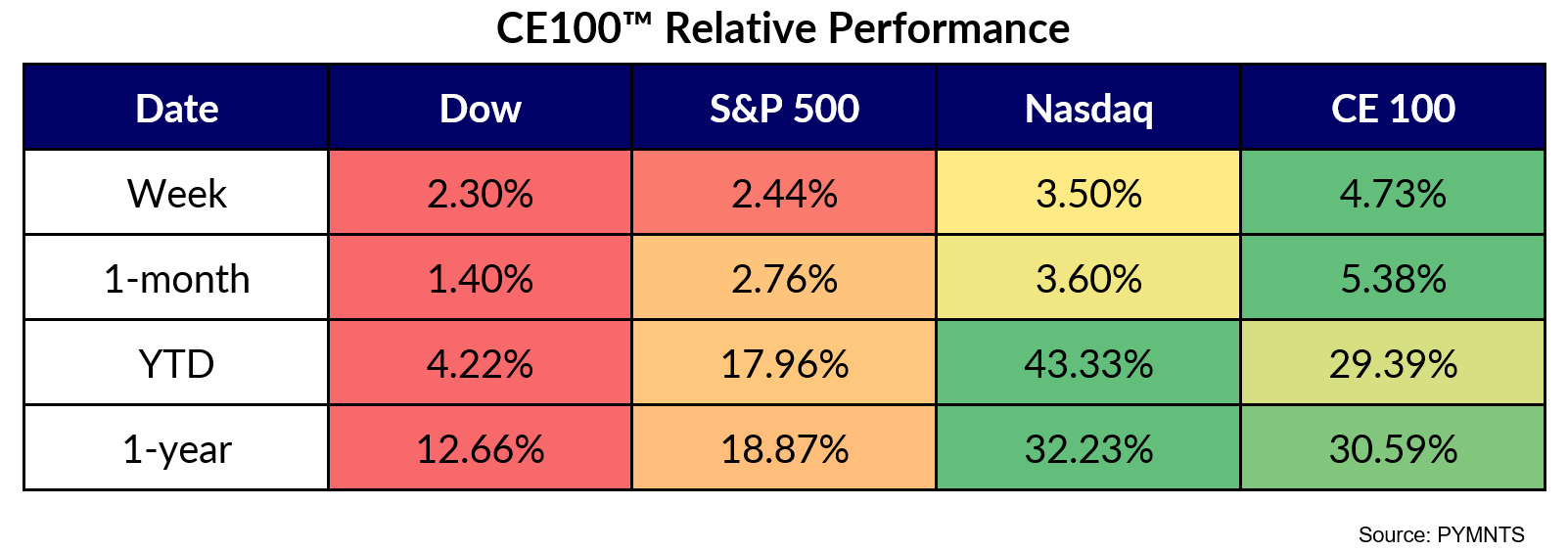

All pillars gained ground as the Index itself surged 4.7%.

The communications pillar led the way, up 7.7%. In that segment, shares of Snap were ahead 12.7%.

As reported here, Snapchat’s bid to allow creators allowing them to share ad revenue, which debuted in April — Snap Star — has logged a roster of several thousand creators. The time users spent watching Snapchat Stories from creators in the revenue-sharing program more than doubled in the first quarter of the year, according to reports.

The Pay and be Paid segment surged 6.8%.

Affirm Garners Positive Sentiment

And in that group, Affirm’s 20% rally represented a snapback in the wake of a downgrade earlier this month from Piper Sandler. But Barclays stepped in this past week, boosting its price target on the name to $19 from $16, and maintaining its “overweight” rating.

Separately, as noted by Yahoo Finance, Mizuho Securities has expressed optimism regarding Affirm’s Debit+ card — with a precursor in the success of Square’s Cash Card as far back as 2017. Elsewhere, Amazon Prime Day loomed large this past week, and Amazon has added Affirm’s pay-over-time option to Amazon Pay.

Shares in Block were up 12.2%. Square now offers its U.S. sellers a credit card, new loan options and early deposit access.

These new tools are designed to meet sellers’ financing and cash flow needs and empower them to more efficiently manage their business finances, according to the company. The new Square Credit Card is now in beta, features a credit limit based on the sales the seller processes through Square,

In a third new offering, Square now offers early deposit access to Square Checking sellers, allowing them to receive funds made through off-platform channels up to two days faster.

Bank Stocks Power Ahead, Too

The Banking group was up 2.7%. JPMorgan was up 3.8% on the week, trailed by Citigroup, up 0.1%. The duo helped usher in earnings season, with the data coming in to show that despite macro headwinds, some trends remain intact.

In our own coverage of these banks’ earnings, at JPMorgan, total payments transactions stood at 1.5 trillion, roughly flat with a year ago. Flat volume, we noted, indicates a willingness to keep spending on cards. The company disclosed in its earnings supplements that debit and card sales volume was up 7% year over year.

During the conference call with analysts, CFO Jeremy Barnum noted that card spending represented consumers’ desire to “want to have rather than need to have” revolving balances as those balances were up 16% to $187 billion. The expected net charge-off rate through the current fiscal year is expected to be 2.6%, per management commentary on the call.

Citi logged growth in its card business as U.S. card spend volumes were up 3% year over year to $152 billion. The card average loans surged 12% to $149 billion. Commercial card spending was up 15% to $15 billion.

Per the supplemental materials, the credit card loans at least 30 days to 90 days past due on its branded business came in at 0.8%, up from 0.5% last year. Average deposits were up 1% to $1.3 trillion.