Aggregators closed the gap last year as they competed with restaurants for diners’ digital spending.

By the Numbers

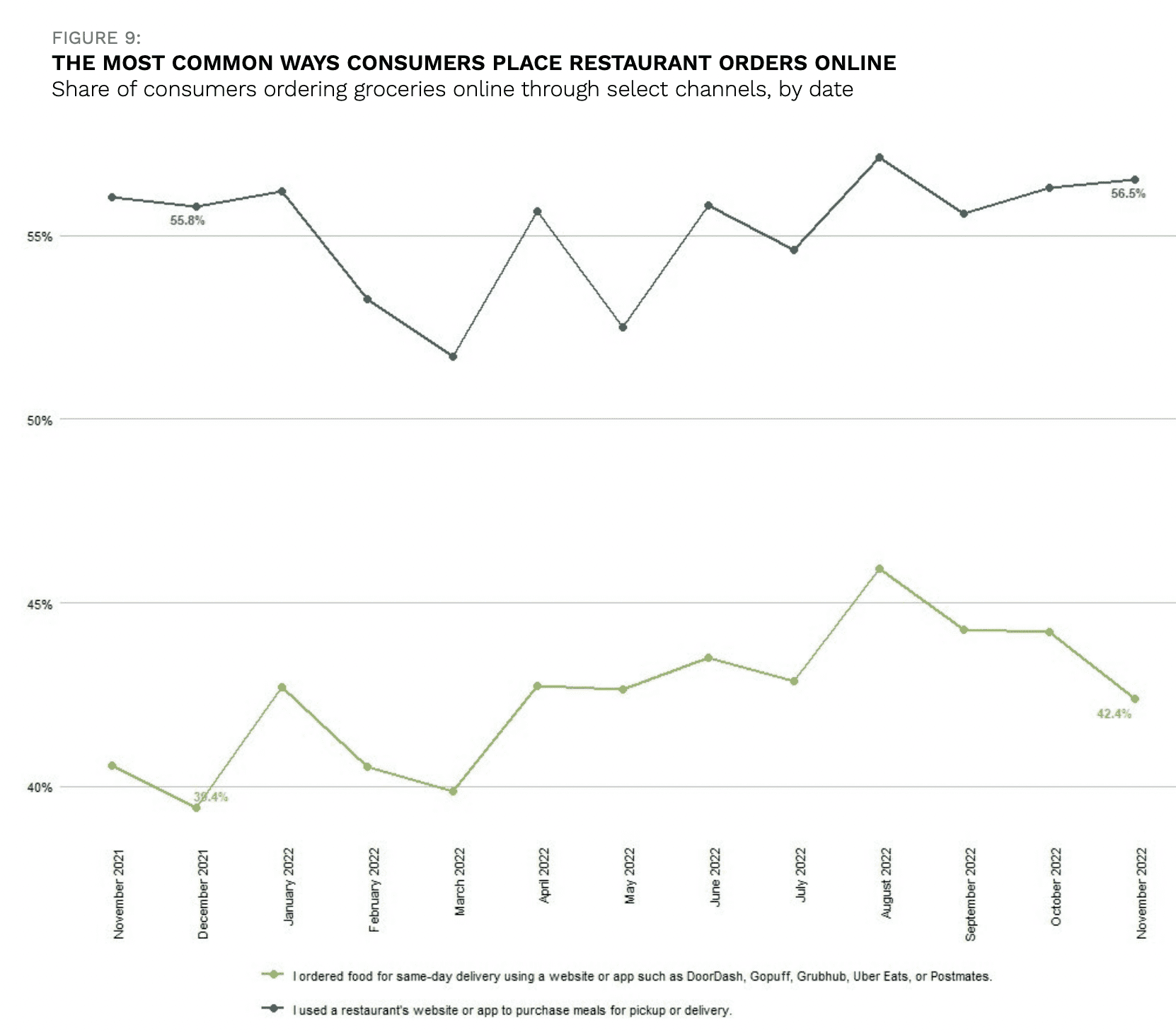

Specifically, aggregator adoption saw a modest rise year over year, and although online ordering directly from restaurants remained well ahead, it also stayed relatively the same throughout 2022. That’s according to research from PYMNTS’ study “12 Months of the ConnectedEconomy™: 33,000 Consumers on Digital’s Role in Their Everyday Lives.”

The report, which drew from responses from tens of thousands of U.S. consumers over the year, noted that between the end of 2021 and November 2022, direct ordering remained roughly at 56%. Yet in the same period, aggregator ordering rose three percentage points. This modest increase, however, still had third-party channels lagging well behind, amounting to 42% of diners as of November 2022.

The Data in Context

Certainly, aggregators have been doing everything in their power to drive adoption, expanding their offerings and courting consumers with targeted promotions.

Advertisement: Scroll to Continue

Grubhub, for one, has been especially active in its efforts to bring new customers into its ecosystem. Over the course of the year, the aggregator announced two partnerships with companies with large followings, promising a year of its delivery subscription Grubhub+ both to Amazon Prime subscribers and to Bank of America cardholders.

“This is truly a win-win, with Bank of America now rewarding cardholders with deals and perks from restaurants they will love, and Grubhub tapping into Bank of America’s loyal and vast customer base to drive even more orders to restaurant owners and drivers,” Grubhub Vice President of Loyalty Launika Raykar said in an August press release.

DoorDash, meanwhile, looked to the holiday season to drive purchases of its own delivery subscription, DashPass. In November, the company announced the option for consumers to purchase three-, six- or 12-month memberships for others as a gift to be sent via email, an option not offered by any of its major competitors.