Digital engagement has become integrated in consumers’ everyday lives across the globe. One example: Mobile wallet use has been growing in-store, replacing some shoppers’ physical wallets, even in cash-heavier countries like Japan.

The PYMNTS’ Q3 2022 ConnectedEconomy™ Index, “How the World Does Digital,” measured the digital activity of 30,000 individuals across 11 countries. Tracked activities included transactional activities, such as purchases, and non-transactional activities, such as messaging or streaming. Overall, we found that global digital transformation is still trending upward, especially regarding daily engagement. Globally, 73% of consumer respondents engaged in one or more of the 37 digital activities the index tracks at least weekly. This indicates a more sustainable momentum than the spikes in sectors such as travel in the previous quarter and may predict a continued and steady growth in the coming future.

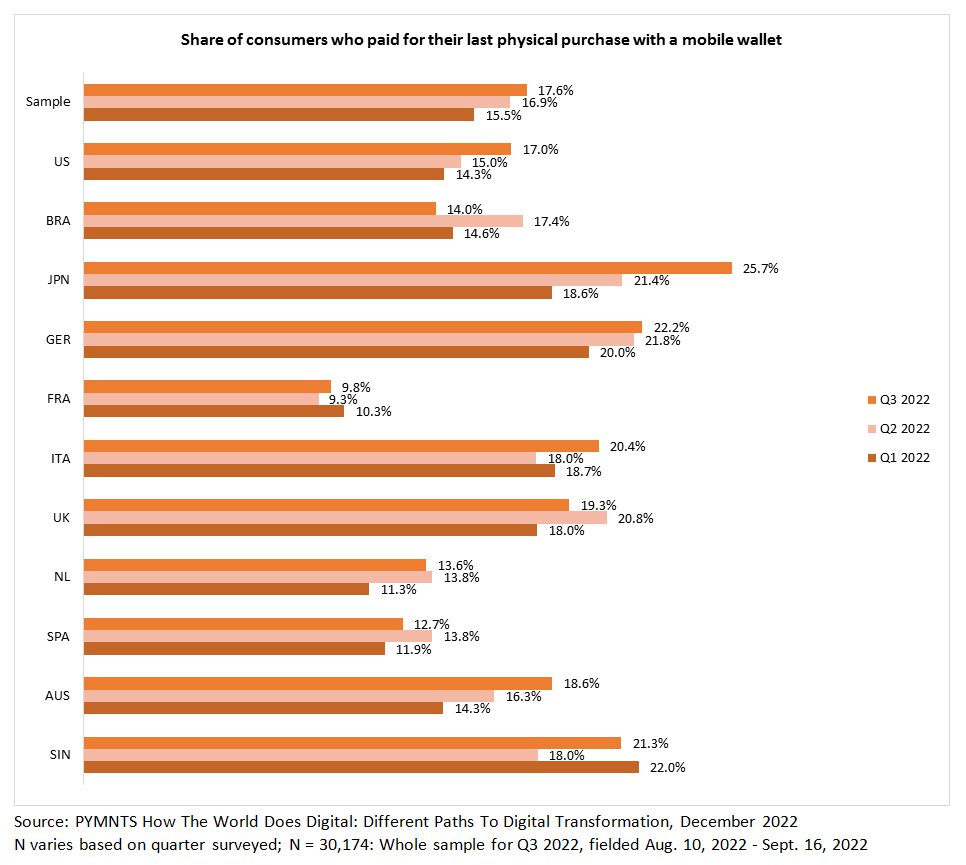

It is clear that mobile wallets have been on the rise. Overall, 16% of consumers paid for their last physical purchase with a mobile wallet in Q1 2022, but by Q3 that share had grown to 18%. We measured increased use by consumers in seven of the 11 countries the ConnectedEconomy™ Index follows. Japan experienced the fastest rate of mobile wallet growth in this manner and is now leading the field.

Japan’s rapid adoption of mobile wallet use for in-store transactions was particularly notable, as using cash for retail transactions is still common in the country. Also making this growth notable was that, of the 11 countries surveyed, Japan ranked last in the average number of activities conducted monthly, weekly and daily. Nevertheless, a 20% increase in mobile wallet use for physical transactions in the country occurred in the third quarter of 2022. And once the alternative payment method caught on, it did so quickly. Japan now boasts the highest adoption rate of mobile wallet use within a quarter and the highest rate overall of its use in-store.

When it comes to wallet choice, Japanese consumers generally prefer using FinTech mobile wallets hosted on native apps, using them for more than 88% of in-store mobile transactions. In general, FinTechs are responding to this local consumer demand by creating platforms specifically coded for iOS, Android or other operating systems to offer optimal performance. One example of these apps is Adyen, which announced the launch of its business-focused payments platform in December but also offered a consumer-facing mobile wallet tool. In an interview with PYMNTS’ Karen Webster, Adyen’s Global Head of Unified Commerce Brian Dammeir said, “The way we look at the evolution of the next five to 10 years is that the distinction between digital eCommerce and in-person interactions is starting to gray and frankly is probably going to eliminate over time.”

Another is British FinTech startup Revolut, is concentrating its expansion efforts in the Asia-Pacific region. Currently offering services in 36 countries, Revolut provides money transfers, P2P payments, investments and other services. As part of these expansion efforts, the company announced in November that it planned to grow its Japan user base from 80,000 to one million.

Bringing once digital-only innovations such as mobile wallets into brick-and-mortar locations is just one example of these and other countries becoming increasingly connected daily. Given these trends, it may be safe to assume that this will only increase as digital innovations and tools become more and more a part of how we live.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More