Dubai is planning to expand its blockchain-powered know your customer (KYC) tool for financial institutions (FIs), according to an announcement.

The nation’s Department of Economic Development has joined the Dubai International Financial Center (DIFC), a financial hub for 72 countries in the Middle East, Africa and South Asia, to expand the feature which accounts for more than half of all KYC verifications in Dubai.

The DIFC said its goal is to support evolving technologies such as blockchain to position Dubai as the global go-to financial hub. The city is not alone in its efforts to use blockchain technology for digital identity verification.

A report found that 40 percent of respondents from technology companies around the globe have a blockchain development in the works, while 90 percent of executives said blockchain will increase in importance in the coming years. The technology is expected to expand the global gross domestic product (GDP) by nearly $1.8 trillion in the next decade.

Blockchain, which was developed in the 1990s, is a decentralized public network that allows consumers and businesses to store and safely transfer currency and financial data instantly. It is not held on a master computer or controlled by a single entity, instead being distributed over many computers, adding to its safety from cyberthieves. Blockchain is valuable because it promises to eliminate go-betweens, cut costs, increase speed and provide transparency and traceability.

The following Deep Dive examines the use of blockchain technology for digital ID verification and how it eases customer onboarding as well as how it can be leveraged to unlock innovative experiences for consumers.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Why Blockchain Adoption Is on the Rise

One 2020 survey found a year-over-year increase in blockchain adoption to 16 percent from 5 percent among all industries and countries, while planned adoption similarly rose to 18 percent from 5 percent. The banking space is the biggest planned and current adopter of blockchain technology among financial markets at 53 percent, followed by the insurance industry at 33 percent. Asian banks in particular have consistently demonstrated an appetite for such technologies to speed and improve customer service. A consortium of financial players in Singapore became the first in Southeast Asia to develop a blockchain-based KYC solution prototype.

The KYC check is a crucial process FIs conduct to ensure the authenticity of those with whom they are trading. The FI analyzes documents, such as ID proofs, utility bills and credit card information, to certify the customer’s identity, a process that is repeated for each interaction. The beauty of blockchain technology is that the customer needs to undergo the KYC process only once, and then the validation is stored on the blockchain for later use. The customer is in control of what happens with the data, promoting greater consumer trust in blockchain compared to other verification measures that risk exposure to bad actors.

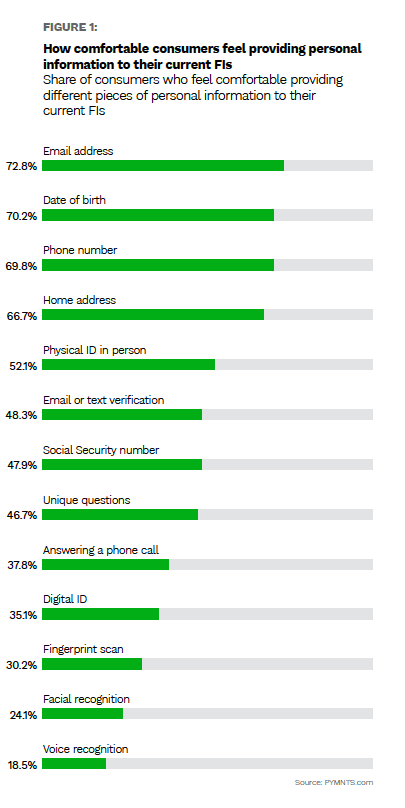

PYMNTS research from 2020 noted that FIs must develop novel ways to authenticate their customers and devise methods to quickly and easily onboard them or risk poor customer satisfaction. The survey of 2,063 U.S. consumers examined how they accessed their banking accounts, how they opened new accounts and their comfort levels when providing sensitive personal information to FIs. It found that 57 percent of consumers who had already interacted digitally with their FIs have increased their use of digital channels, 70 percent did not mind providing standard personal information to their FIs, and 64 percent reported they would be more comfortable providing personal information if they knew it would not be shared with third parties.

These findings indicate consumers’ increased engagement with digital channels and recognition of the need to provide a certain amount of personal data for this purpose, but they also highlight the importance to consumers of knowing that their data is secure and will not be shared without their knowledge.

Protecting customers’ private data and educating them about the tools and technologies designed to secure their information can help reduce their apprehension about engaging in onboarding procedures. PYMNTS data also showed that consumers have varying comfort levels with the information they are asked to provide, being most comfortable sharing email addresses, dates of birth and phone numbers and least comfortable sharing biometric indicators, such as voiceprints, facial scans and fingerprint scans.

It is no wonder the banking space is so eager to invest in and embrace blockchain technology: Its greater transparency, speed and security promise FIs the opportunity not just to build customer relationships, but also to be on the cutting edge.