Some people went into the pandemic with financial troubles, while for others pandemic effects on employment caused late or missed payments and other credit score blemishes.

More Americans are affected than we may imagine, as those living paycheck-to-paycheck include high-earning millennials that aren’t thought of as financially strapped.

In The Second-Chance Consumer: How Buy Now, Pay Later Payments Create New Merchant Opportunities, a PYMNTS and Sezzle collaboration, researchers examined the use of buy now, pay later (BNPL) alternative credit as a primary means to give a hand up to those struggling.

Per the study, “a second-chance consumer is not necessarily a consumer who would be an unreliable or undesirable shopper. We found that 65 percent earn more than $50,000 per year, with 30 percent earning above $100,000. The average second-chance consumer is 44 years old and has a FICO score of 662,” or only 38 points less than the average ‘good’ credit score.

Giving these consumers access to point-of-sale credit is a source of revenue for merchants that benefits shoppers as well, potentially impacting everything from cart size to future loyalty.

BNPL Budgeting Is a Thing Now

While BNPL is achieving stardom making purchases easier by breaking them into affordable installments, it’s other emerging use is as a personal budgeting tool. And for some consumers, BNPL is a better budget fit than credit card usage — for those who even have revolving credit.

Per the study, “many consumers see BNPL as a way to stretch their budgets. This perception gives merchants that offer BNPL payment options a powerful appeal to consumers who have endured financial challenges in the past 18 months.”

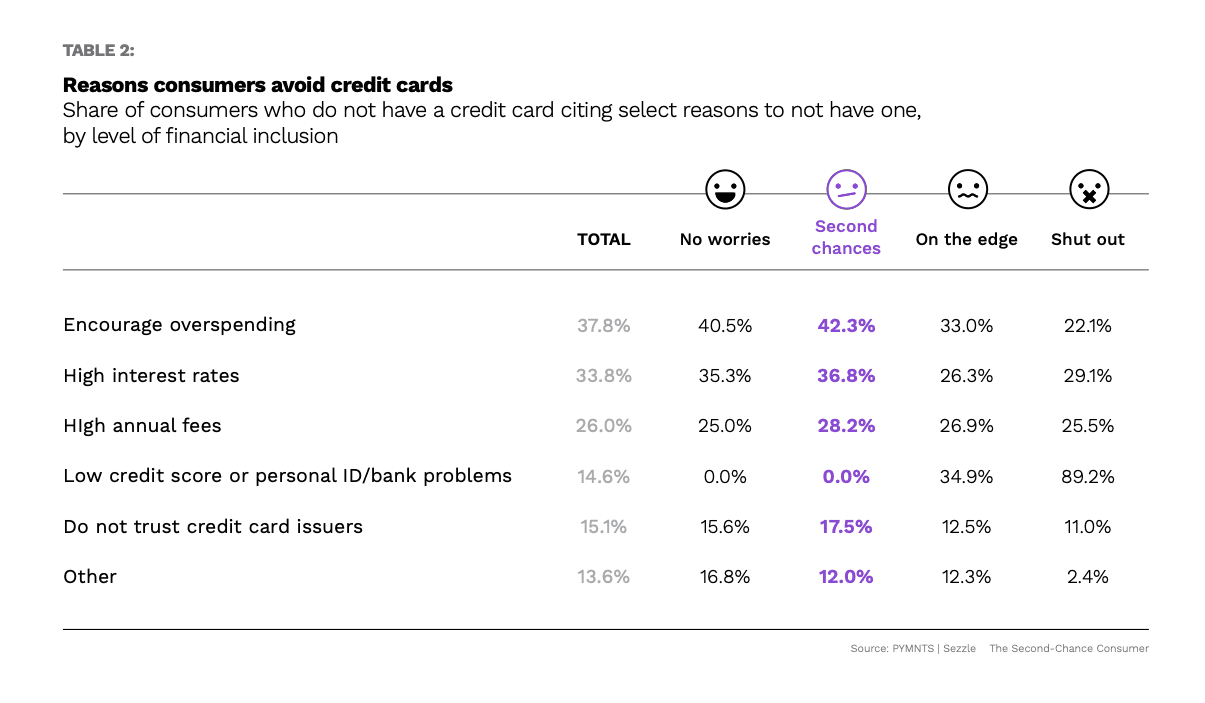

“A second reason that BNPL is a popular option among second-chance consumers exists: such consumers are hesitant to add to their debt burden, even if credit is available.” Researchers found that 42 percent of second-chance consumers without access to credit cards don’t want them.

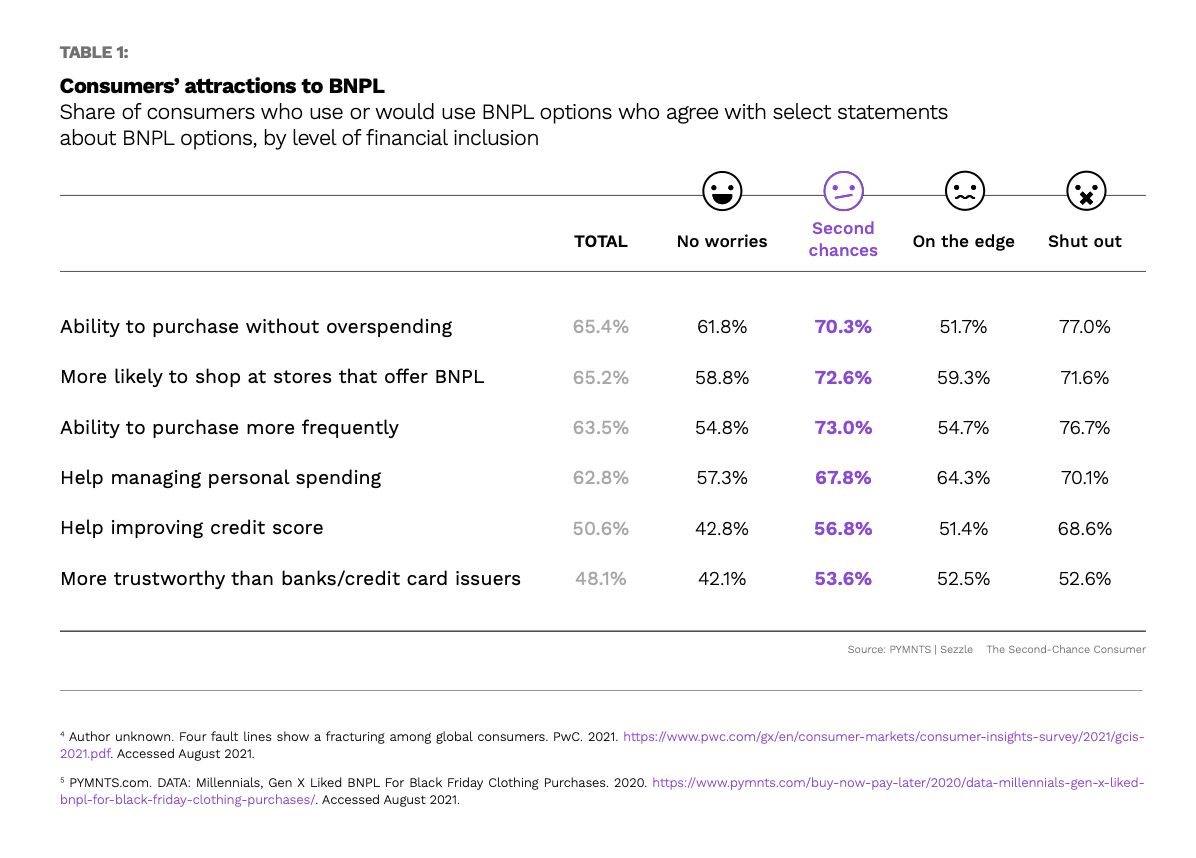

In fact, fully 70 percent of second-chance consumers familiar with BNPL “view it as an option that improves their ability to buy things they want without overspending. BNPL helps consumers stay within budget while empowering them to make purchases without the added burden of revolving credit,” the study states.

An Alternative to Costly Credit Use

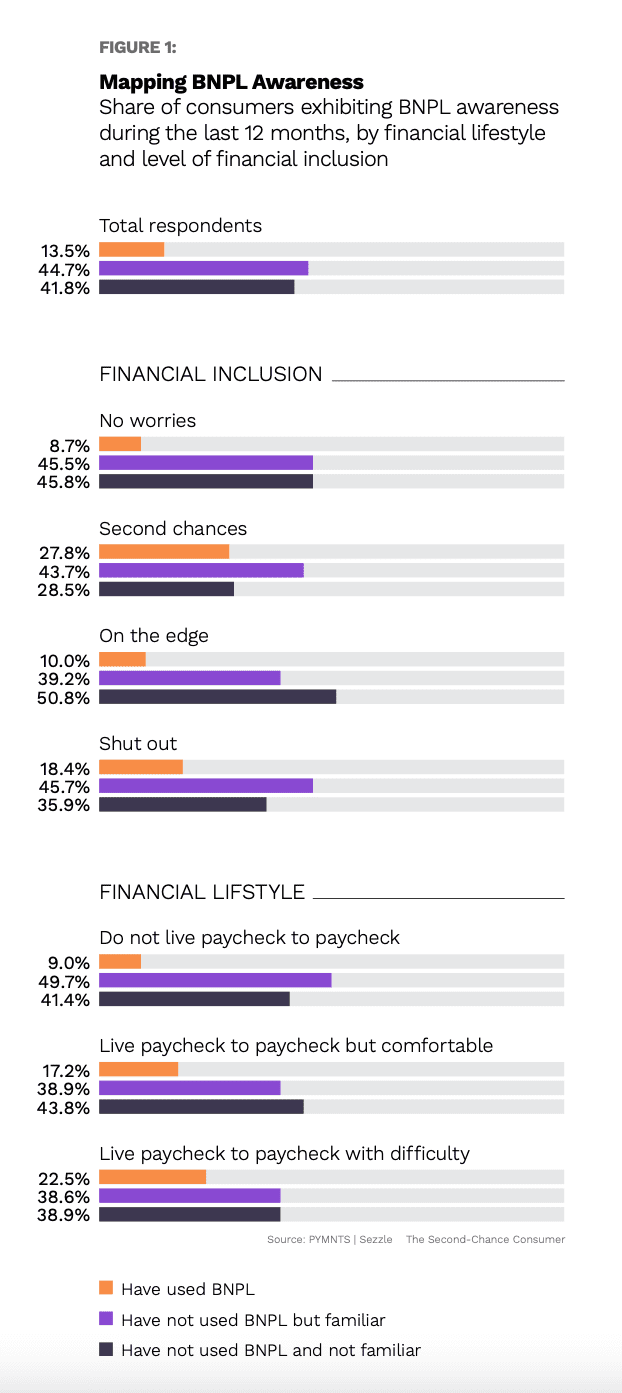

As use cases for BNPL expand beyond its original base of fashion and cosmetics shoppers, applications like credit access and credit repair are gaining awareness and popularity.

The study notes, “A large share of second-chance survey respondents who have chosen to use BNPL as a checkout option online said it allowed them to spread their payments over time (55 percent) and helped them manage their monthly expenses (43 percent). These two capabilities were second-chance consumers’ most-cited benefits, yet notable shares of respondents also said it allowed them to avoid fees (25 percent) and held less chance of fraud than other payment methods (19 percent).”

Courting the second-chance consumer with BNPL pays off for merchants too, of course.

Researchers found that 73 percent of second-chance consumers who have used BNPL or would use it agree with the statement that the payment option “makes me more likely to shop at retailers that offer BNPL.” Another 73 percent of second-chance consumers said they like BNPL for more obvious reasons: its lets them to buy “more frequently than they would otherwise.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More