It’s just a week into the earlier-than-usual 2020 holiday selling season and already three facts are clarifying the retail picture: consumers are going to spend less overall, they are going to spend more time online and they don’t want to touch anything in the process.

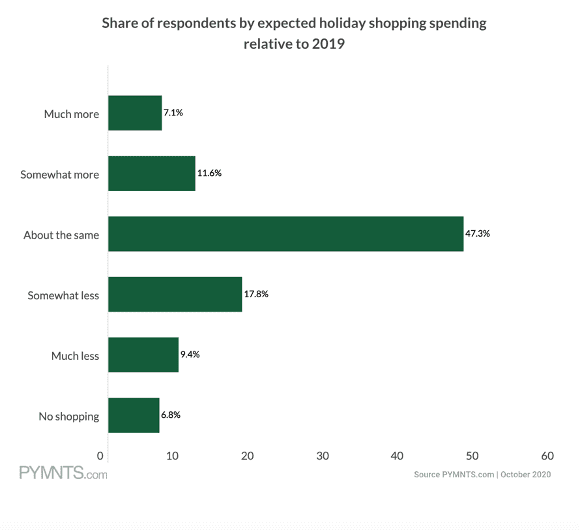

PYMNTS data shows that all three dynamics will become solid planning factors as the season heads into November. Perhaps the data points that are the most contentious center around overall spend. Some forecasts put total retail spending slightly ahead of last year. However, PYMNTS data, which directly addressed intent to spend, shows that only 18.7 percent of consumers will spend more than they did in 2019. Consumers who said they would spend “about the same” accounted for 47.3 percent of responses. The survey showed that 17.8 percent would spend somewhat less, and 9.4 percent would spend much less this year. In a surprising twist, 6.8 percent said they wouldn’t be shopping during the holiday season at all.

The low percentage of enthusiasm for the season (only 7.1 percent said they would spend “much more”) begs the issue of a possible stimulus. It’s hard to know if a December-timed check would be spent on holiday shopping, but it’s clear that the previous stimulus was used for two things: savings and paying down debt. According to PYMNTS’ analysis of University of Chicago data, about 42 percent of consumers saved all or part of their stimulus payment. Forty percent used the payment for debt such as mortgages, auto loans or student loans. Only about 15 percent said they spent the entire stimulus check. This relatively low rate of spending for a one-time transfer is higher for consumers who are facing liquidity constraints, are unemployed, live in larger households or are less educated.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

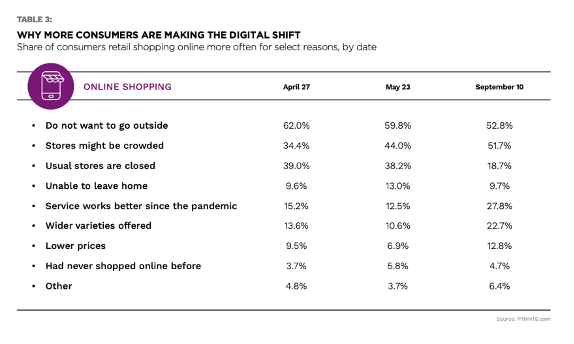

Stimulus aside, when consumers shop this holiday season a greater percentage will do so online. PYMNTS has been tracking consumer spending attitudes and behaviors in the pandemic and found that when it started in early March, only 12.3 percent of all shoppers planned to shift their retail shopping from in-store to online. That number gradually rose up to 48.3 percent in August and has now settled to 41.9 percent. Diving deeper into that number, 83.9 percent of those consumers plan to maintain some or all of their newfound retail shopping habits. The primary reason for avoiding physical stores is still fear of contracting COVID-19. It is clearly stated among consumers using online grocery or food aggregators, and takes on more nuance for retail shopping with 52.8 percent of respondents saying they “do not want to go outside” and 51.7 percent wary of crowds in stores.

The reasoning is more direct when consumers were asked their reasons for wanting to shop with merchants that provide digital purchasing options. The most common reason consumers say they want to shop with merchants offering digital options is the fear of contracting COVID-19. This reasoning is most prevalent among baby boomers. Forty-seven percent of baby boomers and seniors who choose merchants for their digital offerings say it is because they might otherwise contract COVID-19, and 41.5 percent of Generation X consumers and 33.6 percent of millennial consumers say the same.

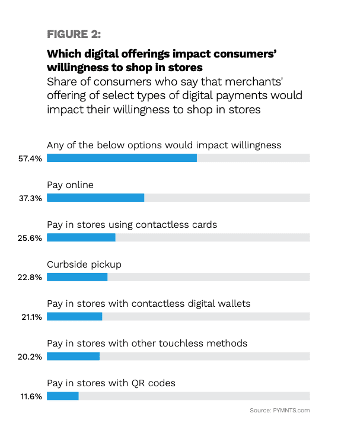

When they do shop they want the digital offerings mentioned here, and the research shows payments play a big role. When asked which digital offerings will impact their willingness to shop in stores consumers said they are particularly interested in using contactless payment options, as 26 percent and 23 percent of consumers say merchants must accept contactless cards and offer curbside pickup, respectively, for them to feel comfortable shopping in a store. This underscores a widespread desire to avoid more traditional in-store payment options, such as cash or cards, which require consumers to make physical contact with paper bills and POS terminals.

Advertisement: Scroll to Continue

Having digital payment options is even more important to bridge millennials, millennials and members of Generation Z than to the average consumer — and far more important than it is to either Generation X consumers or baby boomers and seniors. The payment options merchants accept impact consumers’ willingness to shop in store for 69 percent of bridge millennials, 70 percent of millennials and 71 percent of Gen Z consumers. Just 55 percent of Gen X consumers and 46 percent of baby boomers and seniors say the same. This shows that although digital payment options are in high demand among consumers of all ages and backgrounds, they are in highest demand among millennials and bridge millennials, who are not only the most accustomed and comfortable with the eCommerce shopping experience but who are also professionally established enough to have disposable income to spend on eCommerce purchases.