Earnings season’s not over yet — and the picture on consumer spending is mixed thus far.

The payment networks and banks have noted that though consumers still are using their cards, there have been some pullbacks by lower-income households. The Federal Reserve’s latest survey on consumer credit detailed that use of revolving debt — which includes credit cards — slowed to an annualized pace of 0.1% in March, down from a more than 9% rate in the previous month.

Spending can be and often is lumpy, and the total first quarter revolving debt grew at 5.7%. But that’s lower than the 7.5% rate in the fourth quarter of 2023, and significantly below the year-over-year 9.7% rate that had been calculated a year ago.

For buy now, pay later (BNPL) providers, pockets of significant growth are showing through, lifting the fortunes of publicly-traded firms, and providing evidence — dovetailing with PYMNTS Intelligence’s own data — of acceleration in key categories such as clothing and travel.

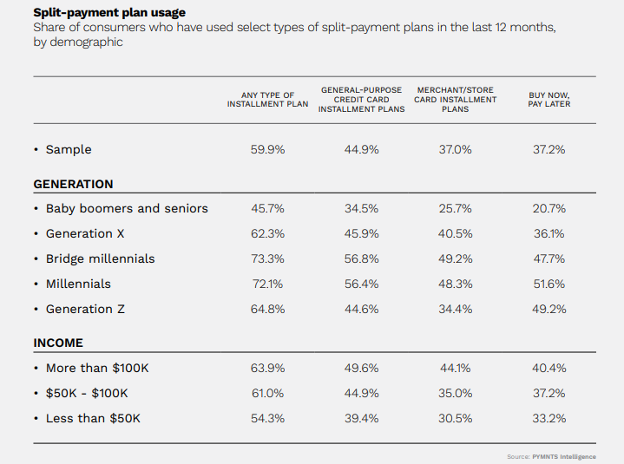

Coming into earnings, PYMNTS Intelligence, in collaboration with Splitit, found that three in five consumers said they’d used some split-payment option at least once in the last year.

Getting a bit more granular, the surveys indicate that 37% of consumers had used BNPL. More than a third of the lowest income consumers had opted for BNPL, a share that increases the higher up the income bracket one goes.

Those who tried it, liked it. PYMNTS Intelligence/Splitit found that a full 79% of consumers had a favorable experience with the product.

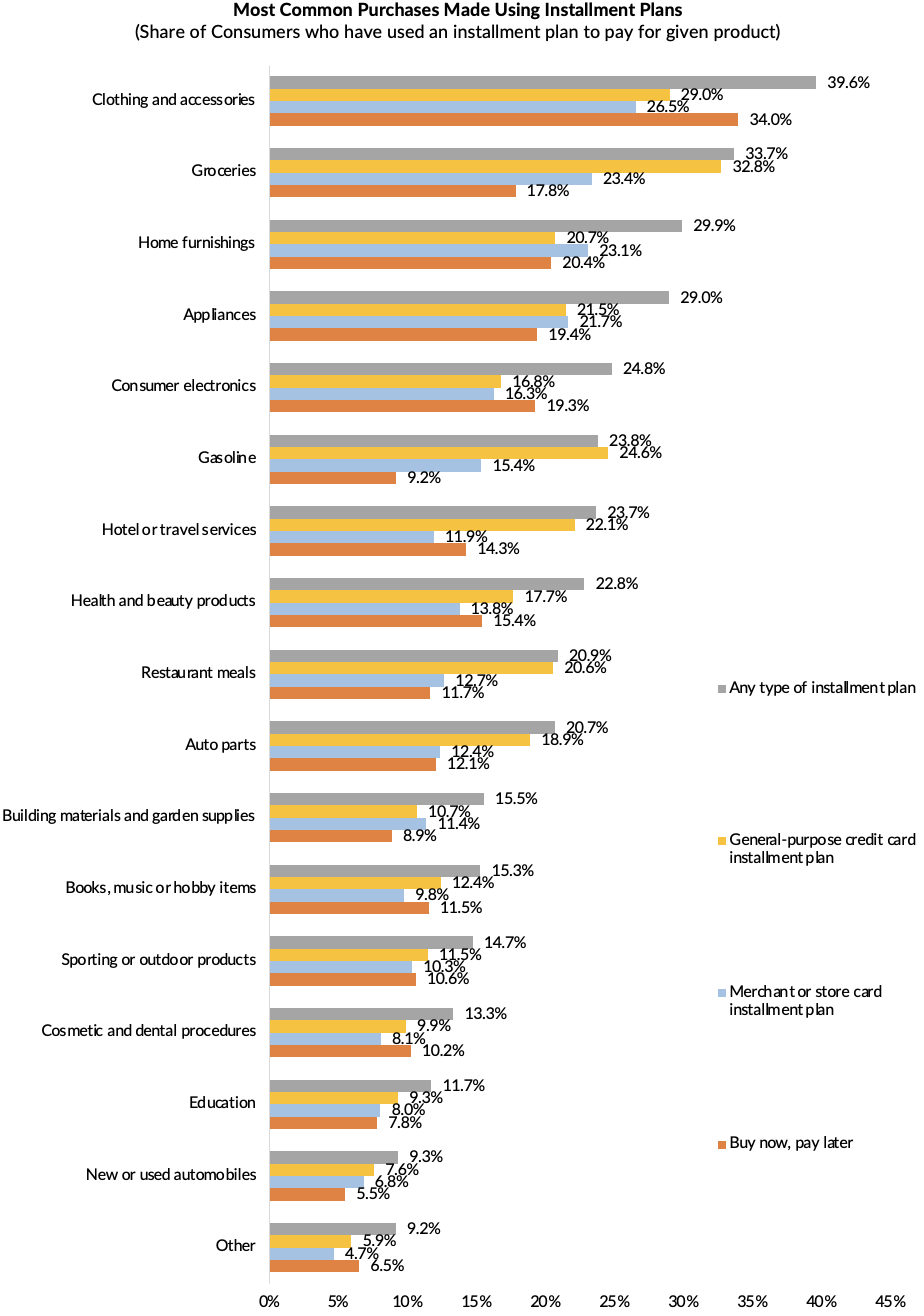

As to what they’ve been buying, the chart below indicates that of the consumers using installment plans, more than a third had used BNPL to buy clothes and accessories, 18% had done so with groceries and more than 14% had chosen BNPL when paying for travel-related services.

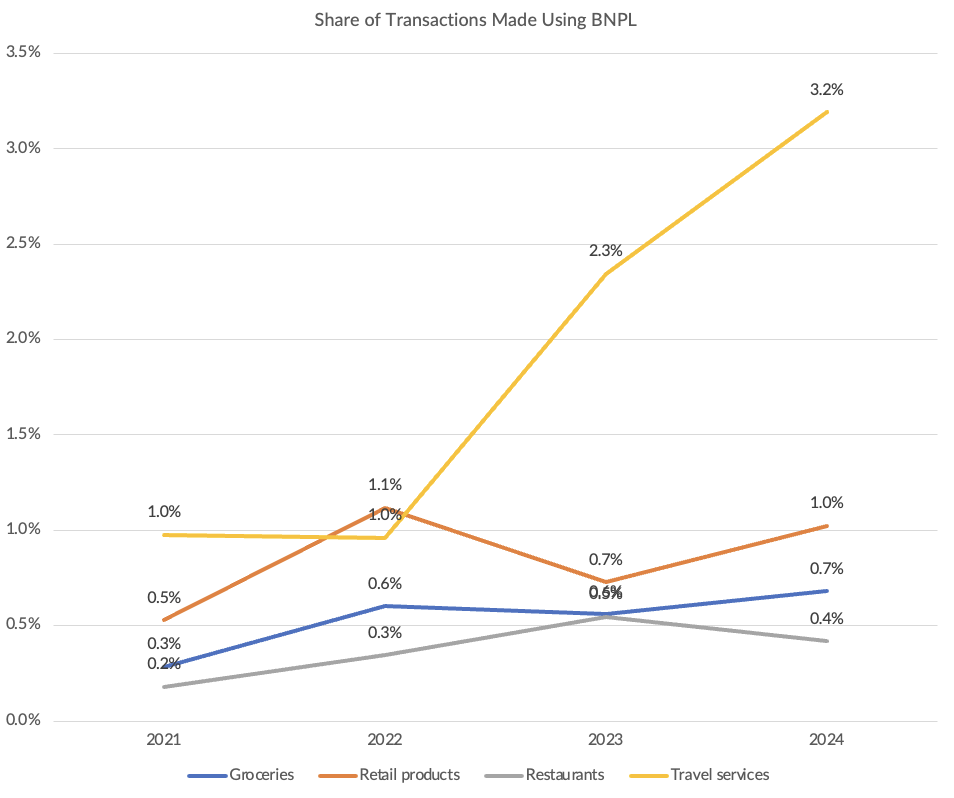

According to the chart below, which uses data from this spring based on surveys with about 2,000 consumers across three key categories, more than 3% of consumers had used BNPL to pay for travel as their most recent transaction, and a much smaller percentage had done so in the other categories. The runway, then, is long for BNPL adoption.

Earnings season corroborates the gathering momentum.

In Block’s first quarter report, management noted that BNPL gross merchandise value (GMV) was $6.98 billion in the first quarter, up 25% year over year.

And separately, on Wednesday (May 8), Affirm’s fiscal third quarter results disclosed 51% growth in revenues to $576 million, as well as 4.7 transactions per average user (up 25% year on year), which indicates stickiness with the installed base. Affirm also provides a quarterly update on spending categories. In the latest reading, spending in general merchandise surged 49%, fashion and beauty was up 17% and travel/ticketing grew by 35%.

Sezzle’s report, just out after the bell on Wednesday, said that total income was up 35%. The company said in its earnings release that underlying merchant sales rose by 33.2% to $492.7 million year on year, while consumer purchase frequency increased to 4.5 times in the latest quarter, up from 3.1 last year.

In the current environment, high interest rates on cards and the aforementioned slowdown in “traditional” revolving credit debt may be further grist for BNPL adoption.

Coming into the end of 2023, about a third of consumers living paycheck to paycheck said they’d used BNPL, according to PYMNTS Intelligence. Additionally, 30% of survey respondents indicated that the low or nonexistent interest rates contributed to their decision to apply for BNPL. Roughly 19.4% valued the fact that the BNPL options did not require a hard credit check. For 10% of the BNPL-using population, consumers said they would not be able to cover bills were BNPL not on offer.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More