Like many young parents across America, I spend a lot of time at Walgreens. If fact, as I am not such a “younger” parent anymore, I find myself spending more time then I would like there.

I have found Walgreens to be a reasonably good digital partner of mine. They are pushing their bar code based app and loyalty aggressively – and it is a good app! Kiosk-based checkout is getting better and ExpressPay has been a wonderfully delightful customer experience. I can scan from the app or reorder in app for all prescription refills. My lock screen is ready willing and able with the Walgreens app when I get within a reasonable distance of a Walgreens location.

Last week however, I found myself a confused customer. I was wondering as a longtime customer of Walgreens and full throttle investor in payments and emerging commerce for a decade and a half, why the hell they had decided to accept Apple Pay.

Any frequent readers of these pages know through multiple interviews I have conducted with Karen Webster, I have announced my skepticism of Apple Pay as anything but an important early inning event, but not transformational in anyway. I am still skeptical of Apple Pay. But this piece is not about skepticism, but rather utter bewilderment of Walgreens decision.

Any frequent readers of these pages know through multiple interviews I have conducted with Karen Webster, I have announced my skepticism of Apple Pay as anything but an important early inning event, but not transformational in anyway. I am still skeptical of Apple Pay. But this piece is not about skepticism, but rather utter bewilderment of Walgreens decision.

Let me explain.

For the last couple years I walk into Walgreens and my resident app is ready to rock. I pick up what day to day items I need, grab my script(s) and start a checkout process that is more cumbersome than it needs to be, but efficient nonetheless. I am prompted for the last four digits of the phone number linked to my rewards account – still not sure why this is necessary!-, they scan the bar code in my app – the same app I reordered from – and then check me out via ExpressPay as I have opted into this highly functional checkout benefit. Then they hand me 6-8 paper receipts/coupons – my biggest pet peeve check my Twitter feed here to see earlier comment on this issue.

Advertisement: Scroll to Continue

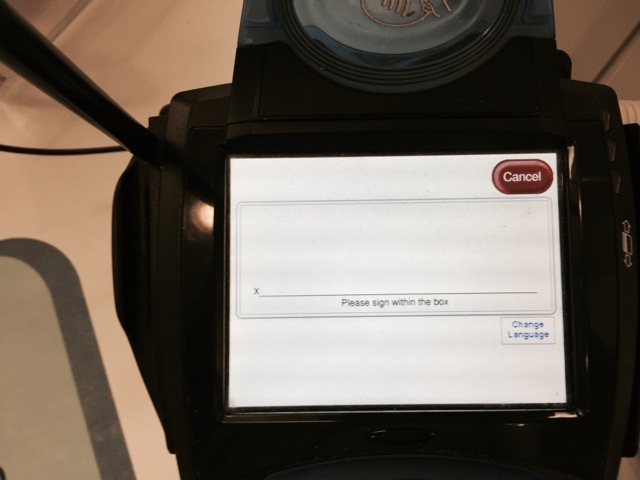

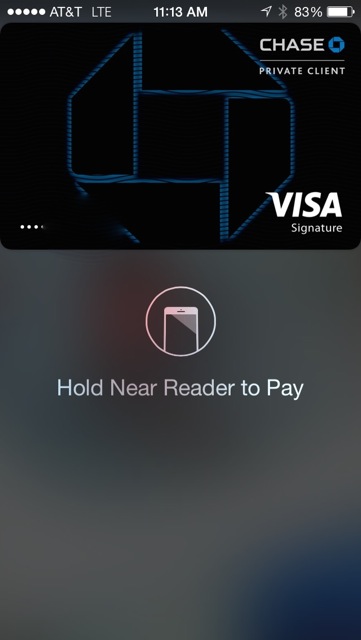

Last week I got the opportunity to use Apple Pay. Knowing that my rewards were not linked I went through the same routine as above. But when we got to payment I stopped. I wanted to tap and go! So I tapped….and I didn’t go. I scanned my thumbprint, and then was prompted to get my handset closer to the terminal to scan again. Once again proving the utterly farcical “tap and go” marketing fraud that is NFC. Then the kicker – my signature! I couldn’t make this stuff up.

I asked the clerk why in the world I needed to sign. I was told because the transaction was more than $50.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Wowser.

I thought they were going to need to get the AED paddles off the wall to revive me from cardiac shock.

I will give Apple Pay and Tim Cook points for security. I guess my transaction would at that point qualify for like quintuple or sextuple factor authentication?

I kind of wished they videoed me so it could be a YouTube parody of Tim Cooks “physical retail checkout is broken” video he played back in September.

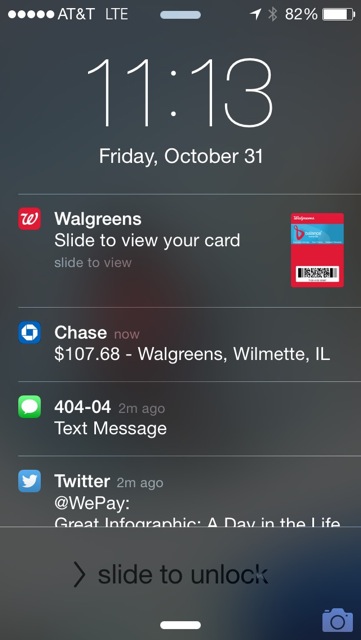

With my transaction complete – the paper stills flows to me – I actually now just refuse it. This is what my lock screen locked like.

Confusing right?

Where is Apple Pay?

Why would Walgreens relinquish any real estate to anyone?

I am their customer. Don’t they want to own me? Why would they let foxes like Apple, issuers or networks into their henhouse? Have they not learned that lesson already?

One would think in their battle to get the Durbin Amendment added to Dodd Frank they would have come to their senses. But this doesn’t look like it to me.

So I ask again, with all the cost, Walgreens why the hell did you do this?