Two new reports show that the U.S. job market continued to slowly recover in September, although small businesses reported only small gains.

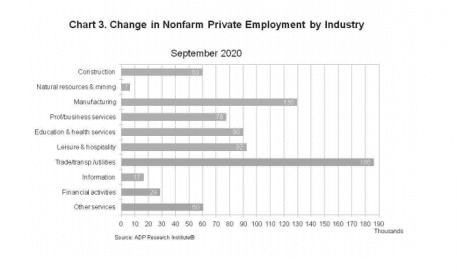

The ADP National Employment Report showed on Wednesday (Sept. 30) that private-sector companies added 749,000 new jobs in September, led by increased hiring in the trade, transportation, manufacturing and healthcare sectors.

“The labor market continues to recover gradually,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “In September, the majority of sectors and company sizes experienced gains, with trade, transportation, utilities and manufacturing leading the way. However, small businesses continued to demonstrate slower growth.”

ADP said that large companies (with more than 500 employees) accounted for roughly 40 percent of the hiring, adding 297,000 new jobs. Midsized firms (50-499 employees) filled another 259,000 positions, while small businesses (one to 49 employees) took on 192,000 new workers.

The report showed that the Trade, Transportation and Utilities group added about 25 percent of total new workers, or 186,000 additional jobs. Other pockets of strength were seen in the Manufacturing sector, which saw 130,000 new jobs added, followed by Leisure and Hospitality, which hired 92,000 and the Education and Healthcare sector, with 90,000 jobs.

On the lagging side, the Financial Activities industry only took on 29,000 new people, while the Information sector hired 17,000 people and the Natural Resources and Mining grew by only 7,000.

Advertisement: Scroll to Continue

The findings in many ways mirror those seen on Tuesday (Sept. 29) in the Paychex IHS Markit Small Business Jobs Index, which inched 0.06 percent higher to a 94.44 reading in September. That’s roughly equal to the Index’s 94.63 reading from April, when pandemic shutdowns were in full swing.

Paychex said the Northeast region’s small business hiring came in a little stronger than average, rising 0.36 percent for September.

“We’re starting to see signs of improvement in specific regions, including the Northeast, which was hit particularly hard in the early stages of the pandemic,” noted Paychex President and CEO Martin Mucci. “Activity in the construction industry has also been a bright spot. Even with hiring levels remaining flat on the national level for many small businesses, when monitoring the number of employees being paid, steady growth is being seen, indicating that small businesses are bringing existing employees back to work.”

The new reports come just days before Friday’s planned release of the U.S. Labor Department’s September Employment Situation report, the broadest measure of the country’s job market.

The new reports come just days before Friday’s planned release of the U.S. Labor Department’s September Employment Situation report, the broadest measure of the country’s job market.

August’s report showed that the U.S. economy added 1.4 million new jobs in both the public and private sectors, with the unemployment rate falling to 8.4 percent. Economists are expecting Friday’s report to show about 800,000 jobs created in September, fueling concerns that the rebound is slowing. They see job gains hurt by consumers’ financial woes, the lack of a second federal stimulus program, a seasonal uptick in coronavirus cases and uncertainty surrounding the November election.

“There are a number of risks and we are going into the fall without much insulation,” Gregory Daco, chief U.S. economist at Oxford Economics, told MarketWatch. “I continue to view the glass as half-empty. We’re still a long way from where we were pre-COVID.”

Although job market growth and the unemployment rate have both rebounded from their springtime lows, the nation’s labor force is still down by about 11.5 million workers from pre-pandemic levels. A final reading on second-quarter gross domestic product confirmed on Wednesday (Sept. 30) that the U.S. economy shrunk by 31.4 percent for the three months ending June 30. However, that was a slight improvement from the initial report of -31.7 percent.

To be sure, the country’s economic measures continue to offer mixed results. Earlier this week, the S&P Case-Shiller Home Price Index showed that property values rose 3.9 percent in July. But the Mortgage Bankers Association’s weekly applications index posted its biggest drop in a month on Wednesday, falling 4.8 percent.

At the same time, the Conference Board’s Consumer Confidence Index surged to 101.8 in September from 86.3 last month, reaching its best level since the pandemic struck and posting its biggest one-month increase in 17 years.