Not at bad week’s performance for the beleaguered CE100.

But then again a single week does not a trend make.

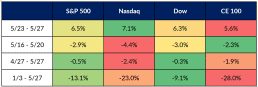

The CE100 Index was up 5.6%. but that was not enough to bring the last full week of trading in May to a positive result, and it lagged the overall, broader indices. The trailing 12 month performance was off by 1.9%, and for the year these publicly traded, largely digital-only upstarts have slipped by 28%.

CE100 Relative Performance

Source: PYMNTS

The vast majority of the pillars were in positive territory, with only the Communication segment down for the week, off 2.8%.

And within that Communications sector, we need look no further than Snap, to see what, well, snapped. Shares in that company plunged 33% on the week, and now stand 66% lower than where they opened the year.

As noted in this space earlier in the week, the company’s shares took a drubbing on the news, from CEO Evan Spiegel, that Snap would come in at the low end of internal targets for the current quarter, which will end in June. In addition, the firm will slow hiring all the way through the end of the year.

Macro Headwinds Gather Momentum

Per a filing with the Securities and Exchange Commission, management has pointed to the tough macro climate as reason for the miss. That means that growth is slowing, of course — and we contend that growth (and investors’ expectations of growth) is what buoys the CE100 names.

Snap’s terrible, awful, no good week we tempered, at least in part, by positive showings from peers in the Communication pillar, among them several platform firms. By the way of example, shares of Zoom zoomed by 23% through the past week, on the back of reports that the company’s revenues were up 12% in the most recent quarter. At the end of the first quarter of 2023, the company’s approximately 198,900 Enterprise customers were up 24% from the same quarter last fiscal year as hybrid/remote work trends remain firmly in place.

As for positive performance, by pillar, banking stocks were largely higher through the most recent few days, as the segment gained more than 10%. It’s important to note that the results here got a boost not just from the marquee FIs in the sector, such as JPMorgan Chase, which gained 11% — digital platforms also had strong showings.

LendingClub was a standout here, where the stock was up 19.4%. The online financial services platform said this week that it added client-to-client institutional sales functionality to its LCX automated loan auction platform. In an interview with PYMNTS’ Karen Webster, Clarke Roberts, SVP of Electronic Trading Services at LendingClub, said that streamlining and automating whole loan auctions can improve price discovery and transparency — and even improve financial inclusion.

Read also: Client-to-Client Sales the Next Evolution

The lines are, of course, blurring in finance, where brick-and-mortar players are setting sights on JPMorgan, which for its part has been committing significant sums to its tech upgrades (billions of dollars), and said earlier in the month that its U.K. digital bank processed 20 million payments in eight months and has more than half a million customers served by that operation.

A shortened week looms before us, and June is already here — which of course means there is only one more month left in the quarter. Wall Street takes stock (literally) as earnings announcements and warnings mount, and we’re due for another deluge of caution (and some pockets of optimism) before too long.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More