Suburban consumers have a weaker perception of financial stability than those in urban communities, making them an interesting target group for certain credit products with low adoption, such as buy now, pay later (BNPL).

The study “New Reality Check: The Regional Divide Edition,” a PYMNTS Intelligence and LendingClub collaboration, studied urban, suburban and rural consumers and their financial preferences. It found that suburban consumers typically belong to older generations — baby boomers and seniors — and they often have high incomes. They use fewer personal loans but more credit cards than people living in other areas. Additionally, of the three groups, they experience the least difficulty making ends meet.

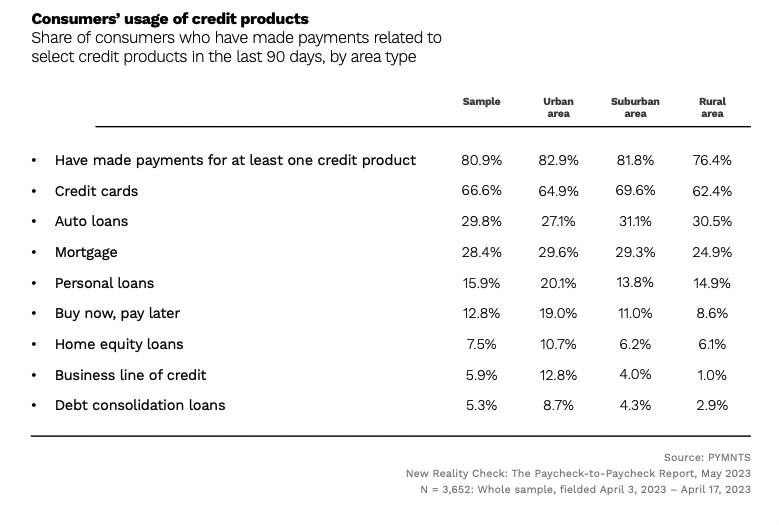

Use of Credit Products

According to the study, 55% of suburban consumers are the least likely to live paycheck to paycheck at 55%. Urban consumers are the most likely to live paycheck to paycheck, at 69%, followed by 63% of rural consumers. To manage their cash, suburban consumers primarily turn to credit cards. They reported the highest adoption rate of credit cards among all personas.

Conversely, the use of other credit options by this group fell behind other personas. For instance, only 11% of suburban consumers used BNPL, compared to 19% of urban consumers and 9% of rural consumers. One reason could be that the older consumers who belong to this segment are more used to operating with credit cards and revolving balances at the end of the month instead of splitting payments.

Suburban consumers will likely continue to live paycheck to paycheck, as nearly 84% of this segment said wage increases did not at least match inflation. Alternative credit products such as BNPL could help them better manage their finances in struggling times. Marketing efforts targeting this segment may allow financial institutions to capture this opportunity.