The new (and reportedly final) rule on overdraft fees may have consumer groups — and consumers — cheering.

But the Consumer Financial Protection Bureau’s (CFPB) move may have a series of negative ripple effects for those same consumers, as banks consider offsetting the impact of new regulations, which among other things, caps the fees at $5.

PYMNTS has noted the move may set up legal jousting in the courts, and as has been widely reported, the CFPB itself may be in for some significant changes when the new presidential administration comes to Capitol Hill next month.

Those ripple effects could include a cutback in some services and products — including overdrafts themselves, which have at times offered at lifeline to consumers trying to pay for essentials.

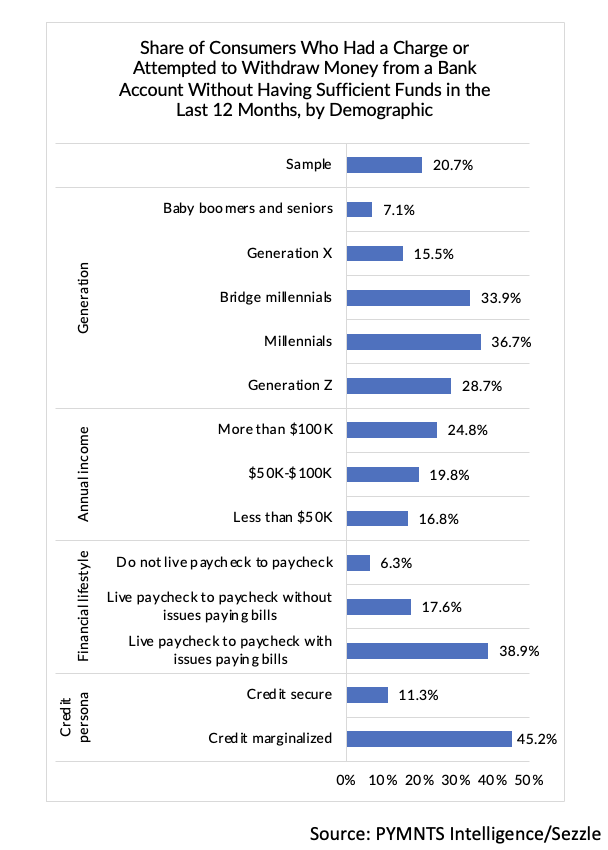

PYMNTS Intelligence, in collaboration with Sezzle, has found that as many as 20% of consumers have withdrawn money from an account through the past 12 months without having the funds on hand to cover the transaction. As seen below, the percentage rises dramatically for consumers who live paycheck to paycheck and have issues paying bills — at nearly 39% of that demographic. The percentage rises, too, for consumers who are credit marginalized and find headwinds in accessing products like credit cards or loans, where the tally is more than 45%.

Of the individuals who, at one time or another, had insufficient funds to cover a transaction, nine in 10 said the reason was due to financial hardship. Of that percentage, 43% said that they had trouble meeting the costs of life’s essentials such as food or housing.

Advertisement: Scroll to Continue

The data shows that 16% of the individuals that we surveyed used an overdraft to cover a non-sufficient-funds event. The average consumer’s overdraft lasted about 10 days and was tied to an average transaction value of $369. The average flat fee paid was $29 for the overdraft, or a percentage of the transaction equating to 2.9% of the transaction.

The read across is that the overdraft can act as a financial lifeline — a form of credit extended by the bank, in other words — to help “cure” an urgent situation.

The Ripple Effects

Fees tied to overdrafts and cash advances are drawing increased scrutiny. As PYMNTS reported last month, for example, the Federal Trade Commission (FTC) has sued financial app Dave, alleging that fees (including a tip system) are tied to deceptive marketing practices when consumers take out cash advances.

In the meantime, the CFPB has offered up a trio of options. As PYMNTS reported on Thursday, institutions affected by the new regulations must choose one of three options for their overdraft programs: cap overdraft fees at $5; set fees to cover only costs and losses; or comply with standard lending laws, including interest rate disclosures.

On the reduced fee front, the CFPB has stated that capping the fees would save consumers about $5 billion. We note that, in October of 2023, that among banks with over $10 billion in assets, 97% of NSF fee revenue has been eliminated. Among the 75 banks earning the most overdraft/NSF fee revenue in 2021, 95% of NSF fee revenue has been eliminated.

The economics of overdrafts require that the bank takes on the risk of paying for the transaction, in effect “floating” it until there’s an inflow of funds to repay the overdraft. A flat fee, now ostensibly at $5, might not be commensurate with the risk. And it bears mentioning that the banks are not required to ensure that a transaction goes through — the overdraft is a service that can, of course, be reconfigured, scaled back or eliminated.

Turning over the account to a collection agency, in the event that the overdrafts are not paid back in the agreed upon timeframe, takes time and money, and there’s no guarantee that there’ll be a successful outcome (and credit scores are negatively impacted). Simply declining the transaction, which is an option for the banks (and may be more widespread), creates the dual hardship of making that essential purchase an impossibility. Late fees from the biller — say, a utility, or a rental company — pile up, adding to at least some of the financial stressors confronting consumers.

And when viewed through that lens, the victory claimed by the CFPB may prove a Pyrrhic victory for consumers.