Buy now, pay later (BNPL) services have quickly gained a large foothold in the retail scene, becoming a household name in digital payments within a short period of time. A recent study found that 25% of eCommerce shoppers in the United Kingdom now use BNPL, for example, with 20,000 different merchants offering it at the point of sale. These services have traditionally been the domain of younger, lower-income demographics such as millennials and Generation Z, who use BNPL to fund purchases they otherwise could not afford.

BNPL options are expanding out of this traditional customer base, however. Wealthier and older generations are deploying BNPL to finance one-time, big-ticket purchases that they could likely afford to buy outright or with traditional financing options, instead leveraging BNPL for cash management purposes. Merchants that sell these big-ticket items are becoming aware of this new customer base and are rolling out BNPL options to take advantage of the larger ticket sizes and improved conversion opportunities they afford. An availability gap remains, however, with demand outpacing supply for BNPL services among these customers.

This month, PYMNTS Intelligence examines BNPL for larger-ticket items and how this use case differs from that of low-priced purchases, both in the type of consumer involved and in how they use BNPL for these large purchases.

BNPL For More Established Consumers and Big-Ticket Products

More established consumers, who tend to be older and with more purchasing power, are typically approaching BNPL from a different mindset. They have the financial means to make smaller purchases and instead are looking to tap into free or low-cost financing to better manage finances or as a way to keep more cash on hand. This segment is more likely to use BNPL to pay for larger purchases — whether necessities such as new appliances or more discretionary purchases. Older shoppers also can be a bit more averse to new ways of paying but will start gravitating toward BNPL more and more as their comfort level with the process and the provider offering it grows.

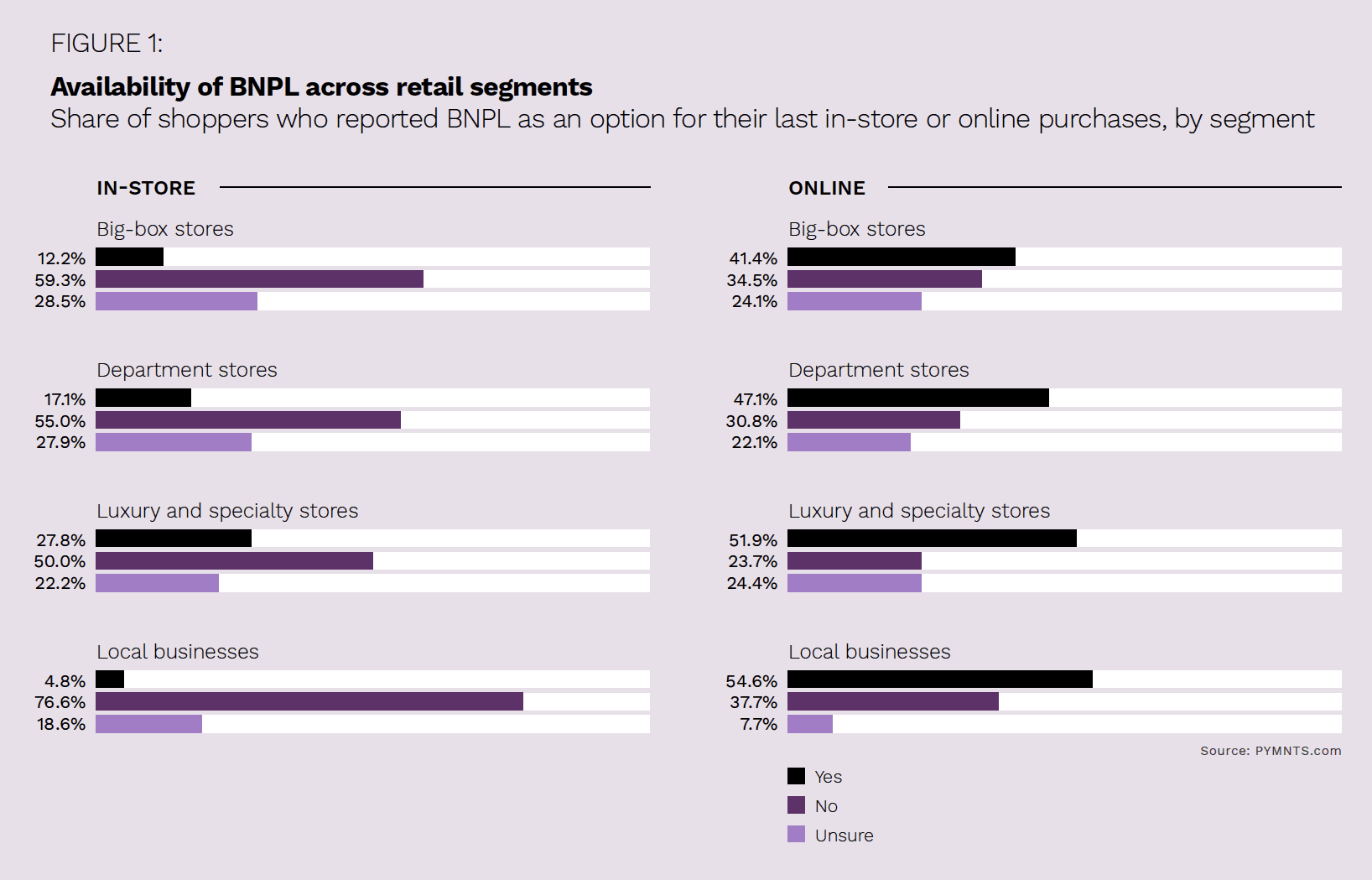

There is still much unmet demand for BNPL in the big-ticket arena, however. PYMNTS’ research found that 56% of surveyed shoppers would be interested in using BNPL for purchases at online luxury retailers, and nearly as many — 53% — would be interested in using it in-store. Two-thirds of bridge millennial and millennial consumers said they think highly of luxury and specialty merchants that offer BNPL options, and 55% of luxury and specialty store shoppers said they would switch to a different retailer if installment payment plans were not available. This demand is further evidenced by a growing rate of BNPL usage among more affluent consumers, with 12% of individuals who make more than $100,000 annually saying they leveraged a BNPL payment plan within the past 12 months.

There is still much unmet demand for BNPL in the big-ticket arena, however. PYMNTS’ research found that 56% of surveyed shoppers would be interested in using BNPL for purchases at online luxury retailers, and nearly as many — 53% — would be interested in using it in-store. Two-thirds of bridge millennial and millennial consumers said they think highly of luxury and specialty merchants that offer BNPL options, and 55% of luxury and specialty store shoppers said they would switch to a different retailer if installment payment plans were not available. This demand is further evidenced by a growing rate of BNPL usage among more affluent consumers, with 12% of individuals who make more than $100,000 annually saying they leveraged a BNPL payment plan within the past 12 months.

Why Big-Ticket Merchants Should Deploy BNPL

BNPL offers high-end retailers the same benefits as it does other sectors: It leads to larger transactions and increased customer conversion. Research has shown that 64% of BNPL users are more likely to purchase if BNPL is available, for example, and merchants that advertised the ability to split purchases into smaller installments saw a 56% increase in average order volume.

These improved sales numbers are likely to continue increasing over time as older and more affluent shoppers become more familiar with BNPL services. More than 46% of baby boomers and seniors and 71% of BNPL users with incomes over $100,000 increased their use of BNPL in the last year. The numbers should continue to increase as inflation and other financial pressures have these segments looking for ways to manage finances, whether for necessities or more discretionary purchases.

PYMNTS’ research additionally found that shoppers who currently do not use BNPL are willing to do so to finance large, one-time purchases. Forty-three percent of consumers want to use BNPL options to remodel their homes, earn a new educational certification or process other large transactions over several smaller installments. Millennials and bridge millennials, already avid users of BNPL for everyday purchases, are the most interested in this use case at 62% and 59%, respectively.

BNPL can also be a helpful option for a high-priced, time-sensitive purchase that people may not be willing to wait for, such as an engagement ring, or an unexpected expense, such as a new sofa. Using BNPL to fund big-ticket items is a strategy that can attract new customers and build loyalty across existing customer bases.

Merchants that manage to tap into these growing BNPL cohorts could find themselves well set for the future. Big-ticket items have long been purchased with traditional financing options, so extending this tradition to include BNPL is sure to succeed.