Younger consumers are navigating early-stage careers and key earnings years under the shadow of the pandemic and the resulting economic crisis, and many also entered the job market during the 2008 Great Recession.

These inauspicious events as well as other trends like rising education costs and sluggish wage growth have all put millennials and Generation Z into tighter financial situations that have made it more difficult for them to afford to pay out-of-pocket for larger, high-value purchases.

The March edition of PYMNTS’ “Buy Now, Pay Later Tracker®” examines how financial challenges like these are leading many younger consumers to turn to credit offerings like buy now, pay later (BNPL), which allow shoppers to pay off large-ticket items over four installments. The Tracker examines use of BNPL among millennial and Gen Z populations and its impact on their shopping behaviors.

Around The Buy Now, Pay Later Landscape

United States consumers ramped up their BNPL use in 2020, during which Gen Z’s spending with the payment method rose 201 percent year over year. Some observers in the space suggest that young shoppers may use BNPL as an intermediary tool for when they need to move beyond the spending limits of debit cards but do not yet qualify for credit cards. Other consumers may simply prefer BNPL plans to credit cards. Some BNPL plans charge flat late fees instead of interest, while others charge varying amounts of interest.

Young adults in India are also showing considerable interest in BNPL, where one local installment loan provider said the tools can help millennials purchase the kinds of big-ticket items that adults in that stage of life often want to acquire. The installment payment plans appear to be particularly popular among co nsumers buying large appliances and expensive electronic devices, according to other BNPL providers.

nsumers buying large appliances and expensive electronic devices, according to other BNPL providers.

These installment payment plans also seem to be making greater inroads in the traditionally cash-heavy Middle East. More than 10 BNPL providers launched in the region last year, for example, and the payment method can replace traditional methods of paying for eCommerce orders via cash on delivery.

For more on these and other stories, check out the Tracker’s News & Trends section.

Carhartt On Converting Younger Consumers With BNPL

Younger shoppers may not be able to comfortably afford all the goods they want from certain brands until they progress higher in their career and income levels. BNPL can make a difference, however, by splitting prices into installments that are easier for consumers to tackle.

This can be key to helping brands attract millennial and Gen Z shoppers, explained Anna Cole, director of direct-to-consumer (D2C) global digital platforms for workwear retailer Carhartt. In this month’s Feature Story, Cole explains how offering BNPL can drive brand awareness, lead to larger and more frequent orders and help merchants appeal to wider customer bases.

To get the full story, download the Tracker.

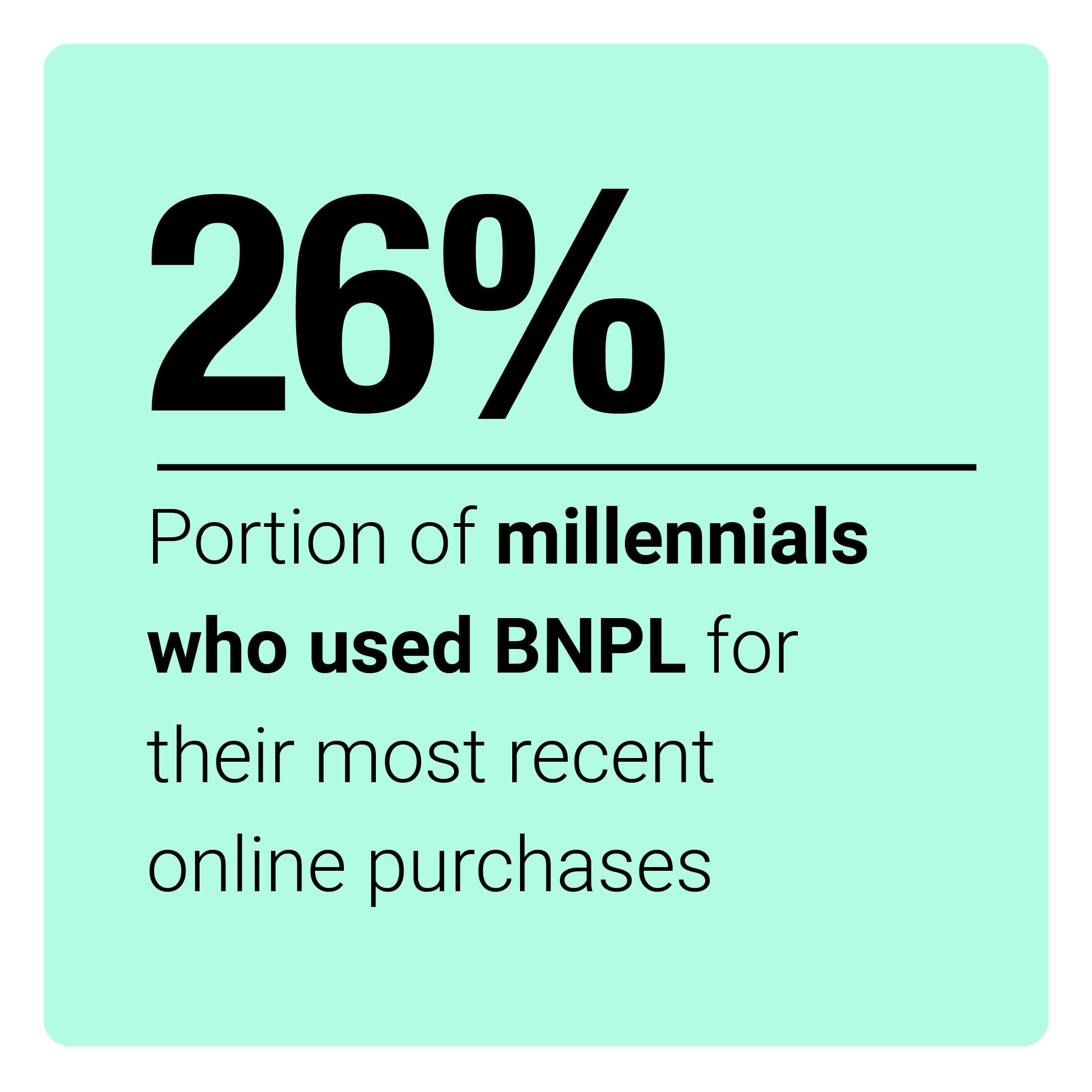

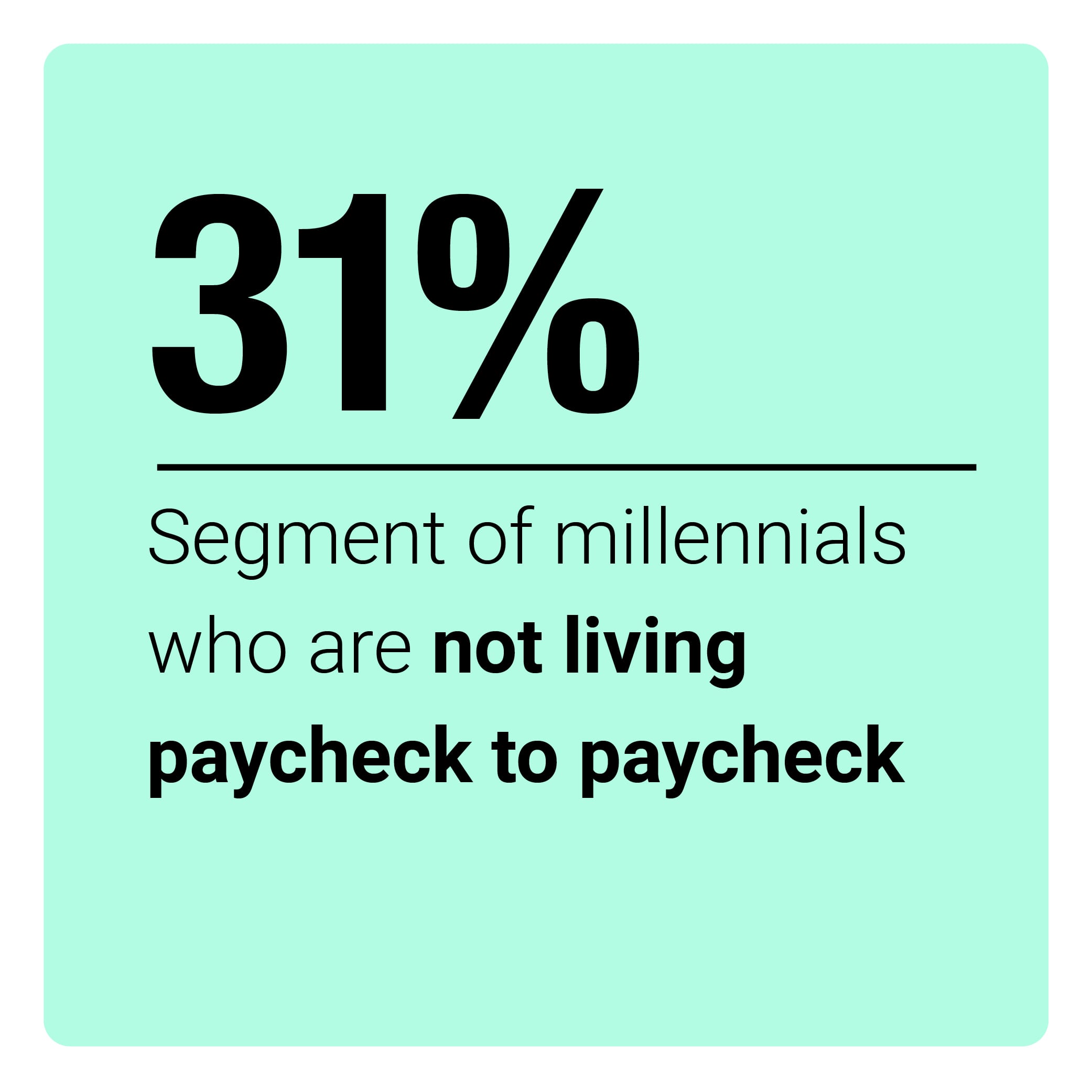

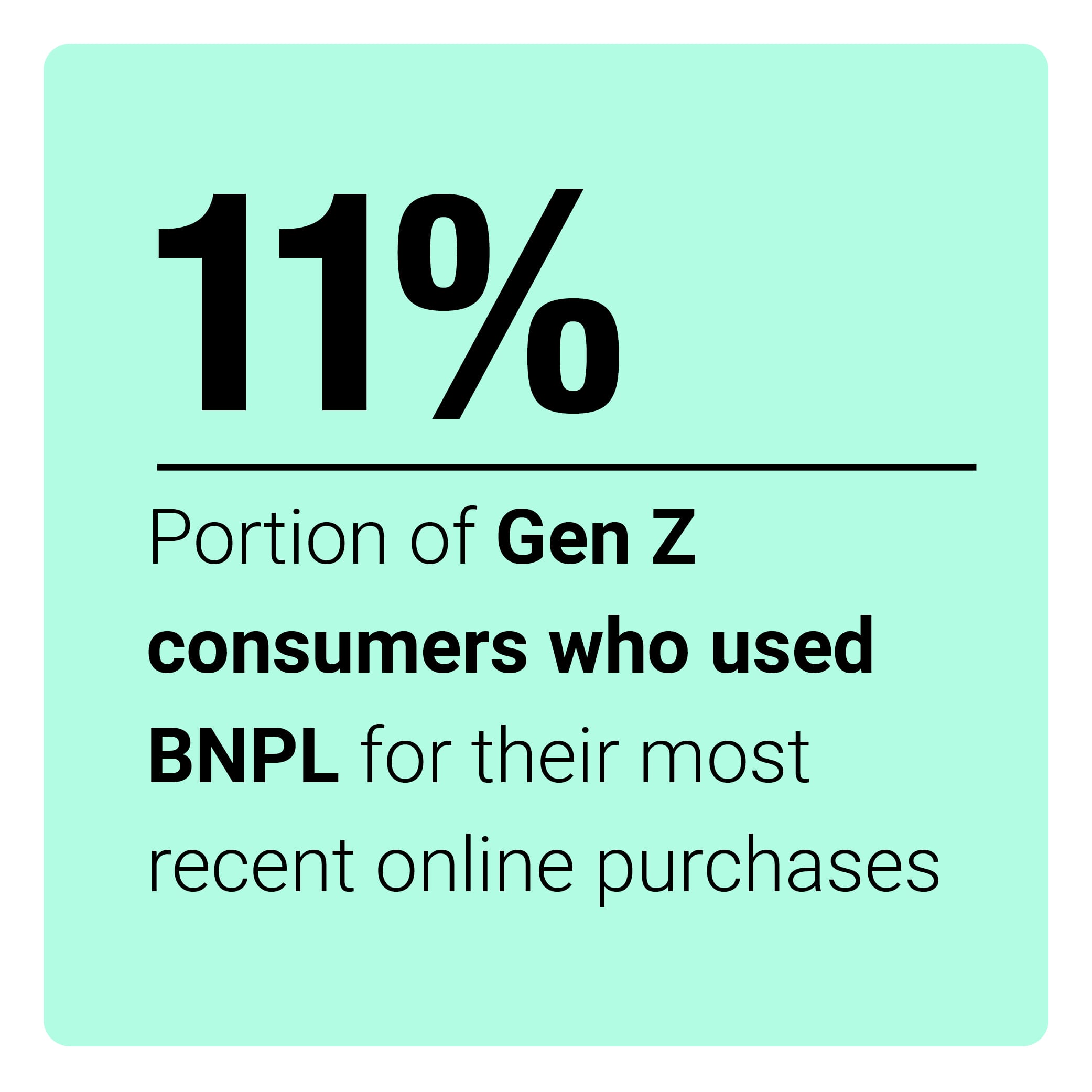

Deep Dive: Analyzing the Driving Factors Behind Gen Z, Millennials’ BNPL Usage

New PYMNTS research charts various generations’ uses of BNPL plans, detailing the way that Gen Z and millennial consumers are turning toward the option for both in-store and online retail purchasing to greater extents than their older counterparts. The Deep Dive examines these trends as well as investigates how intergenerational differences in financial stability may be influencing these purchasing behaviors.

Read the full Deep Dive in the Tracker.

About The Tracker

The “Buy Now, Pay Later Tracker®,” a PYMNTS and Afterpay collaboration, brings you the latest news and research from the buy now, pay later space. This edition offers new insights into how installment payment plans can help merchants convert younger consumers and develop greater brand awareness.