There are and always have been sharp differences between how consumers in different demographic groups experienced the quick and total digitization of the United States economy. In July 2022, PYMNTS identified and measured a sharp divide between how consumers in different income brackets used the internet in their daily lives.  High-income consumers are consistently more likely than low-income consumers to use digital tools to travel, bank, keep in touch with their families, access healthcare and more. In total, high-income consumers are 70% more likely than low-income consumers to participate in the digital economy.

High-income consumers are consistently more likely than low-income consumers to use digital tools to travel, bank, keep in touch with their families, access healthcare and more. In total, high-income consumers are 70% more likely than low-income consumers to participate in the digital economy.

“The ConnectedEconomy™ Monthly Report: Digitally Divided — Work, Health and the Income Gap” examines how the online lives of the country’s highest- and lowest-paid consumers measure up against each other, uncovering the key forces separating them. We surveyed a census-balanced panel of 2,710 consumers between Jan. 6 and Jan. 10 to build upon our ongoing research into how the digital transformation of the U.S. economy is reshaping consumer habits. This edition details how consumers’ online lives diverge as their salaries do, and it explores what that means for the future of the ConnectedEconomy™.

Key findings from the report include the following:

• More consumers went online in the last 12 months, primarily driven by their use of apps to find the best deals on travel and transportation. Across all 10 verticals we study, more consumers are participating in more digital activities than they did one year ago.

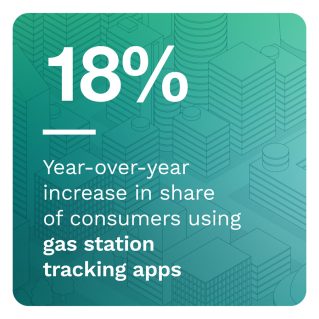

The most significant increase we’ve seen is in the share of consumers using digital to support their travel and commuting needs, using apps, aggregators and platforms to help them do everything from commuting to planning vacations. Fourteen percent more consumers reported using digital tools for these activities in January 2023 than one year prior. The use of apps to track and locate gas stations is up the highest of all — 18% year over year.

• Consumers’ use of digital payments increases as their level of digital participation increases — both within and across digital activities.

The most connected consumers tend to be the most likely to use digital payment methods such as digital wallets and digital tools to make everyday transactions. High-income consumers are a prime example: They are also twice as likely to have paid for their most recent purchase via a digital wallet as in January 2022. Twenty-one percent of high-income consumers paid for their most recent purchase via a digital wallet, while just 12% of low-income consumers did the same.

The most connected consumers tend to be the most likely to use digital payment methods such as digital wallets and digital tools to make everyday transactions. High-income consumers are a prime example: They are also twice as likely to have paid for their most recent purchase via a digital wallet as in January 2022. Twenty-one percent of high-income consumers paid for their most recent purchase via a digital wallet, while just 12% of low-income consumers did the same.

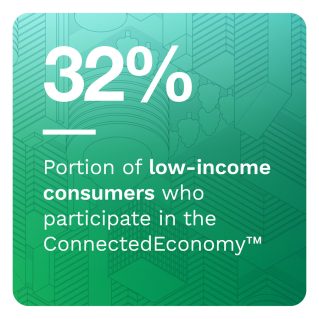

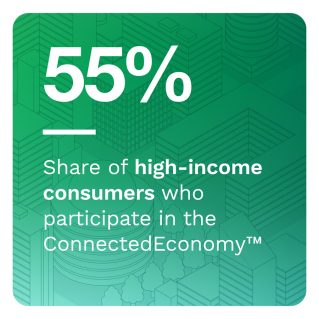

• High-income consumers’ participation in the ConnectedEconomy™ is up 9% year over year, but low-income consumers’ participation has remained virtually unchanged.

High-income consumers are using digital more, partly because they are still working from home, while low-income consumers are increasingly returning to jobs requiring them to work on-site. High-income consumers are now 78% more likely than low-income consumers to be in jobs they can perform from home: 71% of high-income consumers, a projected 45 million individuals, now do at least some of their work remotely from home — up 10% year over year.

To learn more about how income appears to correlate with consumers’ digital engagement and behaviors, download the report.