The higher a consumer’s income, the higher their credit score and the less often they check it, according to “The New Reality Check,” a PYMNTS and LendingClub collaboration based on a survey of 2,326 U.S. consumers.

Get the report: The New Reality Check

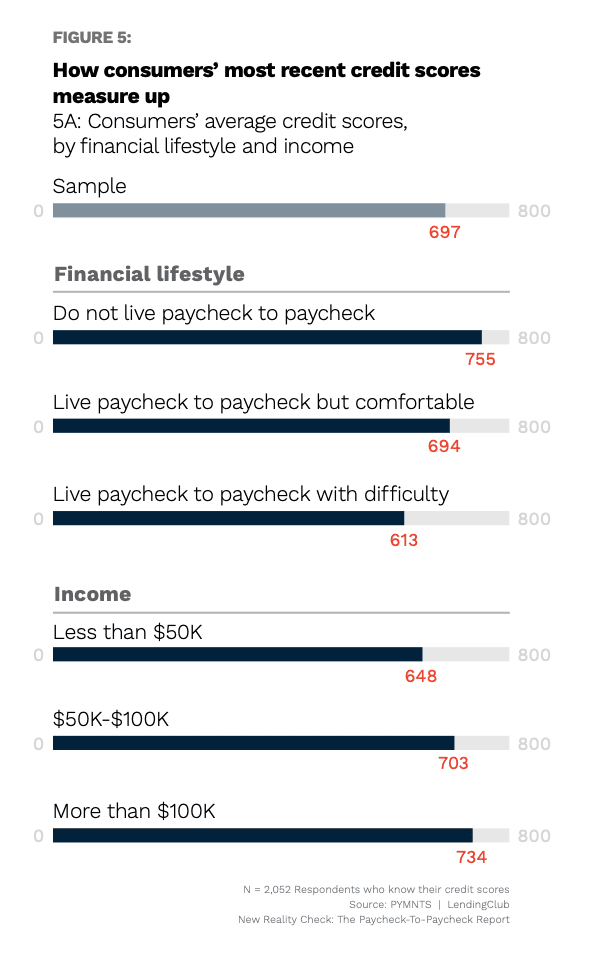

Among those included in the survey, the average U.S. consumer’s credit score in March 2022 was 697.

When categorized by income, there’s an 86-point gap between the credit scores of high-income consumers and low-income consumers, the report found.

The average credit score among high-income consumers — those earning more than $100,000 — was 734.

Among consumers earning $50,000 to $100,000, the average credit score was 703.

Among low-income consumers — those earning less than $50,000 — the average credit score was 648.

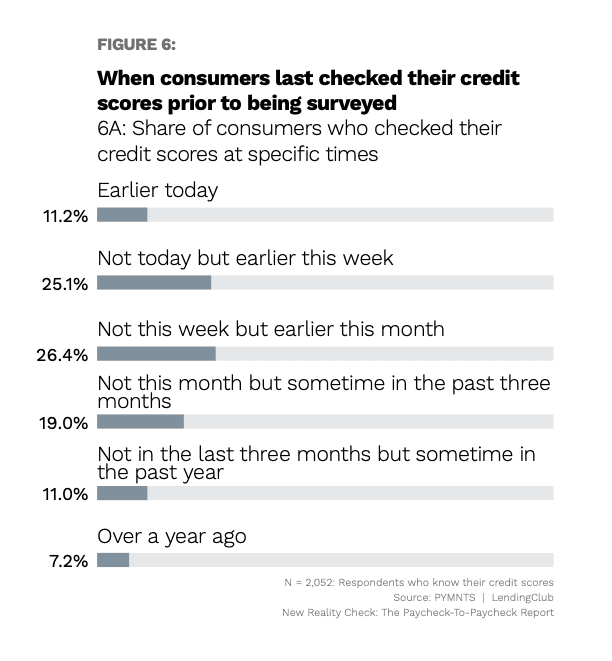

Sixty-three percent of all consumers said they had checked their credit score during the month leading up to March 2022, with 11% saying they had checked it earlier during the day they were surveyed, 25% saying they had checked it not today but earlier this week and 26% saying they had checked it not this week but earlier this month.

Among the different income groups, there’s a difference of seven percentage points in terms of the share of consumers who check their credit scores monthly

Those with a below-average credit score checked their report more often — and most frequently among the three income groups identified in the report — with 67% saying they had checked it during the month prior to being surveyed.

Among consumers with a credit score that was about average, 63% had checked it — the same percentage as that of the entire sample.

Those with an above-average credit score checked it least often, with 60% saying they had checked it during the month leading up to March 2022.