Struggling consumers are relying on payment plans for daily purchases as wages fall behind rising prices.

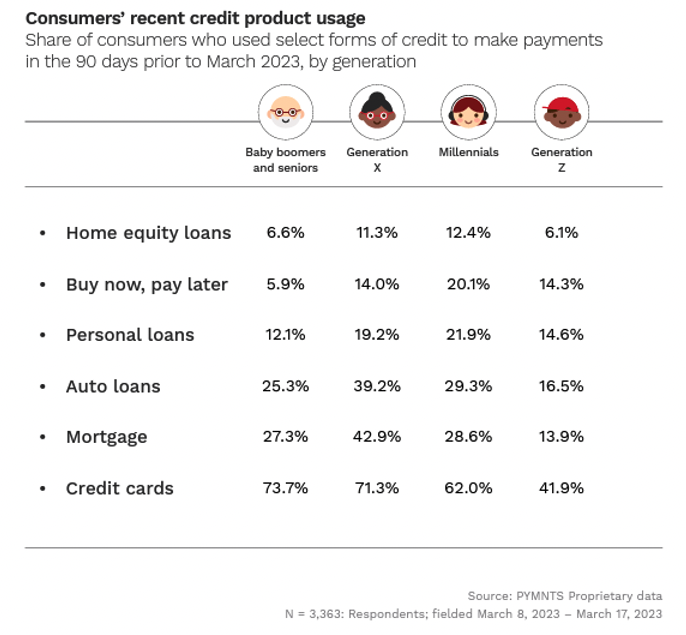

Nearly three-quarters of millennials are living paycheck to paycheck as seemingly ceaseless price increases force consumers to stretch their budgets further to keep up with the cost of living. Given these constraints, it may be no surprise that 43% of millennial consumers are increasingly relying on credit to get by.

But these days, as traditional credit becomes more difficult to obtain and expensive to maintain, some consumers are seeking alternative ways to pay for their day-to-day necessities. “The Credit Economy,” a PYMNTS and i2c collaboration, found that millennials in particular are using buy now, pay later (BNPL) platforms to do so.

Although double-digit shares of all generations besides baby boomers and seniors used BNPL plans in the 90 days before being surveyed, millennial use surpasses the other age demographics, at 20% to Generation X’s 14%.

To be clear, BNPL itself isn’t a problem. Installment payment programs, the modern-day successor to the layaway plans of yesteryear, can be a useful and helpful tool when making purchases that can’t be paid for right away. And with average card rates north of 20%, using BNPL to avoid the interest charges of traditional credit cards may be particularly appealing.

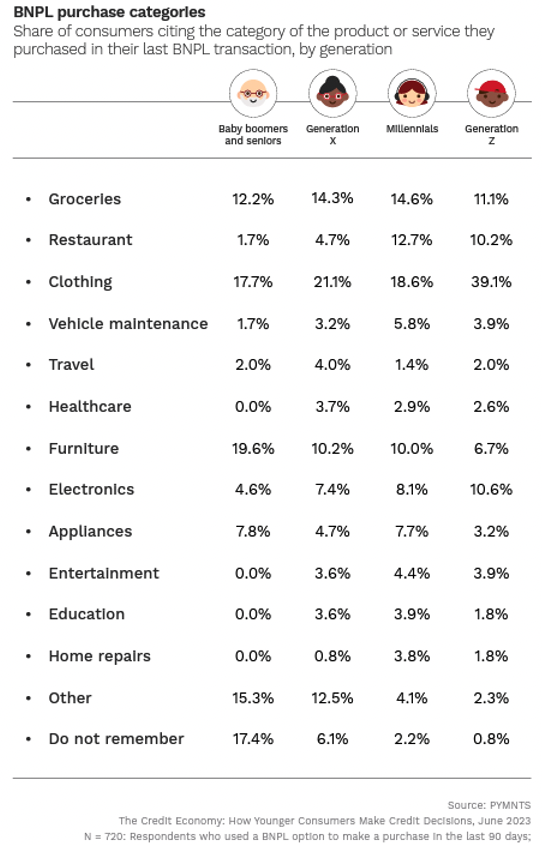

However, looking at what millennials are purchasing on these plans may signify a deeper issue.

Advertisement: Scroll to Continue

When it comes to buying groceries, perhaps the most essential of essential purchases, 15% of millennials have used BNPL. This comes as shoppers overall increasingly use the payment plan to buy food at home, as the grocery sector’s share of BNPL use grew nearly 40% between January 2019 and February 2023. While some of this share of BNPL use for essential purchases may be due to credit card rates’ rise, more consumers needing to put food on a payment plan would likely signify a deeper economic struggle.

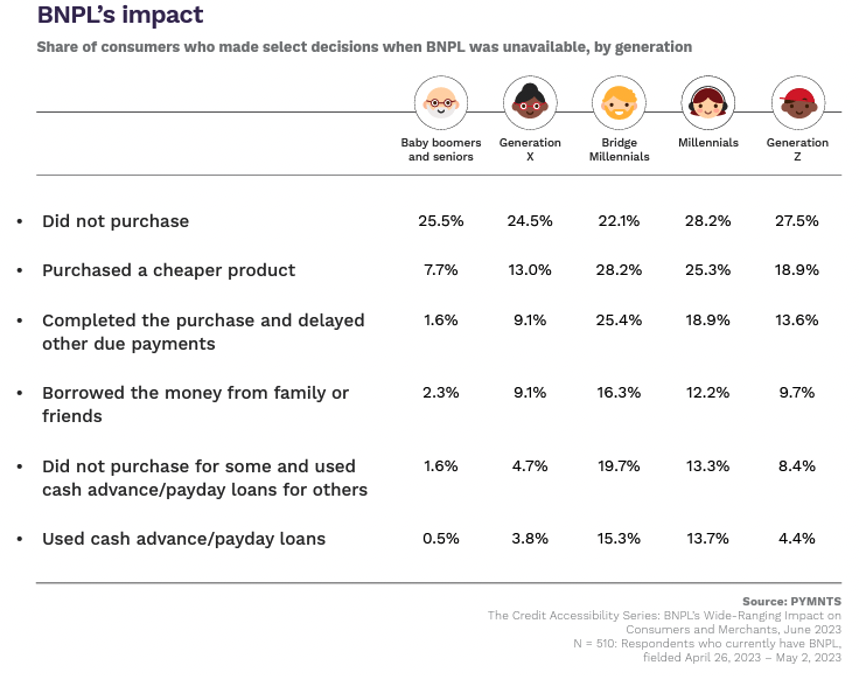

This reliance on BNPL among millennials for essential purchases does suggest that need is a factor when cross-referenced with their most-cited alternatives to BNPL, noted in “The Credit Accessibility Series,” a PYMNTS and Sezzle collaboration.

More than half of millennials either abandoned a purchase or ended up purchasing something cheaper when BNPL was not an available payment method. While it is difficult to discern if the 28% share of millennials who didn’t make a purchase due to BNPL’s unavailability gave up essential items in doing so, some percentage likely did.

As millennials in particular struggle with a paycheck-to-paycheck lifestyle, they may be more inclined to use alternative credit sources to purchase daily necessities. It remains to be seen if this buying behavior is sustainable, especially as other variables such as the restart of student loan repayments could come into play, affecting debt-holding consumers’ purchasing power.