Innovation has become such a buzzword that it can be applied to countless solutions and initiatives, from emerging 5G mobile technology and the rise of “smart factories” to using blockchain to trace and track food supply chains to deploying kiosks to personalizing the ordering experience.

One thing is certain: The race goes to the swift, and there is a price to be paid when companies fall behind. But wanting to be fast and actually pulling it off are two different things.

A new Accenture study examines the cost of being slow to embrace digital technologies, and found that laggards lost 15 percent in annual revenue and could potentially lose 46 percent of revenue gains over the next few years. Additionally, leaders grow revenue at more than twice the rate of these laggards.

These findings reinforce the crux of PYMNTS’ Innovation Readiness Index, which explores how tech infrastructure is key to financial institutions’ innovation.

The State of Innovation

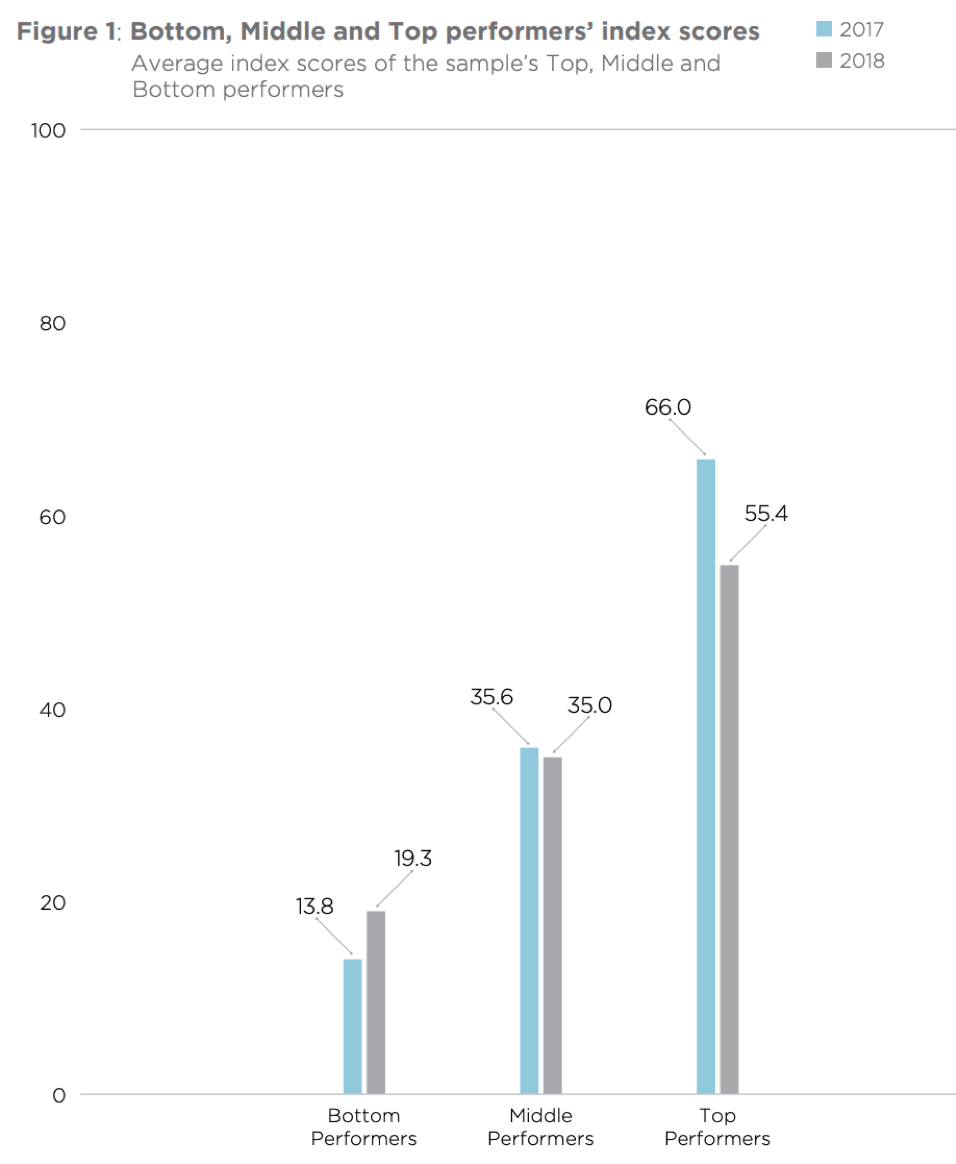

PYMNTS’ Innovation Readiness Index is scored on a scale of zero to 100. The higher the score, the more capable an FI is of designing, implementing and executing innovation plans. The highest-scoring FIs were categorized as Top Performers, while those that scored in the middle and lower ranges were classified as Middle and Bottom performers, respectively.

One of the overarching takeaways from this report was that enthusiasm for innovation appears to have cooled down between 2017 and 2018. The average Index score decreased from 37.8 to 35.3, and that decline was even more pronounced among the Top Performers, whose average fell 16.1 percent, from 66 points in 2017 to 55.4 in 2018.

Conversely, the Bottom Performers became the ones to beat. They saw their average Index score increase from 13.8 points to 19.3, meaning their ability to innovate improved by approximately 40 percent.

Innovation Drivers and Strategies

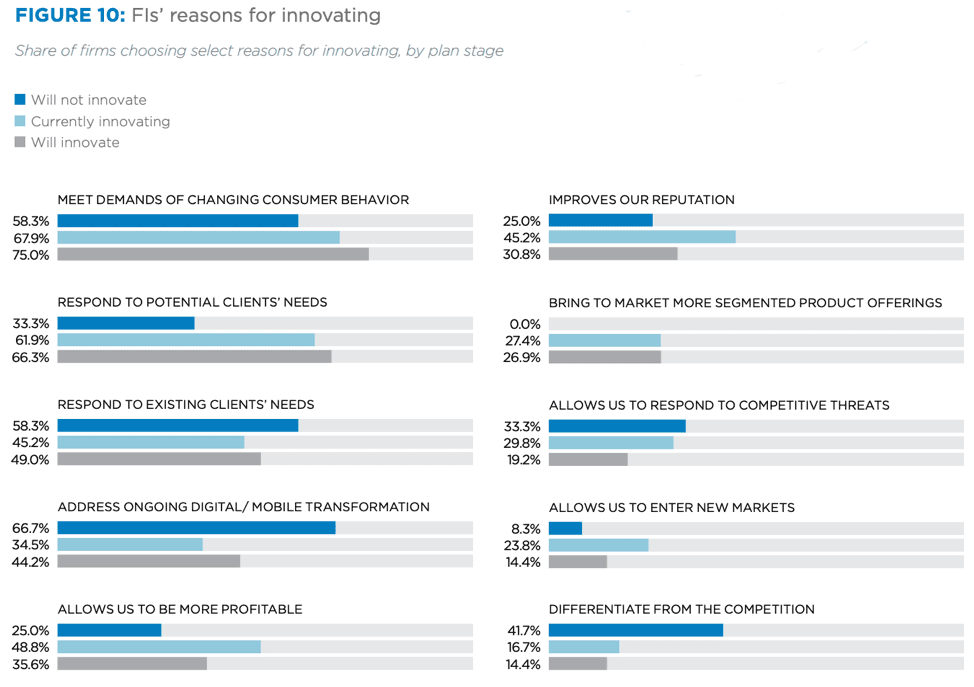

In the May Innovation Readiness Playbook, most current and future innovators say their motivation to innovate is a response to changing consumer behaviors and potential clients’ needs. Future innovators show the most interest in these needs at 67.9 percent and 61.9 percent, respectively. Financial institutions on other end of the innovation spectrum – those with no plans to innovate – seem to be focused on catching up. This group’s main goals include addressing ongoing digital and mobile changes in the market (66.7 percent), responding to changing consumer behaviors (58.3 percent) and responding to existing clients’ needs (58.3 percent).

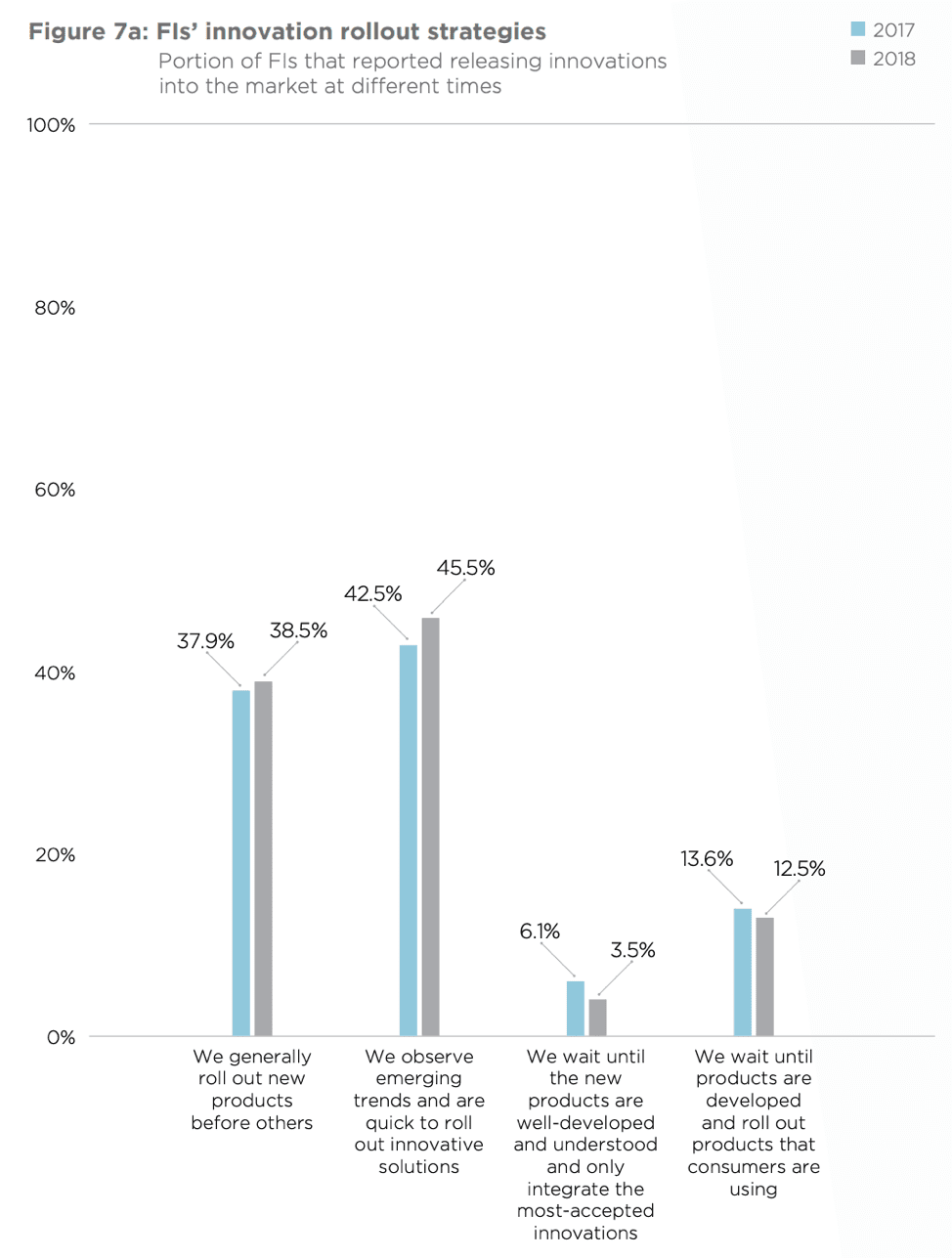

The question became whether FIs were acting fast enough to beat their competition. The truth was that most were not trendsetters, and were instead merely following the pack. However, they also liked to be as close to the head of that pack as possible.

According to PYMNTS’ Innovation Readiness Index, 61.5 percent of FIs waited to see innovations’ market reception in 2018 before investing in developing their own. Just 38.5 percent generally rolled out new products ahead of other FIs, meaning most were not unveiling new solutions in the hopes of creating new trends, but were hopping on their respective bandwagons.

It is riskier to invest time, energy and money into a project that has never been released than to do so for one that has already achieved some degree of market success.

It is also harder to design a new product from scratch than to expand on or alter one that is already in the market. Financial institutions that opted to wait for their competitors to test new products first were hedging their bets, understandably wary of fully committing without some reassurance that it would produce returns – and enabling themselves to learn from their rivals’ mistakes.

Why Innovation Acceleration Matters

According to PYMNTS’ Innovation Readiness Index, the Top Performers’ 2018 decline stemmed from taking longer to release innovations into the market, and inflexible IT infrastructures were to blame. Financial institutions of all sizes struggled to identify lucrative investment areas.

Accelerating investment in innovation was shown to be key to success in the study. Top Performers allocated a greater percentage of their IT budgets to innovation over the past five years than the bottom performers (93 percent vs. 64 percent) and plan to accelerate this investment faster than bottom performers over the next five years (97 percent vs. 74 percent).

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More