The digital shift quickly morphed into the connected economy, and in that online global ecosystem, identity is at least half the battle when it comes to securing against cybertheft.

In The Next Wave: The Business Adoption Of Digital Fraud Solutions Playbook, a PYMNTS and Equifax collaboration, researchers examined the priorities and concerns of businesses today around digital identity innovation, taking the pulse of more than surveyed 300 decision-makers at a variety of business from auto dealers, banks and credit unions to P2P alt-credit lenders.

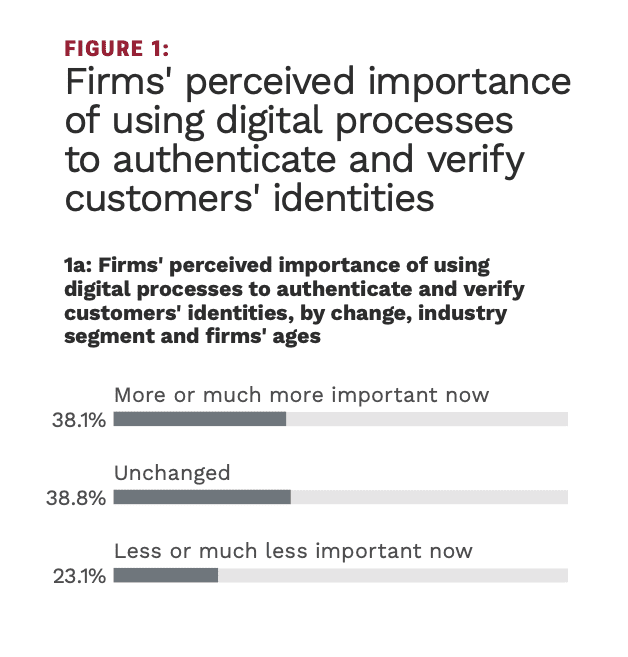

Company size and age are a factor in how businesses rate the urgency of digital identity solutions in 2021. Per the research, “Larger firms represent the highest percentage of respondents [reporting] that digital processes for authentication and verification are important,” with 49 percent of companies doing over $500 million in annual revenue calling digital identity authentication “more” or “much more” important now than it was in 2020.

Smaller firms (under $50 million in annual revenue) “represent 60 percent of businesses that believe that using digital processes is ‘less’ or ‘much less’ important.”

See: The Next Wave: The Business Adoption Of Digital Fraud Solutions Playbook

Uses of Authentication Multiplying

Contributing to the new immediacy is a panoply of issues, some unique to specific verticals and other shared by most if not all businesses as they shore up their digital positioning.

Illustrating this, the report notes, “P2P lenders that plan to invest in digital authentication solutions more commonly cite consumers’ lack of adequate access to technology as a key authentication challenge prompting them to invest in innovative solutions (62 percent). Auto dealers that plan to invest cite delays with existing digital processes as a key factor (55 percent) and banks and credit unions cite consumers’ lack of skill in navigating their current processes as a reason for making new investments (58 percent).”

A common theme among respondents in all sectors is onboarding new clients for growth.

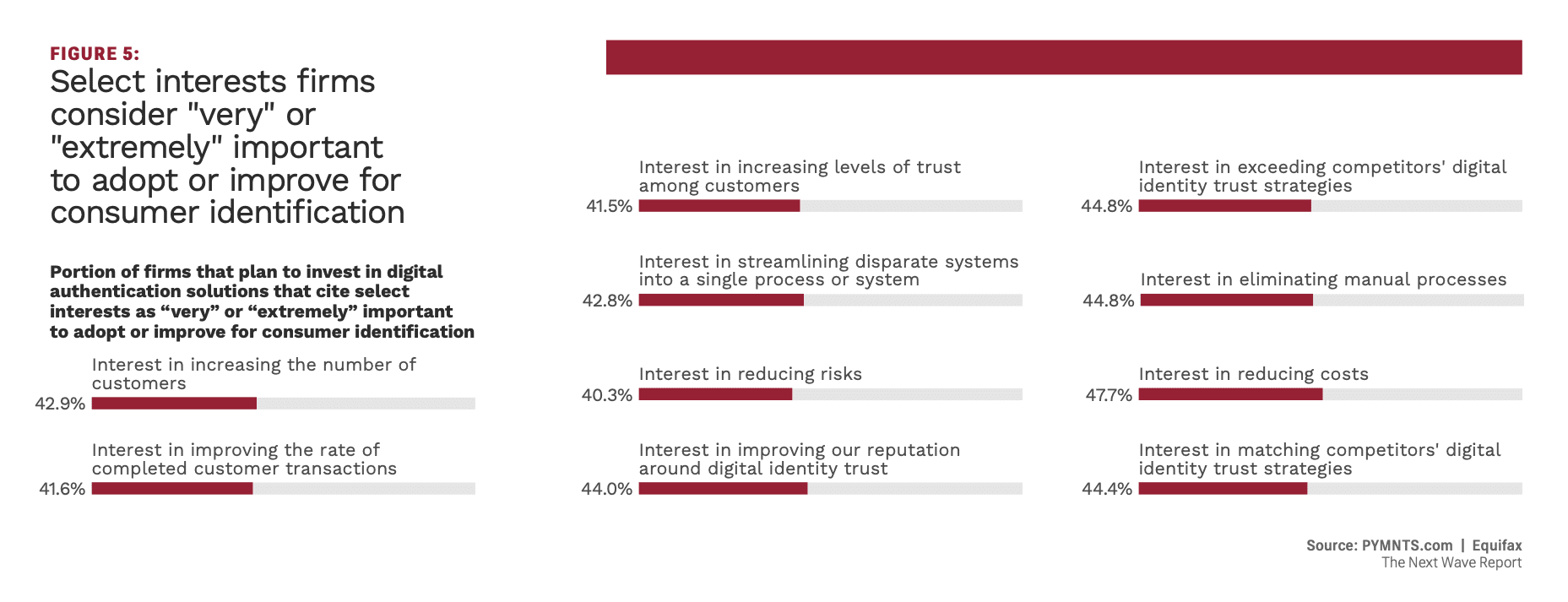

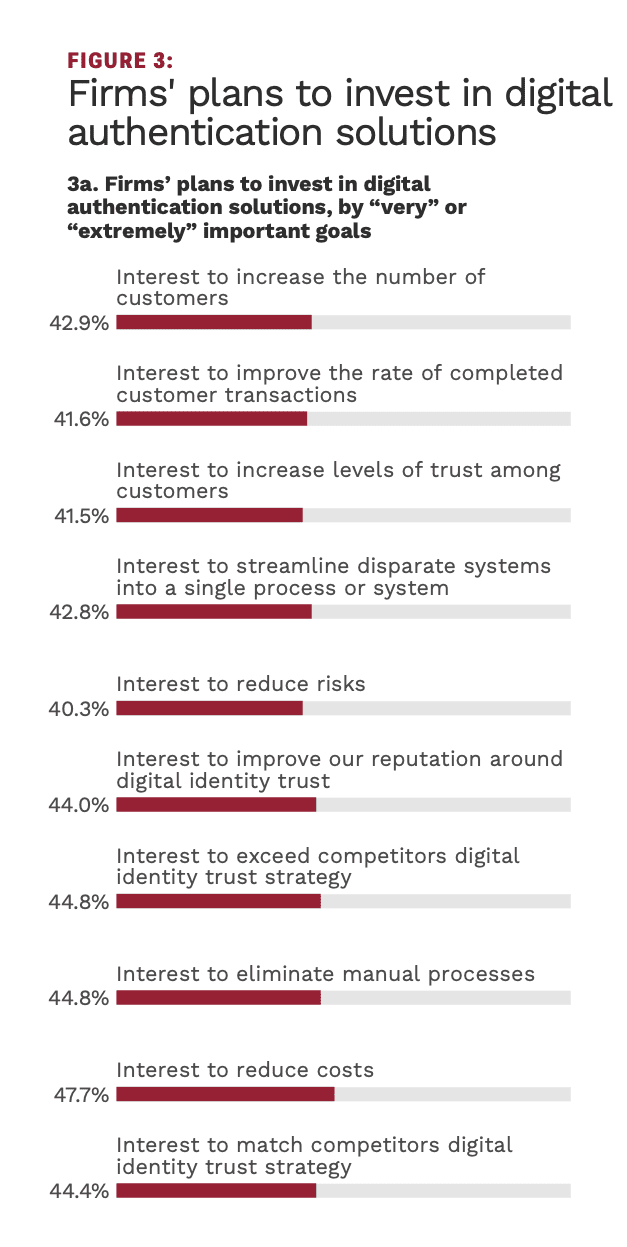

“More than two-thirds of firms consider increasing their customer bases to be a ‘very’ or ‘extremely’ important reason for adopting or improving digital processes for consumer identification. This is closely followed by firms’ interest in improving their rate of complete transactions (68 percent) and boosting trust among customers (67 percent).”

See: The Next Wave: The Business Adoption Of Digital Fraud Solutions Playbook

Cost Reduction, Customer Acquisition Driving Adoption

Other reasons for doubling down on digital identity also surfaced in the new research, with a desire to streamline and be more cost-efficient making the cut as major motivators.

“Forty-eight percent of firms that plan to invest in digital solutions that help with authentication are interested in reducing costs to adopt or improve digital processes for consumer identification,” according to The Next Wave: The Business Adoption Of Digital Fraud Solutions Playbook.

Clearly, it’s trending. How fast businesses move may decide winners and losers later on.

“PYMNTS’ research shows that more than 40 percent of surveyed firms plan to invest in digital authentication solutions to protect themselves and their customers from growing security threats,” per the study. “These firms also see investments in such solutions as key to boosting their customer bases. Investing in innovative authentication and verification solutions is going to be vital to improving relationships with customers and gaining their trust in the long term.”

Read: The Next Wave: The Business Adoption Of Digital Fraud Solutions Playbook