Online security, always a priority, has taken on greater urgency as consumers use digital channels to shop and carry out their banking activities in higher volumes. Research revealed that consumers are expressing growing comfort with and a preference for physical and behavior-based methods of security that are both convenient and invisible. Passwords did not rank among the top three most secure ways to verify a customer’s identity for the first time since 2017. Instead, these spots are going to physical biometrics, PIN codes texted to mobile devices and behavioral analytics that do not require any consumer effort.

Alongside the flood of digital activity comes an increased need to protect users from fraud. Online transactions have risen 20 percent since the start of the pandemic, and 55 percent of consumers identify security as the most important part of the online experience. This Deep Dive examines how newer tools and technologies, including biometrics, behavioral analytics and IP verification processes can help seamlessly identify users and curb fraud.

How ID verification frictions lead to account-opening abandonment

Consumers have embraced the transition to using primarily digital channels for their daily interactions. Eighty-two percent of United Kingdom (U.K.) consumers in a recent study said they are willing to open accounts digitally.

But more than half of U.K. banks have difficulty verifying identities across channels. Seventy-two percent of banks in the country have implemented digital ID verification methods for personal accounts, but just 36 percent said they can capture and verify users’ identities within the same channel.

This inability to integrate ID capture with validation has made clients much more likely to abandon online applications. Thirty-two percent of consumers in the study said they would ditch a new account opening if asked to complete sign-up in a different channel. The frictions caused by these complicated authentication procedures can result in substantial losses of customers and revenues.

Sixty-two percent of firms polled in a recent survey said their companies had increased their deployment of remote onboarding and authentication technologies to counteract customer abandonment. It also meets their need for seamless verification and has fueled the use of biometrics. Forty-five percent said they have witnessed an increase in biometrics adoption because of the pandemic, highlighting the reality of these new vulnerabilities.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Behavioral analytics and IP address verification

Knowledge of online user behavior and the mindset of cybercriminals has given rise to another essential strategy for identifying fraud. Behavioral analytics targets fraud by comparing legitimate users’ interactions, including mouse movements, keystrokes and swipes, to the known behaviors of cybercriminals. An analysis found that 64 percent of account-opening fraud cases showcased behaviors that demonstrate a lack of familiarity with data. Behavioral analytics is rapidly becoming a powerful new tool for identifying risk in the account-opening process.

Geolocation service firms provide specifics about where a consumer is located based on the IP address from the HTTP header on the order placed at a merchant’s site. This can then be compared to the consumer’s stated location, helping a company determine whether the order was made by a fraudster. The whereabouts of an IP address can be examined against the billing or shipping address, ZIP code and area code. Geodata cannot be limited to IP addresses, as fraudsters can fool IP data, and banks that rely on IP-specific location data for users and companies may hurt rather than help the situation.

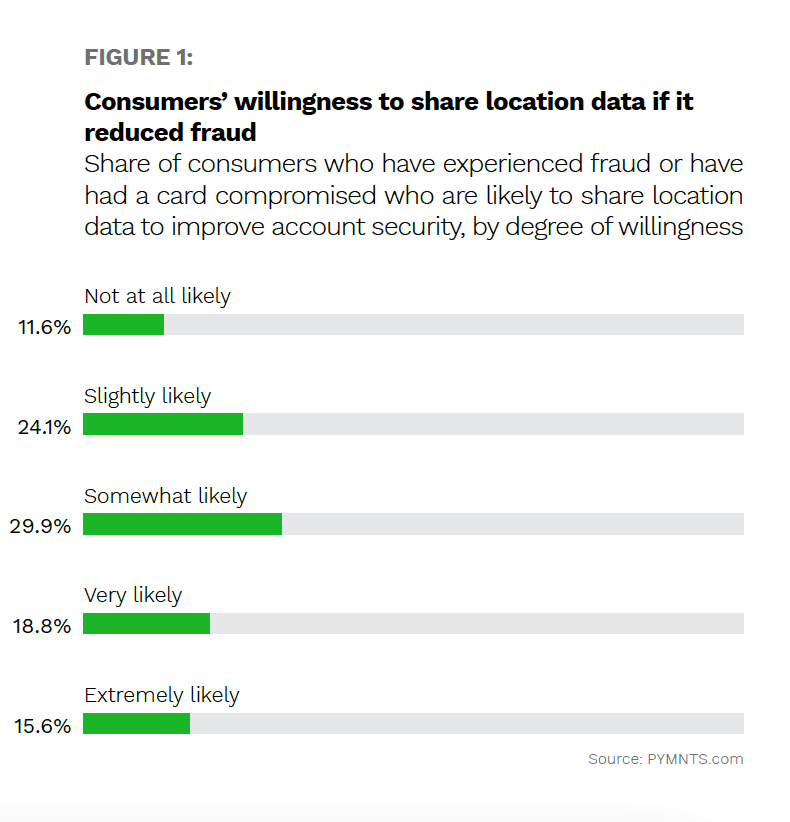

Trevor Wingert, a senior know your customer (KYC) and anti-fraud solutions consultant for GeoGuard, told PYMNTS in a recent interview that moving beyond IP addresses for determining location is critical, especially when it involves the verification of data. He noted that consumers are starting to make informed decisions about sharing their location data, presenting an area of opportunity for the year to come. A GeoGuard survey found that U.S. consumers were increasingly likely to share their locations with banks to protect themselves from fraud.

Wingert noted that there is a direct correlation between stopping location fraud and putting a halt to all fraud, adding that GeoGuard is finding increased awareness of the value of location signals. Leveraging geodata from apps is a better way to guard against illicit activity, as this information allows banks to pinpoint the locations of devices at transaction times.

Harnessing advanced technology tools such as these can help banks and merchants provide customers with seamless end-to-end user experiences that also deliver the invisible security they crave.