With BNPL, customers can typically choose to make smaller, more manageable payments over time rather than paying the full amount all at once. This can be an attractive option for customers who want to spread the cost of a purchase over a longer period or who may not have the credit or financial resources to qualify for traditional financing options such as credit cards or loans.

BNPL is usually offered through a third-party provider, such as a financing company or a payment processor, which handles the transactions and billing. Customers typically need to create an account with the provider and provide some personal and financial information to qualify for the service.

It’s important to note that BNPL is not a free service, and customers will ultimately pay for their purchases, often with additional fees or interest charges. It’s important for customers to carefully read and understand the terms and conditions of any BNPL offer before agreeing to it, making sure that they can afford the payments and fees associated with the service.

BNPL plans are offered by retailers as an alternative to traditional credit card payments and are often used for online purchases. Some popular BNPL companies include Affirm, Afterpay, Klarna and Sezzle.

Here’s how it typically works:

Advertisement: Scroll to Continue

- The consumer selects the BNPL option at checkout when making a purchase.

- The consumer agrees to the terms and conditions of the BNPL service, which may include a deferred payment schedule and fees for late payments or missed payments.

- The merchant processes the transaction, and the consumer receives the goods or services.

- The consumer pays off the balance according to the payment schedule agreed upon at checkout.

BNPL services may be offered by the merchant or a third party, such as a financial institution or a payment processor. Some BNPL services may require the consumer to set up an account and provide personal and financial information. Others may only require a valid debit or credit card for payment. Consumers need to understand the terms and conditions of a BNPL service, as failure to make payments on time can result in late fees and damage to the consumer’s credit score.

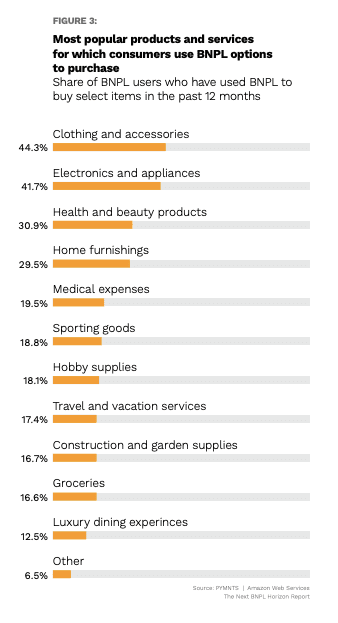

Common uses of BNPL revolve around nonessential items, from consumer electronics to big-ticket outlays, including travel and durable goods. According to the study The Next BNPL Horizon Report: Expanding Access To High-Value Services, a PYMNTS and Amazon Web Services collaboration, “Millennials and bridge millennials are the most enthusiastic about using BNPL plans, as they are the two age groups most likely to be living paycheck to paycheck. Sixteen percent of both millennials and bridge millennials have made at least one BNPL purchase in the past year. No other generation comes close except for Gen X, 14% of whom have made at least one BNPL purchase in the past year.”

Get the Report: The Next BNPL Horizon Report: Expanding Access To High-Value Services

BNPL or Credit Cards?

Buy now pay later (BNPL) and credit cards are both forms of financing that allow consumers to make purchases and pay for them at a later date, but there are some key differences:

Interest charges: Credit cards generally charge interest on unpaid balances, while BNPL services may not charge any interest, at least for a certain period. However, some BNPL services may charge fees for late or missed payments, so it’s important for consumers to carefully read and understand the terms and conditions before using a BNPL service.

Credit check: Some BNPL services may not require a credit check, while others may conduct a soft credit check that does not affect the consumer’s credit score. On the other hand, credit card issuers typically conduct a hard credit check, which can impact the consumer’s credit score.

Credit limit: Credit cards generally have a credit limit, the maximum amount the consumer can charge to the card. BNPL services may not have a credit limit, but the amount the consumer can borrow may be limited by the value of the goods or services being purchased.

Rewards: Many credit cards offer rewards, such as cashback or points, for using the card. BNPL services may not offer any rewards.

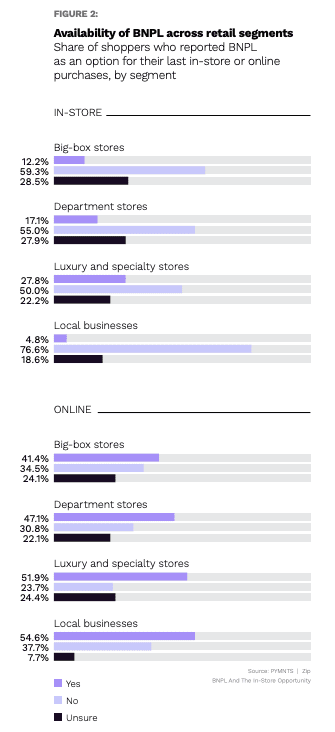

BNPL use in-store is rising, but it remains largely an online payment method.

The study BNPL And The In-Store Opportunity, a PYMNTS and Zip collaboration, states that “BNPL was offered for roughly half of consumers’ most recent online purchases across retail segments but available for less than one-fifth of in-store purchases. The gap between online and in-store availability of BNPL was most dramatic for consumers making purchases from local businesses: Online, 55% of these entities offered BNPL, while just 4.8% offered the method in-store.”

The smallest availability gap was observed among consumers shopping at luxury and specialty stores, with BNPL offered for 52% of their most recent online purchases and 28% of their in-store purchases. At department stores, BNPL had 47% availability for online purchases and 17% in-store. Big-box stores had 41% availability online but only 12% in-store, per the study.

Get the Report: BNPL And The In-Store Opportunity