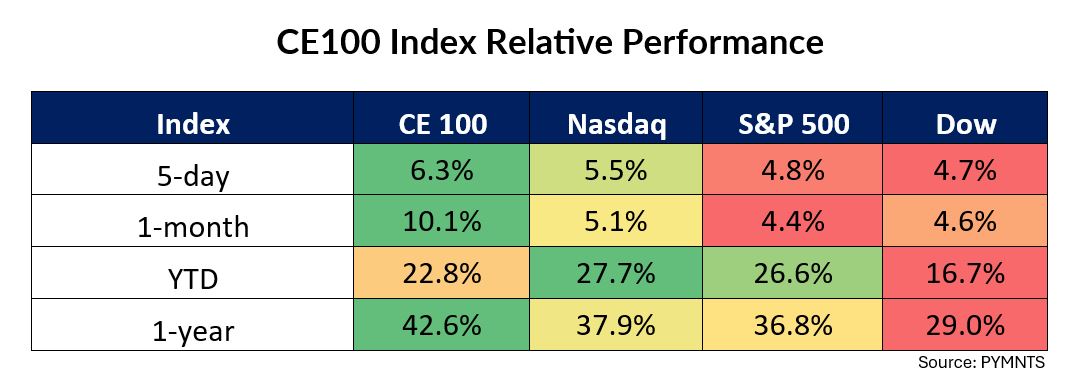

Earnings, earnings everywhere — and for connected economy stocks in the CE 100 Index, roaring ahead almost in lockstep, the week was a good one.

Indeed, two sectors of the CE 100 — the Live segment and the Pay and Be Paid pillar — surged double-digit percentage points, with respective 12.2% and 10.7% gains.

The banking segment was ahead by 8.4%, as the impeding Trump presidency ignited optimism on Wall Street over banking deregulation.

Within the Pay and Be Paid cohort of the CE 100, Sezzle was a standout here, leaping more than 100% through the week, rallying 72% on Friday alone in the wake of earnings reported Thursday.

Sezzle’s results and earnings materials indicated that active subscribers for its Premium and Anywhere offerings jumped by 319,000 from last year’s September period to end at 529,000 in the most recent quarter. Active customers, overall, were 3.6% higher than last year to 2.7 million. Repeat usage as a percentage of total orders stood at 95.7%, compared to 93.8% a year ago. And quarterly purchase frequency stood at 5.4x, from 3x last year in the third quarter. Total revenues were 71% higher year on year to $40.8 million.

In addition, as CEO Charlie Youakim said on the conference call with analysts, ”the partnership with WebBank has simplified our business, allowing us to focus on a unified product construct, which aids profitability. The on-demand product has led to a 30% increase in activations, reducing entry friction for consumers and serving as a bridge to subscription services.”

The other BNPL stalwart in the CE 100 group, Affirm, saw shares up 7.5%.

In our coverage of earnings, Affirm’s CEO Max Levchin remarked on the company’s earnings call that the company has a third of the volume and more than half of the revenue in the United States pay later space. Affirm notched double-digit gains in active customers and merchant counts. Transactions per active consumer grew 25% year over year to 5.1. Gross merchandise volume (GMV) rose 35% year over year to $7.6 billion.

By spending category, Affirm noted that the company saw double-digit growth across the board as measured by GMV, with the exception of slight declines in sporting goods and outdoors. The general merchandise category grew 47%; the electronics, equipment and auto categories all grew more than 25% year over year. Total revenues were 41% higher to $698 million. Within its direct-to-consumer efforts, Affirm Card (a Visa debit card) generated $607 million in GMV, up 20% from the fiscal fourth quarter and up 171% year over year.

Block shares gathered 3.3%, still positive for the week despite losing 10% after reporting earnings, where revenues of $5.9 billion missed Wall Street expectations of $6.2 billion.

As reported this week, Block saw a 15% improvement in retention of sellers who adopted a full suite of banking products (three or more) compared with sellers who did not. For the third quarter, Block reported $2.3 billion in gross profit, up 19% from a year ago. Block’s Cash App businesses reported $1.3 billion in gross profit, up 21% year over year. During the same period Cash App Card monthly active users increased 11% to more than 24 million.

In the Live segment of the CE 100, Porch Group sailed 55.4% higher, extending gains from the previous week, as the latest quarter’s profitability metrics were better than the Street had anticipated. The firm reported that though revenues slipped by 14% to $111.2 million, adjusted EBITDA ( a rough measure of cash flow) was positive $16.9 million, up from $8.8 million last year.

Declining names were few and far between in the CE 100 Index this past week.

iRobot shares sank 27%. The company’s third-quarter sales of $193.4 million, up 3.9% year on year, missed consensus of $218 million. The 2024 net sales forecasts of $685 million to $710 million were down from previous forecasts of $765 million to $800 million. In the statement that accompanied the results, CEO Gary Cohen remarked that “our overall results did not meet the expectations we set in August, as persistent market segment and competitive headwinds impacted our sell-through performance.”

MercadoLibre led the lone sector to post losses — the Shop sector of the CE 100, down 0.4% — dipping 8.9%.

The company’s recent earnings detailed that users of its digital bank, Mercado Pago, soared by 35% year over year, indicating greater reach into financial services.

However, continued investments in those credit operations and in commerce fulfillment centers (five new additions in Brazil and another in Mexico) pressured margins.

The company said in its earnings materials and during a webcast with investors that eCommerce operations showed momentum, as GMV across its online marketplace gained 14% year over year to $12.9 billion. Items sold reached nearly 456 million in the third quarter, up 28% YoY. As for the credit operations within Mercado Pago, the overall business grew 77% YoY to $6 billion, the credit card operations leaped 172%, and that portfolio reached $2.3 billion.

Non-performing loans have been stable, according to commentary on the call. Management also indicated that the investments in the aforementioned fulfilment centers has come as the company expects future demand in those markets to increase, which necessitates capacity buildouts.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More