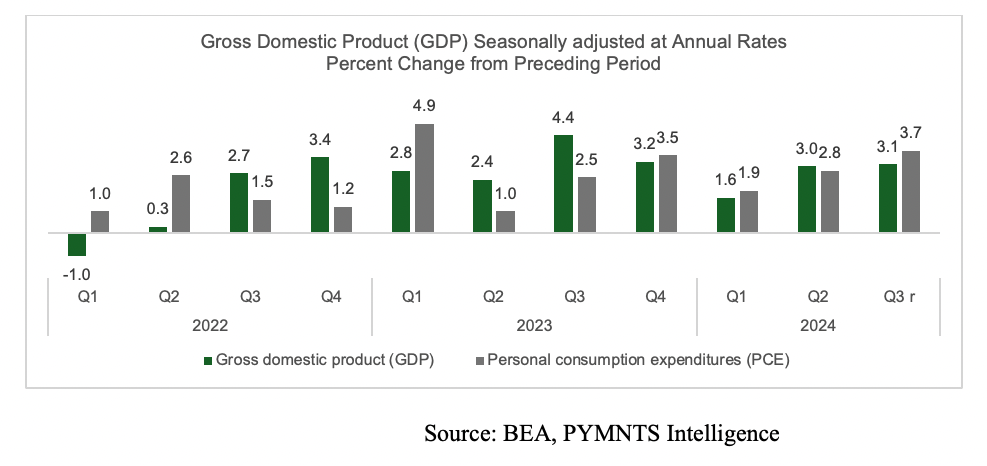

GDP increased at a 3.1% annualized pace in the third estimate by the U.S. Bureau of Economic Analysis, up from the second estimate of 2.8%. The pace was up from the second quarter of this year at a 3% annualized growth rate. Consumer spending, as measured in the personal consumption expenditures metric, was up 3.7%, annualized.

The PCE price index — a measure of inflation — rose by 1.5% in Q3, continuing its downward trend from 2.5% in Q2 and 3.4% in Q1. This slowing rate of inflation suggests that some of the earlier pressure points, such as supply chain disruptions and elevated commodity costs, have eased.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Disposable Personal Income Growth Lags Outlays

However, disposable personal income, the measure of what consumers have on hand to spend on goods in services, continued to grow at a pace that was outmatched by inflation and spending. The data showed that household disposable personal income increased by 1.1% in Q3, higher than the 1% increase seen in Q2.

If prices and spending rise more quickly than income, then the logic follows that consumers save less. This is borne out by the latest data, where the personal saving rate settled at 4.3%, down from 4.9% in the previous quarter.

Advertisement: Scroll to Continue

The PYMNTS Intelligence report “Paycheck-to-Paycheck Consumers Continue to Struggle With High Interest Rates” found that coming into September, the last month of the third quarter, struggling paycheck-to-paycheck consumers — who account for 23% of the population — averaged $2,447 in savings, while those living without difficulty averaged $7,558. Fifty-one percent of paycheck-to-paycheck consumers struggling with monthly expenses had no readily available savings.

In the meantime, the latest retail spending data showed that the savings rate may see further pressure, while credit cards continue to be a key means of spending into the holidays. Meeting monthly debt obligations means that there’s even less disposable income to set aside.

November’s consumer spending was buoyant, as eCommerce sales rebounded from a tepid pace in October. Census Bureau data released this week indicated that overall retail sales surged 0.7% in November, ahead of the consensus of 0.6% gains month over month and quickening from October’s newly revised 0.5% pace (up from the previous 0.4% report).

The average credit card debt, as measured across all PYMNTS survey respondents, was over $5,000, but struggling paycheck-to-paycheck consumers are carrying balances of $7,000. In addition, 41% of financially struggling cardholders often or always reach their card limits. They are more than six times as likely as financially stable consumers to do so.