In the bid to build a super app, just because you can — or think you can — doesn’t mean you should.

News came this week that Elon Musk, who seems to be bent on having a go at every business model there is, still has his eyes on launching a super app.

Bloomberg’s report notes that Musk is in the running to debut an as-yet-undefined offering that will (at least for now) be known as “X, the everything app.” There’s no real detail beyond that.

Of course, there’s some wood to be chopped before then, as Musk has also been busy forging ahead with plans to buy Twitter at the original asking price.

The app ambitions raise a few questions, namely, just what it would look like and whether Twitter can be a launching pad toward building out an ecosystem.

It’s far from a sure bet.

Advertisement: Scroll to Continue

And, at least in Musk-land, we’ve been here before. Back in May, we detailed that Musk said that he’d make Twitter into a super app that would broaden Twitter’s social media functionality and add payments into the mix.

WeChat is an obvious model and one that has been touted by Musk. But that template took shape in the days before the pandemic reshaped us all.

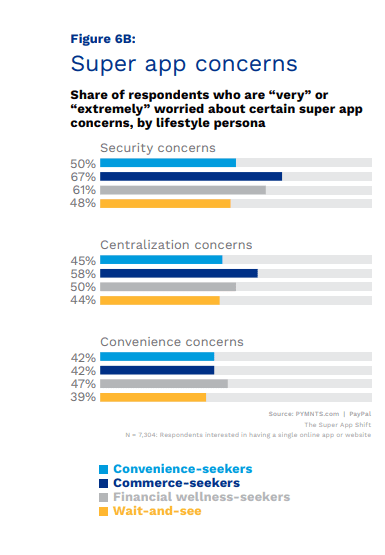

PYMNTS’ research has shown that three-quarters of consumers would be interested in super apps. The fact remains that they’d only trust a few providers to deliver them. Concerns still linger, as detailed in the “Super App Shift” report by more than 9,000 consumers in the U.S. and Europe surveyed by PYMNTS, over the safety of having all that data accessible and accessed in one place.

Security worries cut across all of the personas we’ve encountered — from the people who want the convenience of the app itself to those who would ostensibly use that app to conduct commerce (which is part of Musk’s ambitions). It isn’t the case anymore that social media and messaging represent ground zero for super apps, as had been seen in Asia (there’s the WeChat example again).

The data seems to indicate that consumers have already made up their minds about the providers they trust to deliver those super apps. The banks? Well, they come first, trailed a bit by PayPal. Big Tech is quoted way down on the list and Twitter does not make the pantheon of Big Tech names that would be trusted. The chart below depicts the country-by-country trust levels — none of which auger particularly well for Twitter if the ambition is to forge a super app that is truly global in reach.

We need to note, too, that a super app’s very appeal — its sticky web of services and products woven together, with a digital front door as an entryway — is a formidable barrier to a Twitter-centric offering. A WeChat user, for example, would be loath to switch to another provider because so much of daily life is already being lived within that digital umbrella. Though it is true there is no super app yet in the U.S., a number of huge players with deep pockets are well on their journeys to build them. Walmart stands out here with its push into digital banking. Amazon’s doing it too, starting with payments and commerce and then crucible branching out into other parts of life — music and entertainment, for instance.

Musk’s ambitions loom large, but his reach may exceed his grasp.