The rise of the gig economy exposed an issue that had plagued freelancers for ages: past-due invoices and cash flow. PYMNTS’ Gig Economy Index found that 84.5 percent of existing freelancers say they would do even more freelance work if they were paid more quickly.

Problems getting paid aren’t just a part of life for independent contractors – they also affect businesses of all sizes. And those unpaid invoices add up.

According to PYMNTS’ Trade Credit Dilemma Report, the value of outstanding invoices in the U.S. equals $3.1 trillion on an average day. How did extending trade credit to buyers become such a costly way of doing business?

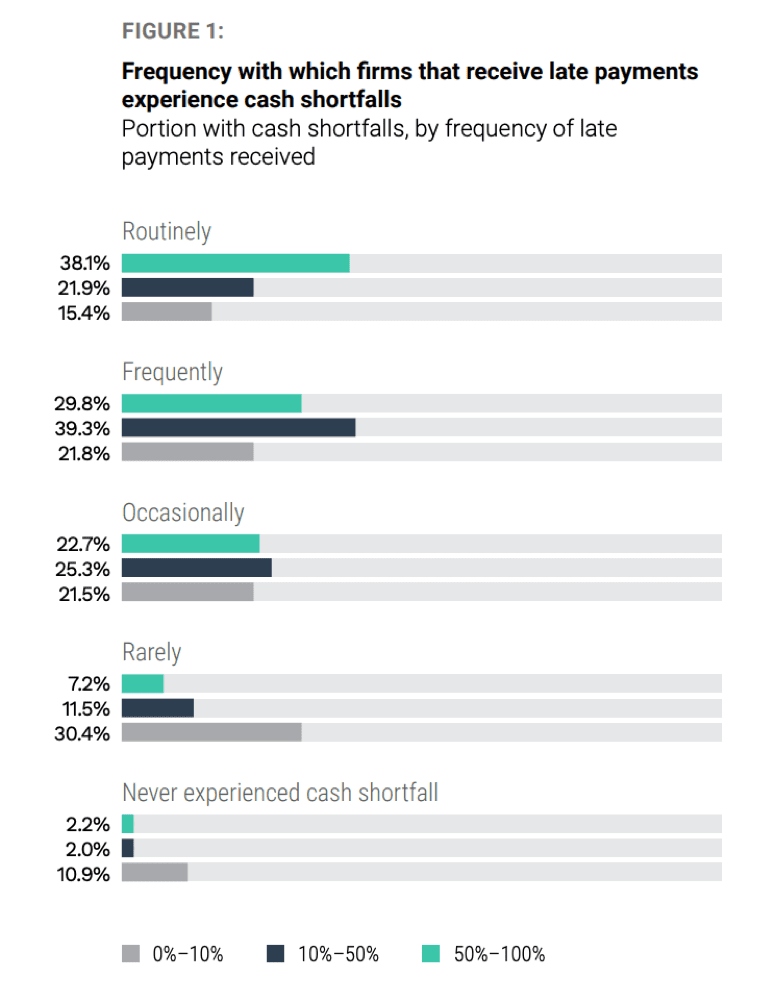

Late payments create a vicious cycle; 67.9 percent of firms that receive more than half of their payments late report experiencing cash flow problems.

While an average of 13.2 percent pay their suppliers late on average, 27.5 percent of those who frequently receive late payments do so in turn.

Additionally, 38.1 percent of firms that receive at least half of their payments late report having routine cash flow problems. Only 2.2 percent that also receive at least half of their payments late said they never experience a cash shortfall.

The severity of this problem varies by sector. Landscaping experienced more late payments than the average. Over one-third (34.8 percent) were subjected to late payments compared to 28.7 percent total. This resulted in 62 percent of landscaping firms having cash flow problems, also a little higher than the average (55.6 percent).

When companies are forced to extend trade credit, it puts them in the uncomfortable role of playing financial institution to determine a supplier’s creditworthiness. Using a credit report from a third party was the most common method (26 percent) on average. Less common were more subjective criteria like the customer’s time in business (13.5 percent), findings of an informal web and social media search (11.8 percent) and the personal relationship with the customer (11.1 percent).

Taking on this role is beyond most firms’ area of expertise. It would seem that extending trade credit could come with unexpected risk. One solution has been trade credit insurance.

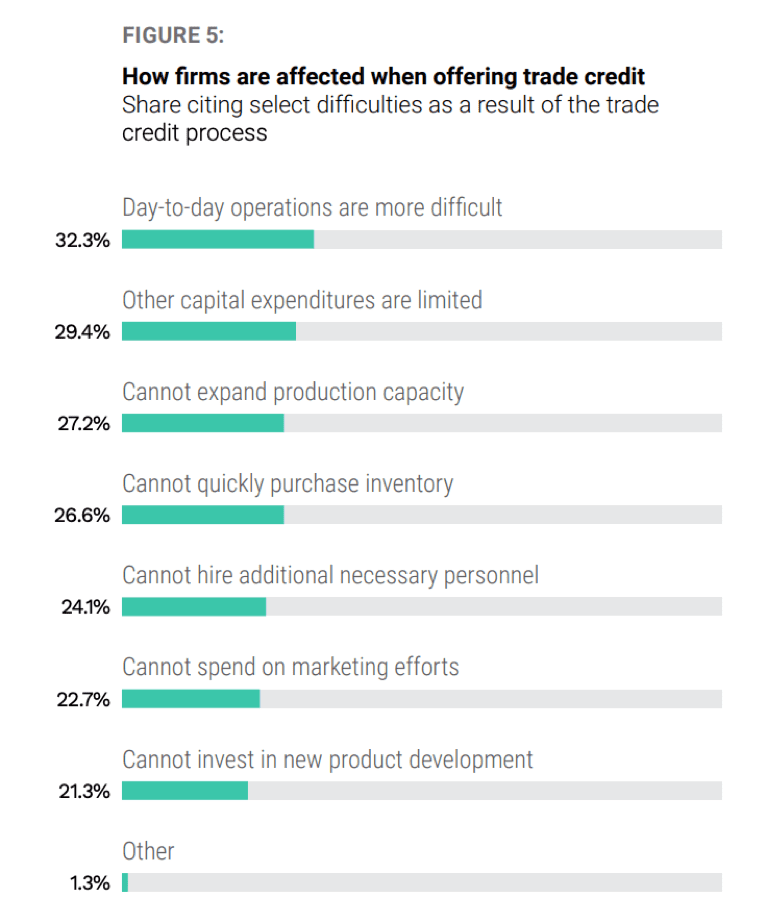

No one in the study explicitly mentioned this risk as a difficulty. One-third (32.3 percent) said offering trade credit made day-to-day operations harder, though. It also limited spending on capital expenditures, production capacity, inventory purchases, new hires and marketing efforts.

Solutions have emerged from alternative lending companies like Kabbage, BlueVine and Fundbox to give suppliers immediate payments, while buyers are given a longer time to pay or have the option of financing payments. This often comes with a fee for the seller.

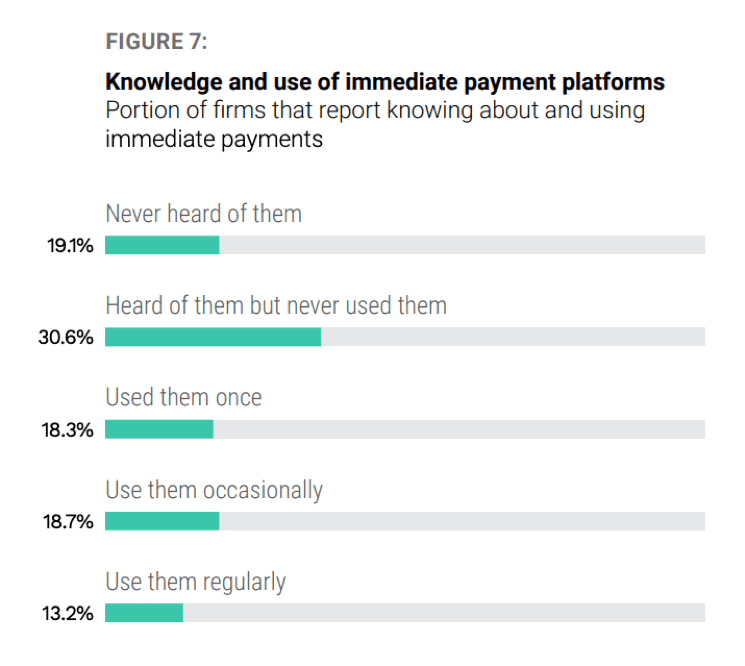

Awareness of immediate payment platforms was relatively high, but usage was low. More than 80 percent were familiar with them. Close to one-third (30.6 percent) had heard of them, but had never used them. Only 13.2 percent used them regularly.

Convenience aside, many firms perceived that immediate payments platforms could help increase revenue. A majority (58.3 percent) of all businesses believe making payments through immediate platforms would increase their revenues, while a similar figure (55.8 percent) believe the same for collecting payments.

Specifically, 36.6 percent of sellers believe immediate payments would make day-to-day operations easier, while 32.3 percent think immediate payments could help expand marketing efforts and grow their businesses. Buyers also believed immediate payments would positively affect operations and marketing, but to a lesser degree.

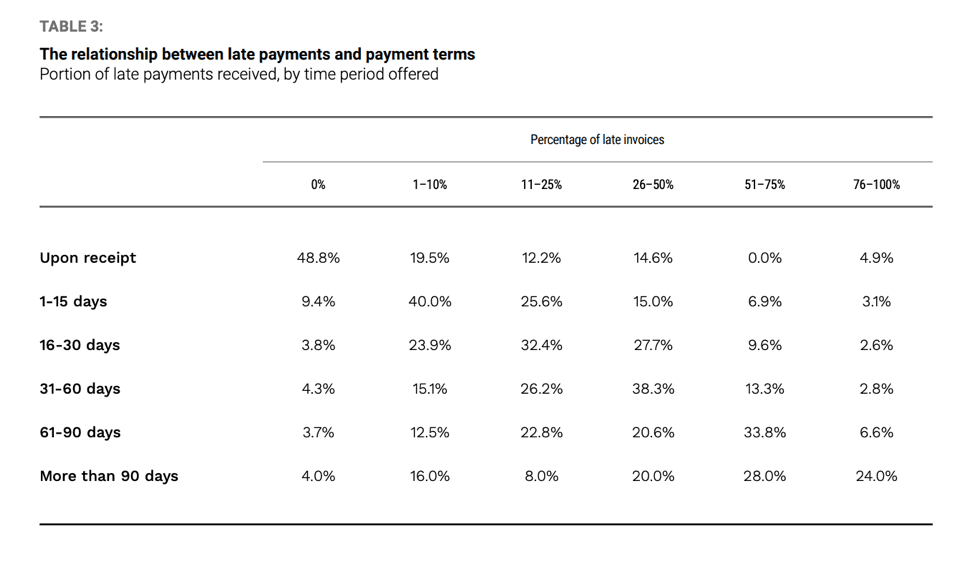

In the study, discounting and offering long payment terms were found to lead to late payments. Firms that gave between two and three months are paid late more than one-third of the time, and close to half (48.8 percent) that don’t offer extended payment terms say they are never paid late. One to 15 days appeared to be the sweet spot.

Companies that get paid late more than 75 percent of the time offer discounts of 5.7 percent on average, which is significantly higher than those offered by firms that are paid late only 10 percent of the time.

Late payments hamper routine operations in the near-term and also prevent investing in future growth. Immediate payment services have the potential to mitigate risk, and many buyers and sellers are aware they exist despite relatively low adoption.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More