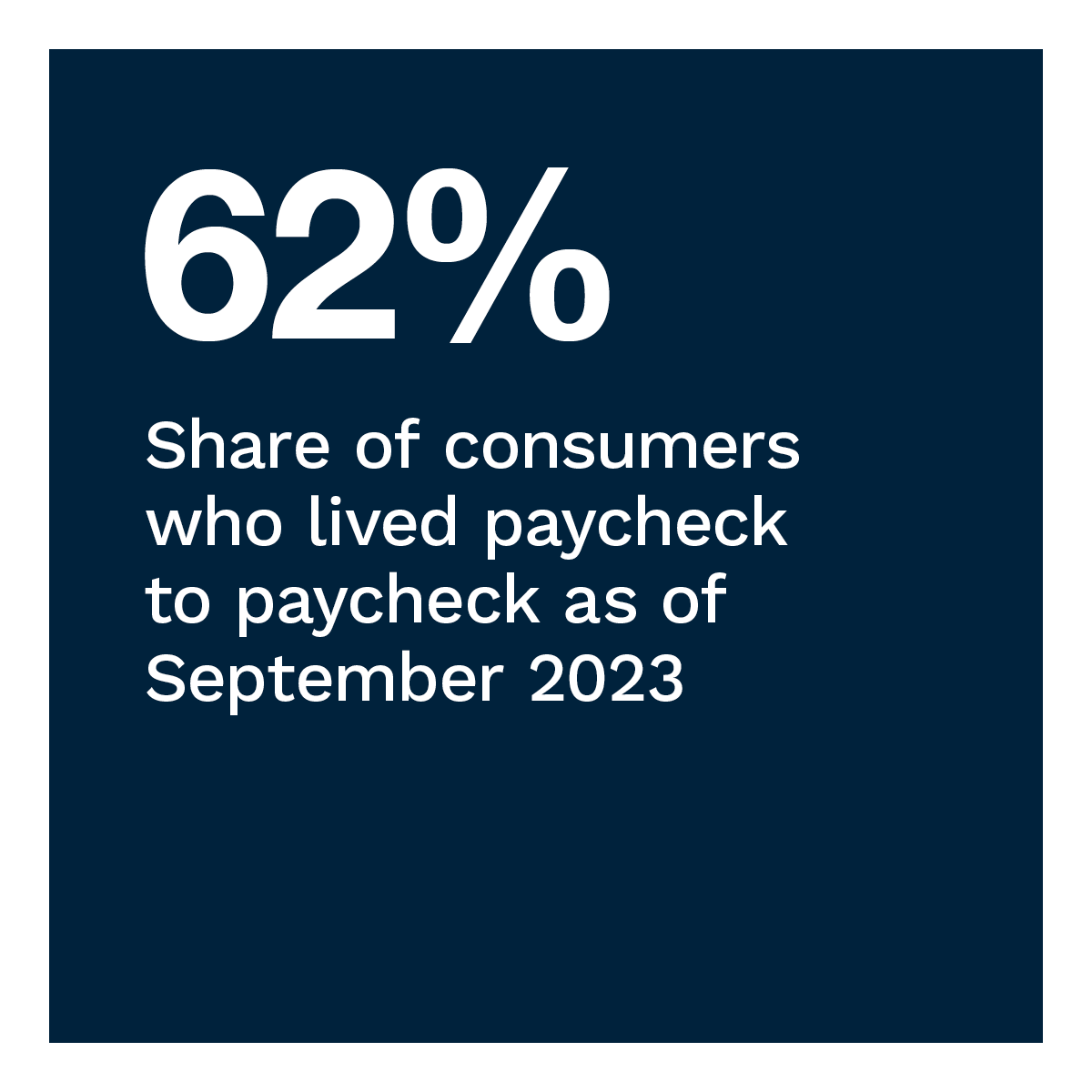

Living paycheck to paycheck continues to be the predominant financial lifestyle in the United States. As of September 2023, 62% of consumers live paycheck to paycheck, with 22% struggling to pay their monthly bills. Despite efforts to manage budgets, consumers across financial lifestyles report putting aside savings can be challenging. This is especially true when faced with major or unexpected expenses.

More than three-quarters of consumers report using a significant percentage of their saved income on a major expenditure at least once. Moreover, consumers say they deplete 67% of all available savings, on average. The average consumer faces such depletions once every four years. Among paycheck-to-paycheck consumers, the average recurrence drops to once every 2.5 years. Emergency expenses — as well as major life events — are the main reasons consumers use the money they have saved.

These are just some of the findings detailed in this edition of “New Reality Check: The Paycheck-to-Paycheck Report,” a PYMNTS Intelligence and LendingClub collaboration. The Savings Deep Dive Edition examines consumers’ ability to put aside and save money in the current economic environment, especially when faced with major expenditures. This edition draws on insights from a survey of 3,648 U.S. consumers conducted from Sept. 5 to Sept. 20 and an analysis of other economic data.

Other key findings from the report include:

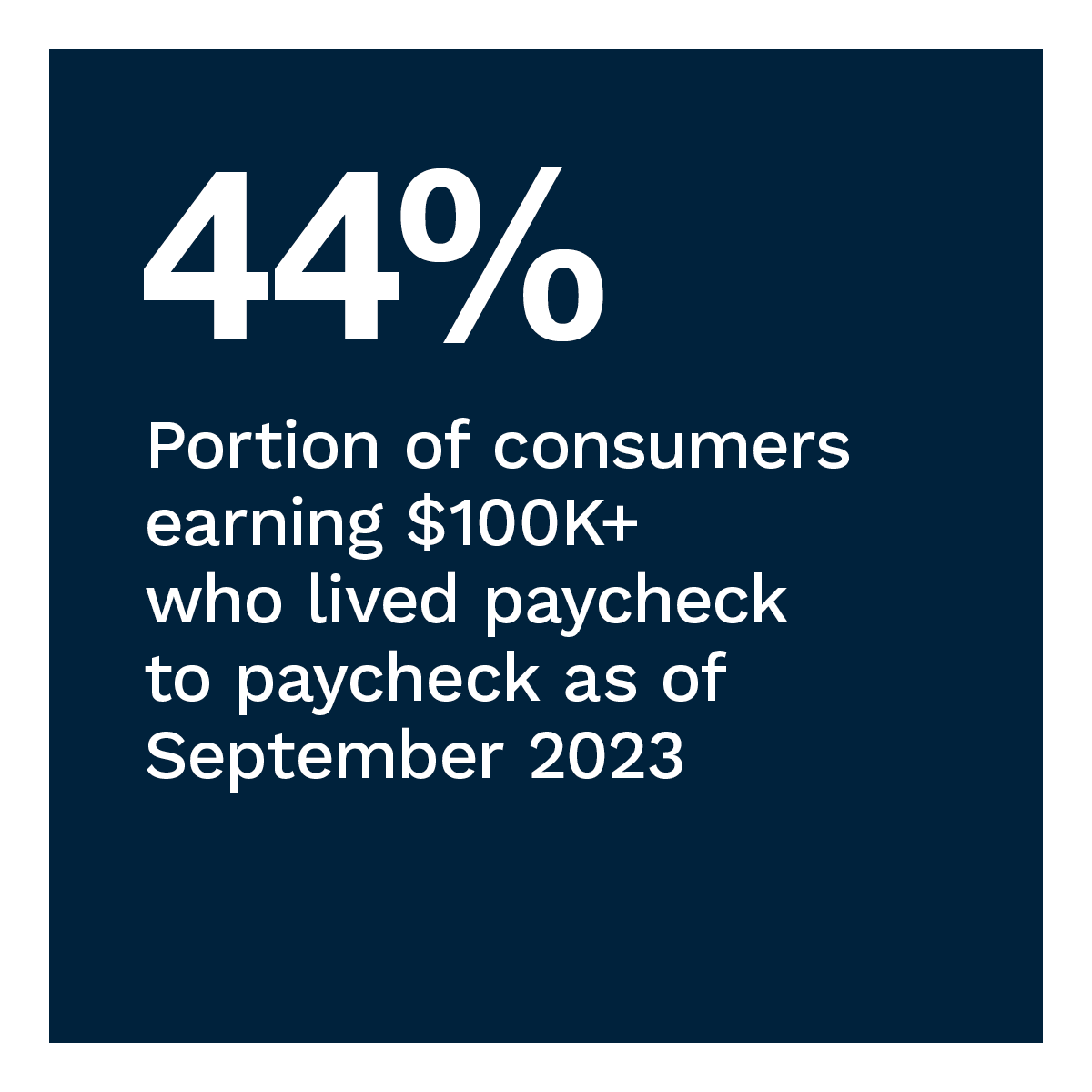

Aggregate consumer savings amounted to an average of $11,000 per consumer in September 2023. This amount is roughly unchanged from September 2022 after netting out the effect of inflation. However, the average amount that is readily available in real terms has dipped 7% since September 2021. Those with the most domestic savings are less likely to have seen their savings ability dip. Consumers annually earning more than $200,000 are the most likely income bracket to cite an increased ability to save.

Seventy-eight percent of all consumers surveyed recall having at least one expenditure that required them to withdraw a sizable portion of their savings. That share rises to 90% among paycheck-to-paycheck consumers with issues paying their bills. Bridge millennials, at 83%, are the generation most likely to report this.

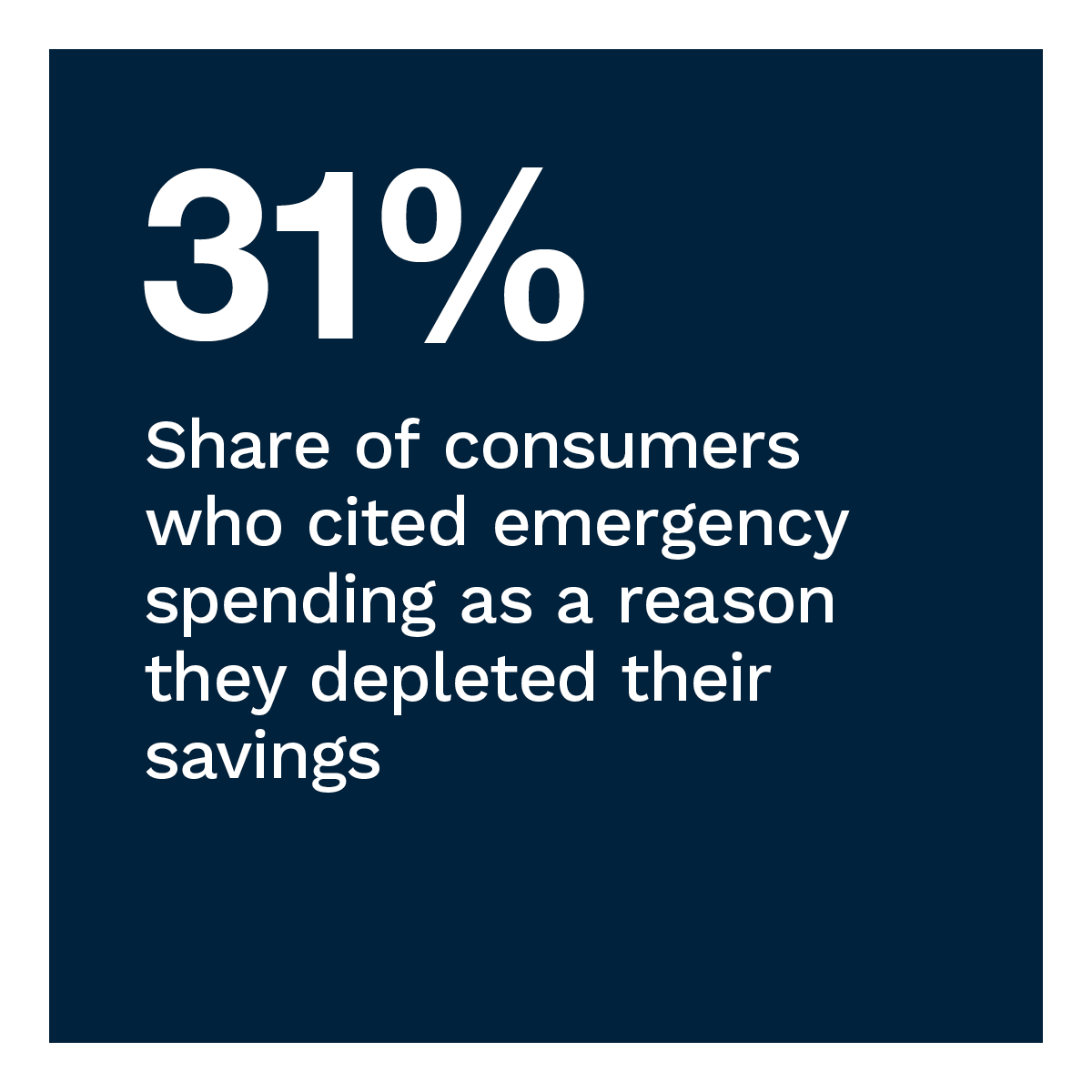

Consumers can face various major nondiscretionary events that can deplete their savings. Emergency expenses are the most cited, at 31%, followed by job loss or income reductions, at 20%. Discretionary spending on major life events, travel and buying expensive items are other reasons consumers cite. Interestingly, virtually the same share of consumers cite discretionary events as emergency expenses.

Struggling consumers continue to find ways to manage budgets and save. At the same time, they face discretionary and nondiscretionary events that can deplete these savings. Download the report to learn more about the impact of major expenditures on how U.S. consumers living paycheck to paycheck save their money.