Through the next few months, the purses and wallets will open in anticipation of holiday spending.

Beyond the cash flow hangover that might be a result, and as consumers continue to expect inflation to remain a feature of everyday life and perceive credit as tougher to get, it’s the subprime consumer who may be the most pressured.

Who Is the Subprime Consumer?

Broadly speaking, subprime consumers are those individuals with FICO scores that are roughly in the 580 to 619 range. But definitions vary. Experian said on its website that subprime consumers are defined as having a FICO score below 670, a categorization that encompasses roughly a third of the U.S. population.

Why Are They Subprime — and What Happens?

These consumers have perhaps missed a payment or two or had a charge-off or distressing financial event such as a foreclosure. Or they might be new to credit in the first place.

There’s a bit of a vicious cycle that develops when subprime consumers seek to tap the credit markets. Subprime borrowers tend to be viewed as a more acute credit risk, so they must grapple with higher interest rates and higher fees — all of which mean that loan terms are onerous enough that they’re hard to satisfy. The subprime borrower then might miss payments, which makes getting any new credit and rising above subprime status a difficult, if not impossible, task.

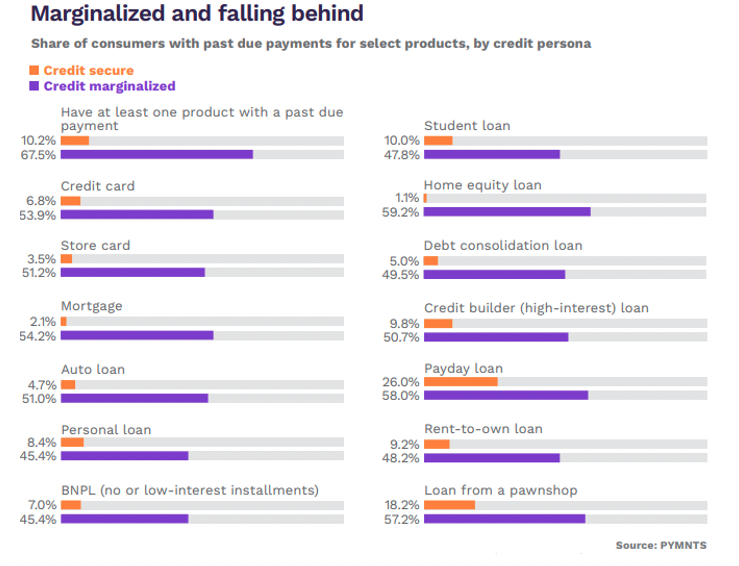

And that means, then, that many subprime individuals are credit marginalized.

Advertisement: Scroll to Continue

The report “How Credit Insecurity Is Changing U.S. Consumers’ Borrowing Habits,” a PYMNTS Intelligence and Sezzle collaboration, found that 50% of credit-marginalized consumers are those with FICO scores below 650, which places them firmly within the subprime category.

Credit-marginalized consumers represent about a quarter of the overall population, and they have been rejected at least once when applying for credit products in the past 12 months.

How Do They Live?

If most subprime consumers are marginalized, and 46% of the marginalized population lives paycheck to paycheck with issues paying bills, they are finding that their spending options are a bit pressured. A full 79% of those individuals have been negatively impacted by an adverse event in the past year, such as losing a job or suffering from the death of a loved one. A third of marginalized U.S. consumers said they have struggled to get loans in the wake of those tough life events.

Where Are the Pressures?

Fifty-four percent of the credit-marginalized population — again, dominated by subprime borrowers — have fallen behind on a credit card payment, and more than half have done so with a buy now, pay later (BNPL) loan.

What’s Next?

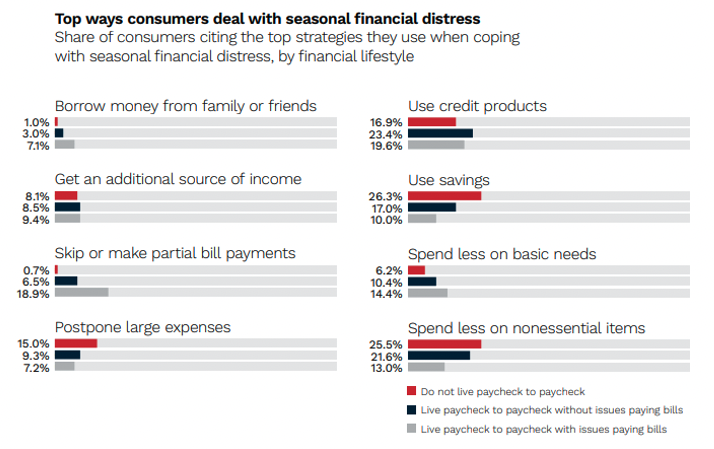

Research by PYMNTS Intelligence and LendingClub into what’s to come during the holiday season paints a tough portrait for subprime, paycheck-to-paycheck households. Roughly a third of individuals with issues paying their bills will use credit where they can to grapple with financial stress, 10% will spend less on basic needs, and 17% will tap into their (already dwindling) savings.

What Might Help?

There’s a growing interest in using BNPL to manage everyday expenses and spread payments out over time on terms that are less expensive than traditional credit products.

The report “BNPL’s Wide-Ranging Impact on Consumers and Merchants,” another PYMNTS Intelligence and Sezzle collaboration, found that 28% of consumers said the low- or no-interest rate hallmarks of BNPL are among the most important features in choosing the payment option, and three-quarters of subprime consumers use it. About 19% of the subprime users said they see it as a way to improve their credit scores — a nod to the fact that they want to escape the constraints of credit marginalization.