In payments, complexity reigns, and making payments simple, transparent and speedy is anything but easy.

That’s especially true with cross-border payments, where commerce done globally demands that firms be aware of regulations and payments preferences that are endemic to a specific country or even specific region. Infrastructure can be varied, too, in terms of technology.

Fragmentation reigns, then, and as detailed in the Simplifying Cross-Border Payments Playbook, as firms strive to connect cross-border fund flows, any number of considerations are paramount. These include security and grappling with legacy systems in the embrace of real-time payments.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

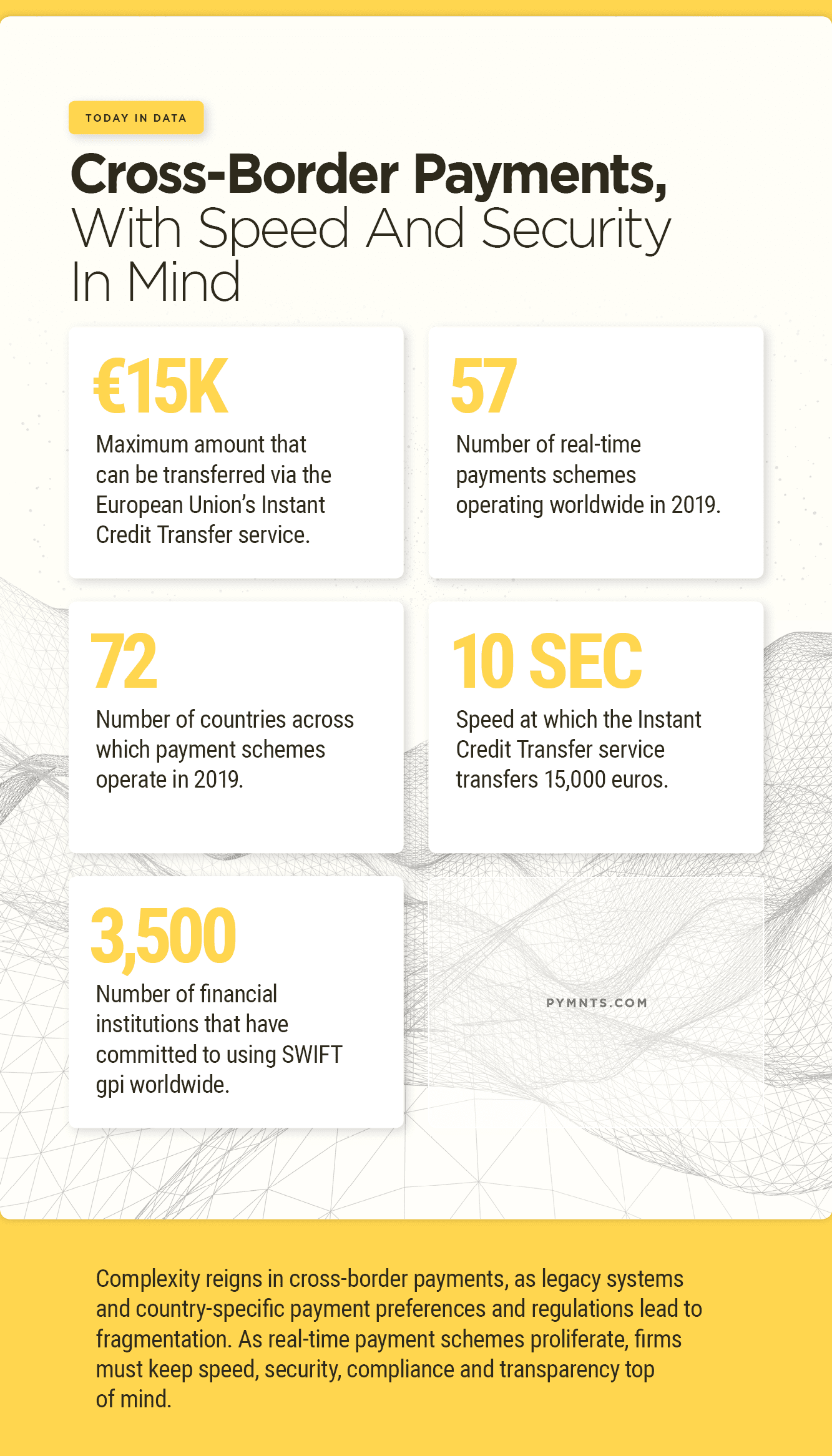

Data:

15,000 euros: Maximum amount that can be transferred via the European Union’s Instant Credit Transfer service.

57: Number of real-time payments schemes operating worldwide in 2019.

Advertisement: Scroll to Continue

72: Number of countries across which payment schemes operate in 2019.

10 seconds: Speed at which the Instant Credit Transfer service transfers 15,000 euros.

3,500: Number of financial institutions that have committed to using SWIFT gpi worldwide.