A transformation toward contactless payments is underway at the nation’s credit unions as the public shuns cash and even physical cards to lower infection risks with COVID-19. This change in consumer behavior is expected to remain even after vaccines are more widely distributed. It will likely alter global markets and regulations as the financial ecosystem becomes more digitized.

Tom Gandre, chief operating officer at credit union service organization PSCU, told PYMNTS’ Karen Webster that his data shows clear signs of this trend: The number of contactless payments made by American CU members has more than doubled since the beginning of 2020.

The use of Apple Pay, Google Pay and other digital wallets has also been on the upswing since the start of the pandemic. PSCU reported that the hike in mobile wallet credit purchases among its CUs’ members was nearly 36 percent by January 2021, while mobile wallet debit purchases climbed to nearly 60 percent during the same period. The following Deep Dive examines the interest in contactless payments among credit union members and the opportunity for the CU space to meet members’ changing payment needs through digital innovation.

The High Stakes Of Offering Contactless

New research is showing that contactless payment options have become so important to consumers that they may abandon purchases if these preferred methods are not available to them at checkout. Fifty-seven percent of survey respondents in PYMNTS’ How We Shop Report stated that merchants’ digital payment options impact their willingness to shop, and 26 percent insisted that merchants accept contactless card payments. Offering touchless payments thus has the potential to drive merchants’ performance through consumer preference.

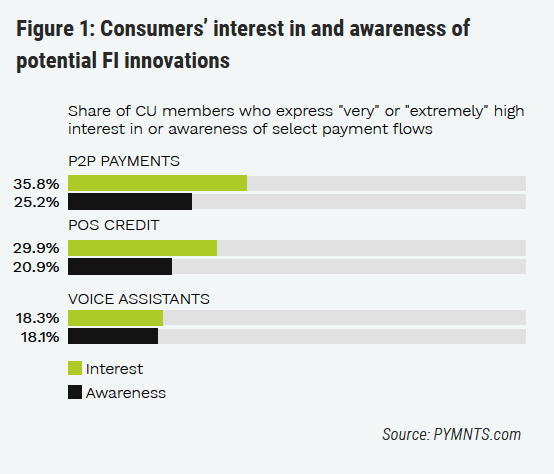

CU members in particular have a growing appetite for digital payment options. PYMNTS’ 2020 Credit Union Innovation Index, conducted in partnership with PSCU, found that many CU members are interested in adopting new payment methods, even with little knowledge of them. Consumers who value financial institution (FI) innovation expressed a desire for a variety of technologies, including peer-to-peer (P2P) payment apps, point-of-sale (POS) credit financing options such as buy now, pay later plans and voice assistant tools. Nearly 36 percent of CU members said they are “very” or “extremely” interested in using P2P payments, for example, yet only 25 percent said they are familiar with them. Thirty percent of CU members similarly expressed an interest in POS credit options, despite only 21 percent reporting awareness of them.

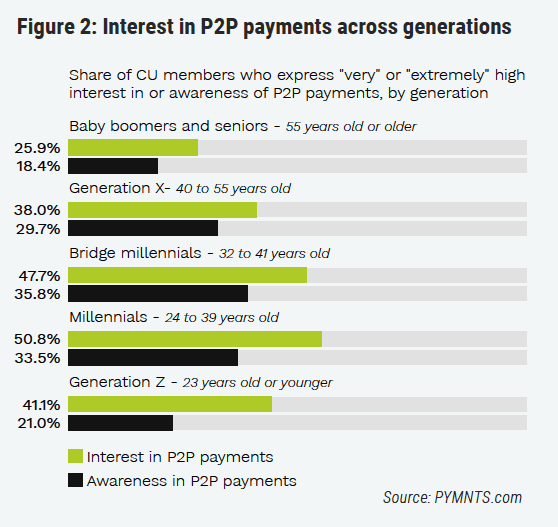

CU member interest in digital payment methods is also strongest among younger age groups representing sought-after markets for CUs because of concerns about aging membership bases. PYMNTS’ research indicates that millennials (ages 23 to 39) and bridge millennials (ages 30 to 40) have the greatest interest in P2P payment use, for example. Nearly 34 percent of millennial CU members and almost 36 percent of bridge millennial members are already familiar with P2P payments, yet their interest in using them is even higher: 51 percent for millennials and 48 percent for bridge millennials.

These findings indicate major — and potentially missed — opportunities for CUs in the digital era of financial services. PSCU’s Gandre suggests that CUs must think more like challenger banks when it comes to staying on top of digital payment innovation if they want to remain competitive in the evolving space. The pandemic has driven home the need for mobile and online banking strategies to provide seamless member experiences as consumers stay away from branches out of desire or necessity. All indicators suggest that these trends are only likely to continue to grow, however. CUs that can push the digital envelope by meeting member demands for more variety in payment technologies are sure to see advantages in 2021 — and beyond.