Retailers are having a rough go of it in 2022. Inflation is at 9.1%, according to the consumer price index, and supply chain disruptions mean inventory shortages that frustrate both merchants and consumers. The pandemic continues to linger as well, with outbreaks and new variants unexpectedly disrupting staff schedules and consumer spending habits.

Buy now, pay later (BNPL) has proven to be quite effective at encouraging consumer spending amid this economic uncertainty. Businesses that offer BNPL services have enjoyed larger ticket sizes, more frequent customer visits and a host of other benefits that are keeping retailers afloat.

This month’s PYMNTS Intelligence examines the multipronged obstacles retailers are currently facing and how BNPL can help them weather the continuing storm.

Retail’s Economic Hardships

Prices are at the top of shoppers’ minds as inflation curbs their spending power. Half of consumers would switch brands to save money, and many are also shifting their shopping channel preferences. Seventy-two percent of eCommerce sales occur via mobile device, and retailers without strong mobile presences could find themselves hard-pressed to cultivate customer bases — especially among younger generations.

BNPL services have not been immune to these obstacles. Adding to this economic pressure are new regulations from world governments that seek to crack down on the largely unregulated BNPL industry. The United Kingdom, for example, began its BNPL regulation process in 2021, and Australia is exploring options similar to those in the U.K., expressing its intent to treat BNPL providers like other small-scale lenders.

Leveraging BNPL to Counter Economic Hardships

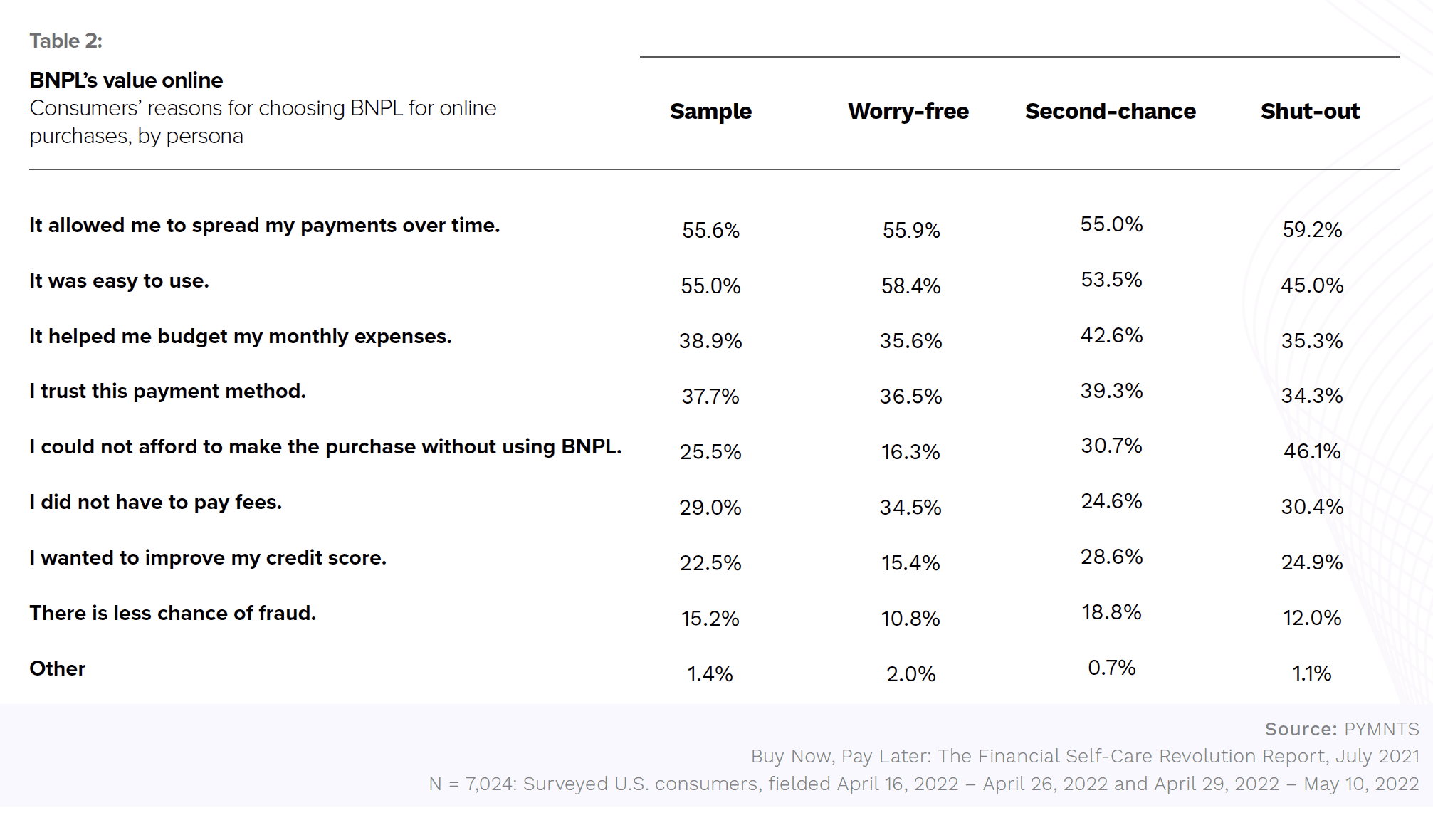

BNPL incentivizes consumers to make potentially daunting purchases despite economic hardship. PYMNTS’ research found that 46% of customers who could not access traditional credit options used BNPL offerings to make purchases they could not have afforded otherwise. Forty-seven percent of consumers said they would be interested in BNPL for expensive, one-time retail purchases.

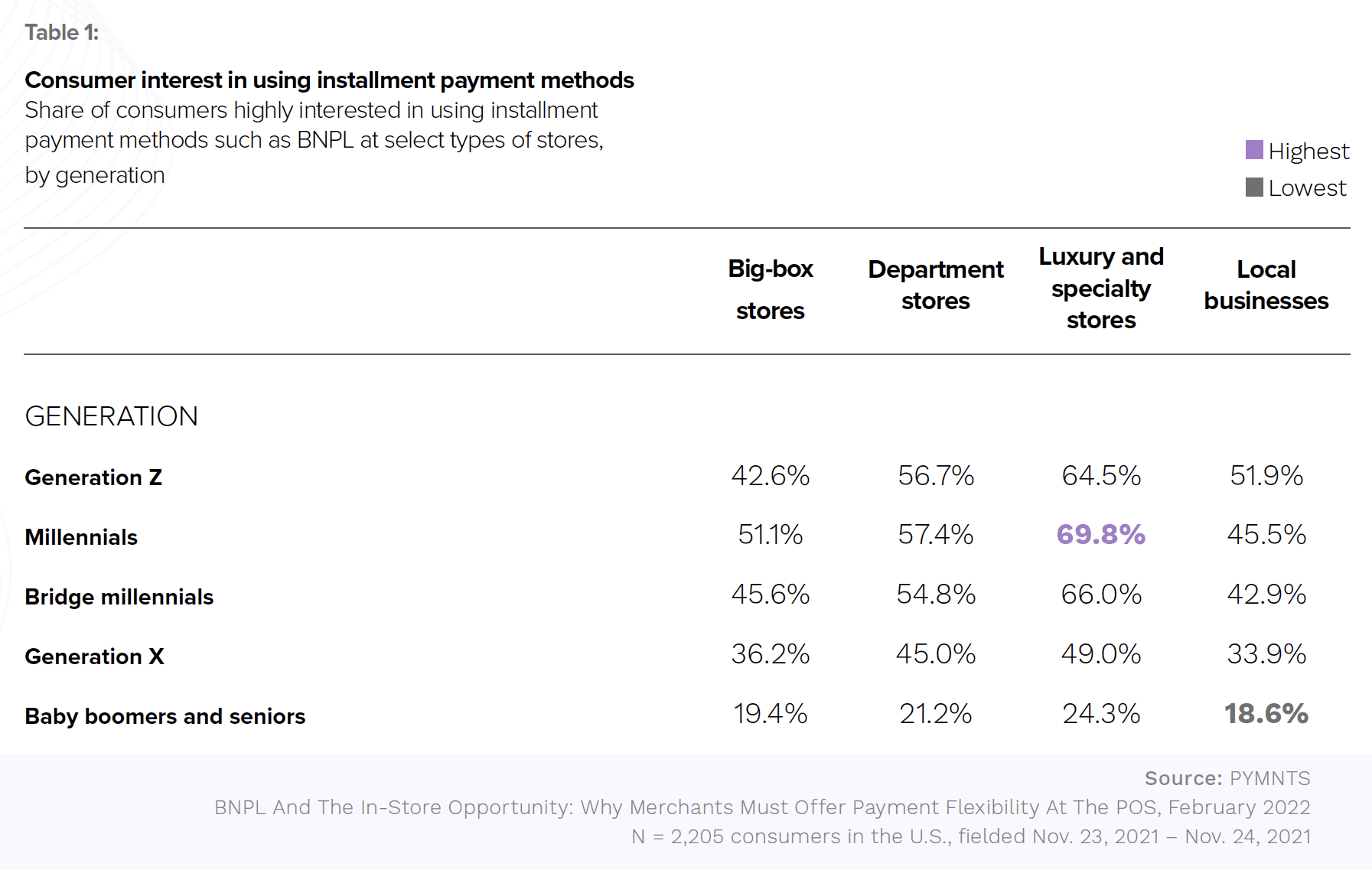

BNPL services are especially popular among younger generations such as millennials and Generation Z. Fifty-six percent of Generation Z shoppers said they were highly interested in using BNPL options at department stores, and 52% were interested in doing so at local businesses. These shares were 57% and 46% among millennials, respectively. Luxury and big-box stores are also common targets for BNPL use, but these would be common uses even without the current economic environment.

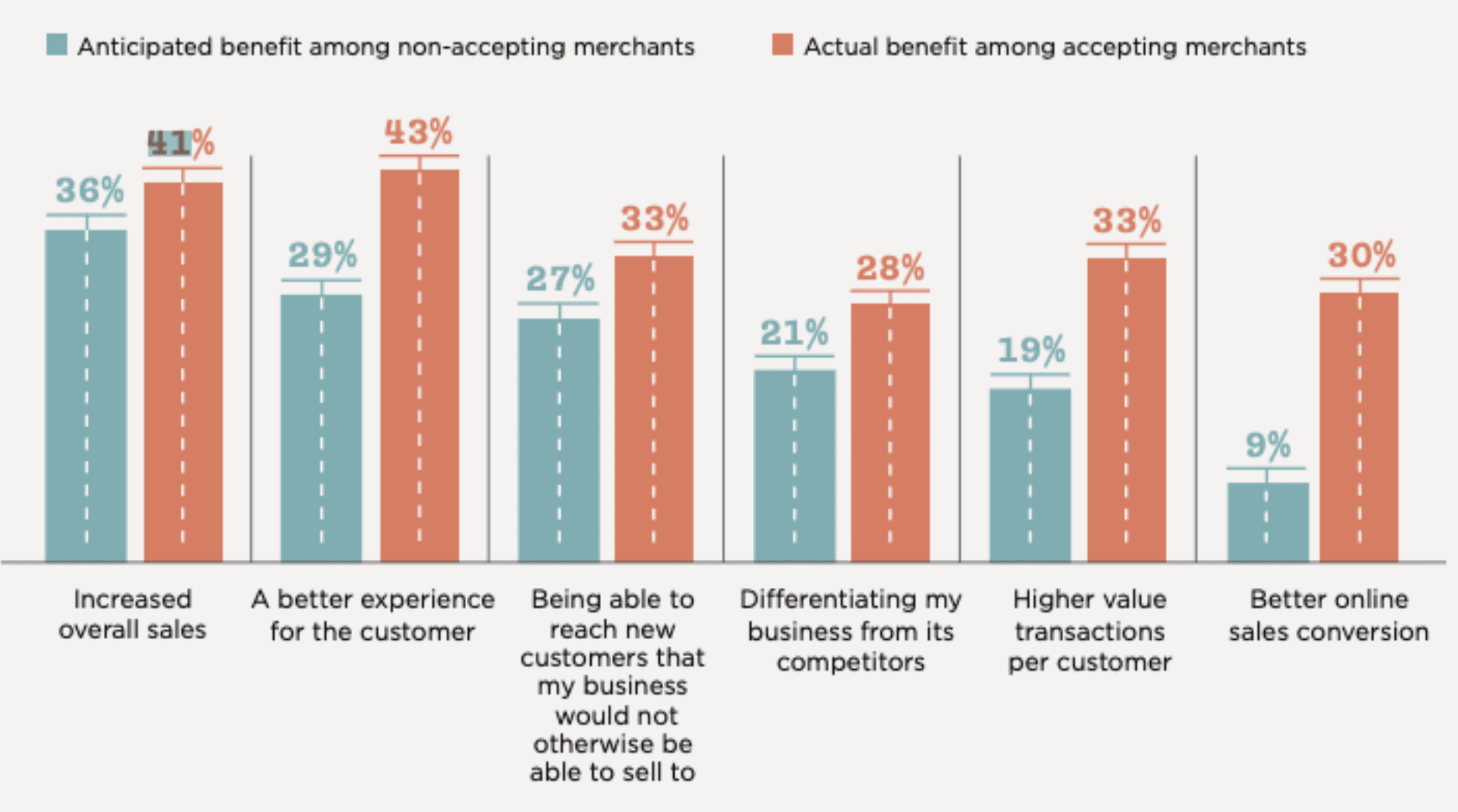

Merchants’ attitudes toward BNPL are no less sunny. Forty percent of Unites States retailers that offered BNPL said they did so to increase their businesses’ online sales, along with 25% of Canadian retailers. Once implemented, 41% of U.S. merchants found that overall sales had increased, 33% saw higher-value transactions and 30% reported higher online sales conversion. Equally important was that 43% reported better customer experience, which, although less quantifiable, is essential for fueling return visits.

The current economic climate is tough for both retailers and consumers. BNPL services offer the opportunity for both groups to benefit if the current economic climate continues for the foreseeable future.

Source: Author unknown. The Global State Of BNPL: How Banks And Providers Can Champion And Leverage Customer Interest To Succeed. 2022. https://rfi.global/wp-content/uploads/2022/03/RFI-Global-Report-The-Global-State-of-BNPL-How-Banks-and-Providers-Can-Champion-and-Leverage-Customer-Interest-to-Succeed.pdf. Accessed August 2022.