As the economic and financial imbalances caused by the pandemic persist, access to credit has become vital for covering short-term financial needs, purchasing goods and services, and paying bills.

Against this backdrop, overdrafts have emerged as a popular form of credit, providing consumers with financial flexibility while generating revenue for financial institutions.

However, this form of credit comes at a cost, per findings detailed in “The Credit Accessibility Series: How Consumers Use Overdrafts,” a PYMNTS Intelligence report with Sezzle which examines consumer behaviors and sentiments related to the use of overdrafts based on a survey of more than 2,800 consumers in the United States.

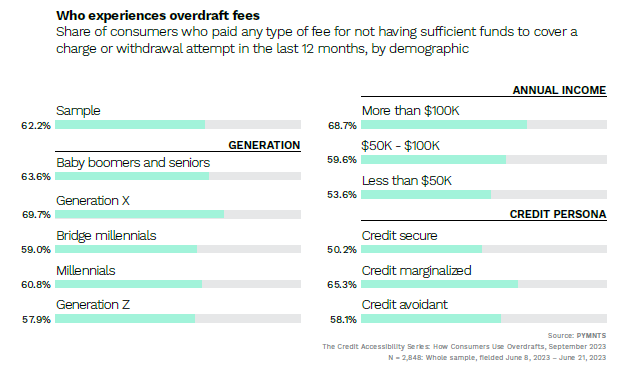

According to the study’s findings, 62% of consumers who attempted a transaction without sufficient funds were charged some type of overdraft fee in the last 12 months. These fees varied, with 45% of consumers being charged a flat fee and 27% being charged a percentage of the transaction.

Across various age groups, a higher share of older generations than younger ones were found to have incurred overdraft fees due to insufficient funds for charges or withdrawal attempts within the past 12 months. Specifically, nearly 70% of Generation X and 64% of boomers found themselves in this situation, surpassing the average of 62%.

Following closely behind were millennials and bridge millennials, with approximately 61% and 59%, respectively, attempting transactions without adequate funds over the same period. Generation Z exhibited the lowest rate, albeit with a slight gap, at about 58%.

When it comes to income categories, individuals with higher incomes, particularly those earning over $100,000 annually, topped the list in attempting more transactions without sufficient funds within the last year, with nearly 70% of them experiencing overdraft fees as compared to just 54% of those earning less than $50,000.

Overall, the average consumer is overdrawn for 9 days, and needs an average sum of about $370 to fully cover the transaction.

Examining the data further shows that the usage of overdrafts often leads to further financial hardships for consumers. In fact, 90% of consumers who experienced overdrafts faced additional financial difficulties, while 84% of consumers who had their transactions declined also experienced hardships.

Overdrafts can also result in broader credit accessibility issues, damaged credit scores, and the inability to pay accumulated fees, while transaction declines can lead to uncovered charges, including bills and other essentials, resulting in services being cut off.

In summary, the reliance on overdrafts as a form of credit highlights the financial insecurity faced by consumers across income brackets and credit backgrounds. Moreover, the high prevalence of overdraft fees and the resulting financial hardships underscore the need for education on financial and credit management to address the specific challenges faced by different consumer groups.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More